EX-99.1

Published on September 9, 2014

The PNC

Financial Services Group, Inc. Barclays Global Investor Conference

September 9, 2014

Exhibit 99.1 |

2

Cautionary Statement Regarding Forward-Looking

Information and Adjusted Information

Our presentation includes snapshot

information about PNC used by way of illustration. It is not intended as a full business or

financial review and should be viewed in the context of all of the information made

available by PNC in its SEC filings. The presentation also contains forward-looking

statements regarding our outlook for earnings, revenues, expenses, capital and liquidity

levels and ratios, asset levels, asset quality, financial position, and other matters

regarding or affecting PNC and its future business and operations. Forward-looking statements are necessarily subject to numerous

assumptions, risks and uncertainties, which change over time. The forward-looking

statements in this presentation are qualified by the factors affecting

forward-looking statements identified in the more detailed Cautionary Statement included

in the Appendix, which is included in the version of the presentation

materials

posted

on

our

corporate

website

at

www.pnc.com/investorevents,

and

in

our

SEC

filings.

We

provide

greater

detail

regarding

these as well as other factors in our 2013 Form 10-K and our 2014 Form 10-Qs,

including in the Risk Factors and Risk Management sections and in the Legal Proceedings

and Commitments and Guarantees Notes of the Notes To Consolidated Financial Statements in those reports, and in our subsequent

SEC filings. Our forward-looking statements may also be subject to other risks and

uncertainties, including those we may discuss in this presentation or in our SEC

filings, accessible on the SECs website at www.sec.gov and on PNCs corporate website at www.pnc.com/secfilings. We have included web

addresses in this presentation as inactive textual references only. Information on those

websites is not part of this presentation. Future events or circumstances may change

our outlook and may also affect the nature of the assumptions, risks and uncertainties to which our forward-looking

statements are subject. Forward-looking statements in this presentation speak only as of

the date of this presentation. We do not assume any duty and do not undertake to update

those statements. Actual results or future events could differ, possibly materially, from those anticipated in forward-looking

statements, as well as from historical performance.

In

this

presentation,

we

may

sometimes

refer

to

adjusted

results

to

help

illustrate

the

impact

of

certain

types

of

items.

This

information

supplements

our

results as reported in accordance with GAAP and should not be viewed in isolation from, or as

a substitute for, our GAAP results. We believe that this additional

information

and

the

reconciliations

we

provide

may

be

useful

to

investors,

analysts,

regulators

and

others

to

help

evaluate

the

impact

of

these

respective items on our operations. We may also provide information on the components of total

net interest income (purchase accounting accretion and the remainder, which we refer to

as core net interest income), on the impact of purchase accounting accretion on net interest margin (core net interest

margin (net interest margin less annualized purchase accounting accretion divided by average

interest-earning assets)), on pretax pre-provision earnings (total revenue less

noninterest expense), and on tangible book value per common share (calculated based on tangible common shareholders

equity (common shareholders

equity less goodwill and other intangible assets, other than servicing rights, net of

deferred tax liabilities on such intangible assets) divided by period-end common

shares outstanding). Where applicable, we provide GAAP reconciliations for such additional

information, including in the slides, the Appendix and/or other slides and materials on our

corporate website at www.pnc.com/investorevents and in our SEC filings. In certain

discussions, we may also provide information on yields and margins for all interest-earning assets calculated using net interest

income on a taxable-equivalent basis by increasing the interest income earned on

tax-exempt assets to make it fully equivalent to interest income earned

on

taxable

investments.

We

believe

this

adjustment

may

be

useful

when

comparing

yields

and

margins

for

all

earning

assets.

We

may

also

use

annualized, pro forma, estimated or third party numbers for illustrative or comparative

purposes only. These may not reflect actual results. This presentation may also include

discussion of other non-GAAP financial measures, which, to the extent not so qualified therein or in the Appendix, is

qualified

by

GAAP

reconciliation

information

available

on

our

corporate

website

at

www.pnc.com

under

About

PNCInvestor

Relations,

which

may

include materials from other investor presentations or in our annual, quarterly or current

reports. |

3

Focused on Executing

Difficult operating environment

Revenue growth challenged

Regulatory compliance costs increasing

Remain focused on acquiring appropriate risk-adjusted assets

Invest and grow our fee income businesses

Enhance our technologies and processes

Maintain capital management discipline

Industry Issues

PNCs Differentiation |

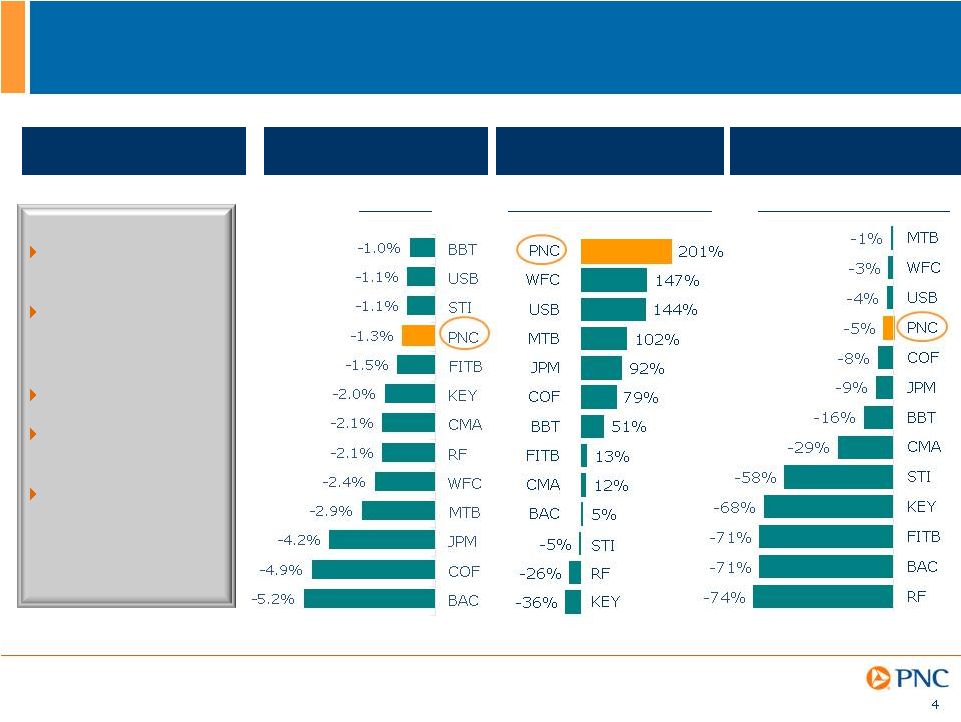

% Chg From

All Time High (3)

Variance

(1)

Performance Through the Cycle

Tangible Book Value

Per Common Share

(2)

All Time High

(3)

Closing

Stock Price vs. 9/4/14

Basel I Tier 1 Common

Capital Ratios

(1)

(1)

Source:

The

Board

of

Governors

of

the

Federal

Reserve

System

Dodd-Frank

Act

Stress

Test

(DFAST),

March

2014:

Supervisory

Stress

Test

Methodology

and

Results,

March

2014

(as

corrected).

The

variance

reflects

the

difference

under

the

Federal

Reserves

supervisory

stress

test

between

the

Basel

I

Tier

1

common

capital

ratios

reported

as

of

September

30,

2013

and

the

minimum

Basel

I

Tier

1

common

capital

ratio

projected

under

the

supervisory

severely

adverse

scenario

between

the

periods

4Q13

and

4Q15.

Ratios

were

calculated

using

the

capital

action

assumptions

contained

in

the

Federal

Reserves

Dodd-Frank

stress

testing

rules.

(2)

See

Note

A,

B

and

PNC

reconciliation

in

Appendix

for

further

details.

PNC's

book

value

per

share

was

$43.60

and

$75.62

at

12/31/07

and

6/30/14,

respectively.

(3)

See

Note

C

in

Appendix

for

further

details.

Performance

through the cycle

Disciplined risk

management

culture

Diverse franchise

Strong capital

management

Strategies to

drive growth

Franchise

Differentiation

% Chg 12/31/07 to 6/30/14

(2) |

5

Southeast

sales

(1)

+22% CAGR (12 -14)

Midwest sales

(2)

+8% CAGR (09 -14)

Drive growth in

acquired &

underpenetrated

markets

Capture more

investable assets

Redefine the Retail

Banking business

Build a stronger

Residential Mortgage

business

Bolster infrastructure &

streamline processes

Executing Our Strategic Priorities

Strategic Priorities Update

AUA

(3)

:$300B +10% (2Q14 vs. 2Q13)

Executing according to plan

Increased % of Purchase

(5)

originations to

50% of total originations in 2Q14

Fee income

(4)

+7% (2Q14 vs. 2Q13)

Noninterest expense +0% (2Q14 vs. 2Q13)

(1)

Southeast

markets

defined

as

Alabama,

Georgia,

North

Carolina,

South

Carolina

and

Florida.

Sales

for

total

Corporate

Banking

and

AMG.

AMG

refers

to

Asset

Management

Group.

(2)

Sales

for

total

Corporate

Banking

and

AMG

sales.

(3)

AUA

refers

to

client

assets

under

administration

including

both

AMG

AUA

and

brokerage

assets

of

approximately

$43

billion

for

2Q14

and

$39

billion

for

2Q13

from

Retail

Banking

Brokerage

business.

(4)

Retail

Banking

fee

income

refers

to

noninterest

income

in

the

following

categories:

service

charges

on

deposits,

brokerage,

and

consumer

services.

See

Reconcilement

in

Appendix.

(5)

A

mortgage

with

a

borrower

as

part

of

a

residential

real

estate

purchase

transaction. |

6

Building Best In Class Technology & Operations

Priorities

Activities

Key Accomplishments

YTD 2014

Establish and demonstrate

ability to recover critical

systems

Strengthening all perimeter

defenses

Implementing scanning and

monitoring capabilities

Refreshing technology

Migrating to new data centers

and infrastructure

Introduced new lean

management systems which

continuously improves

processes

Support scalable businesses and provide additional expense savings to fund investments

Simplify how we work and lower cost of managing our businesses

Deliver greater value to our customers

Reduce operational risk

Developed and began execution

of technology strategy to further

mitigate business continuity and

disaster recovery risks

90% of applications vulnerability

scanned

Expanded security monitoring to

Online banking and PNC.com

Data center location selection and

hosting strategy developed

Onboarding applications

Achieved productivity gains of

20%

Business

Continuity

Infrastructure

Modernization

Cyber Security

Process

Optimization &

Continuous

Improvement

Long-Term Benefits |

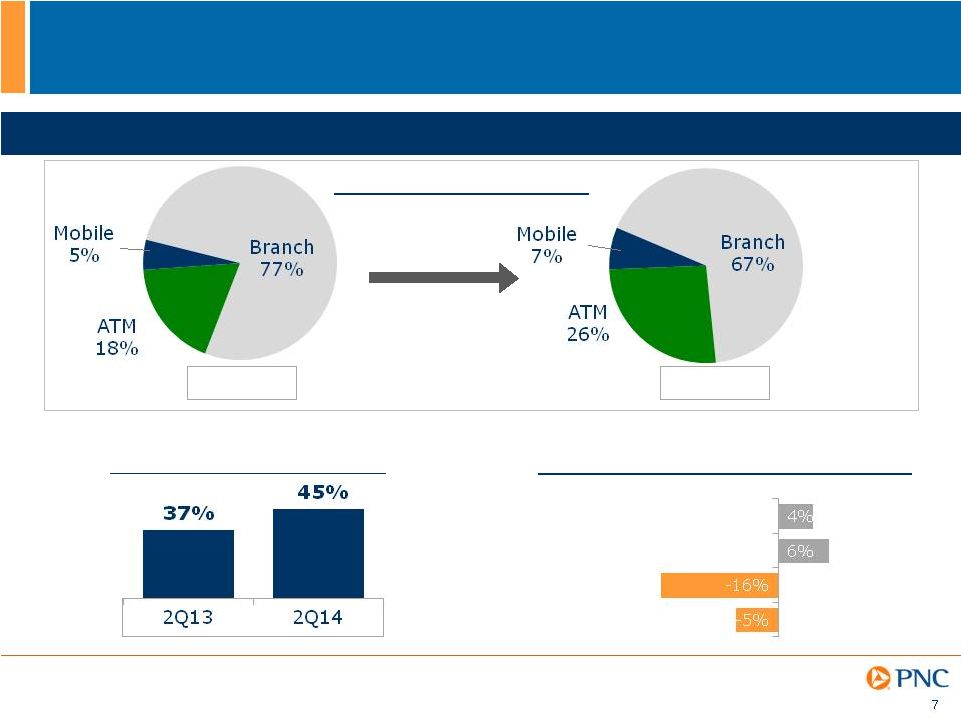

Redefining the

Retail Banking Business Digital Consumer Customers

(1)

Retail Banking Headcount (HC)

12 month change

Investment Professionals

Call Center Sales Reps.

Tellers

Total HC

(June 2013 vs. June 2014)

(1) Digital Consumer Customers represents consumer checking relationships that process the

majority of their transactions through non-teller channels.

Successfully

migrating

customers

to

self-service

ATM/Mobile

usage

increasing

2Q13

2Q14

Total deposit transactions |

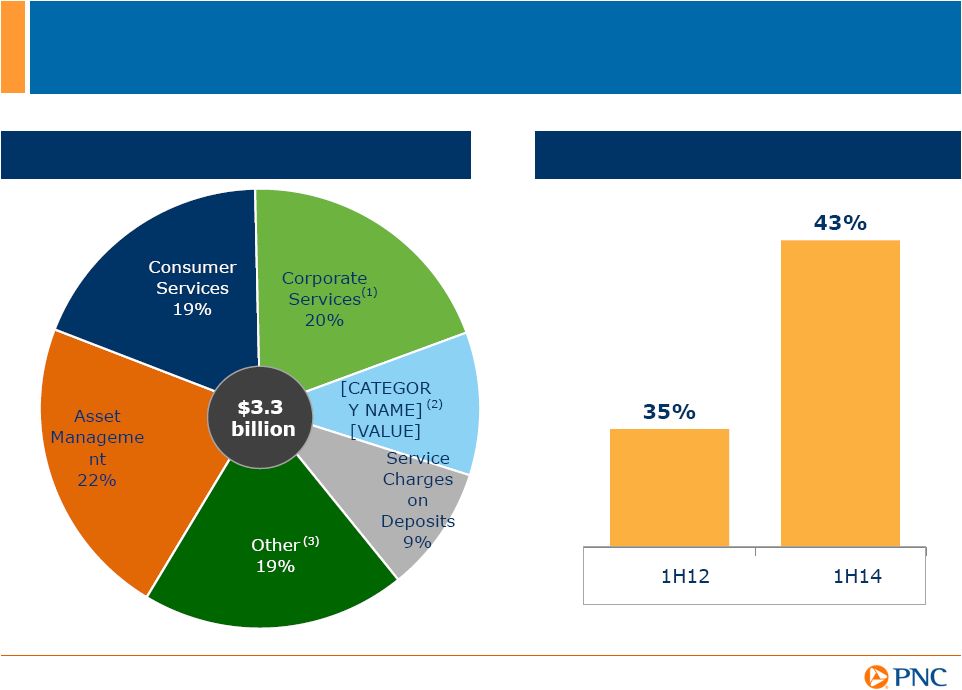

Diverse and

Higher Percentage of Noninterest Income 1H14 Noninterest Income Mix

(1)

Includes

net

commercial

mortgage

servicing

rights

valuation

gains.

(2)

Includes

benefit/provision

for

residential

mortgage

repurchase

obligations.

(3)

Other

includes

net

gains

on

sales

of

securities,

net

other-than-temporary

impairments

and

other

income.

Other

income

includes

gain

on

sale

of

a

portion

of

VISA

class

B

common

shares

and

credit

valuations

for

customer-related

derivatives

activities.

Noninterest Income to Total Revenue

8 |

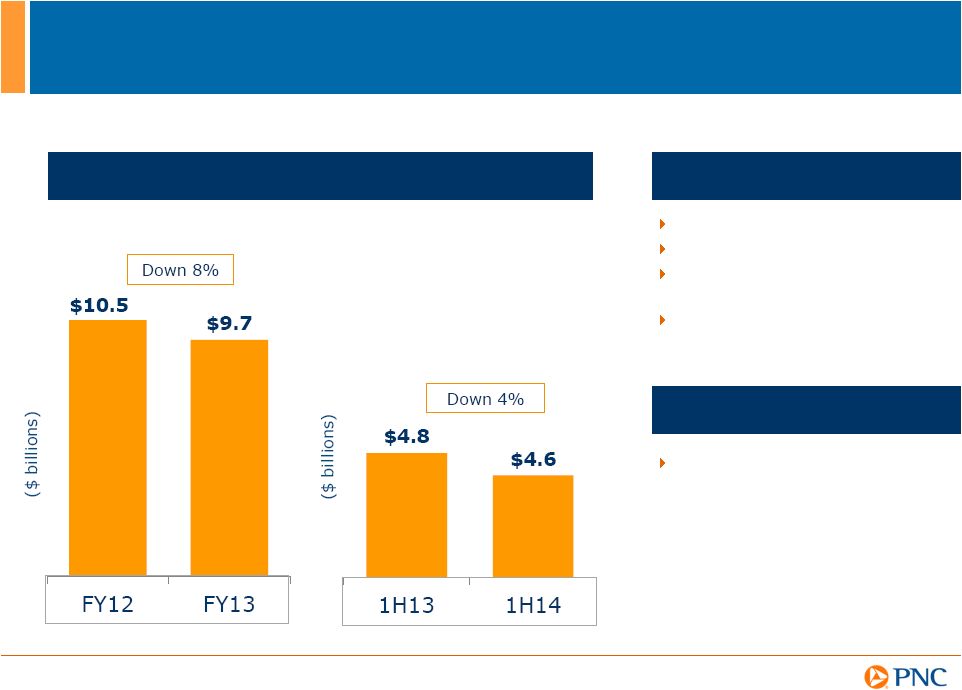

Branch

reconfiguration Process optimization

Re-engineering mortgage

servicing business

Continued focus on expense

savings initiatives through

CIP

(2)

goal of $500 million

Noninterest Expense Trends

(1)

Focused Expense Management While Investing for

Future Growth

2014 Expense Management

Opportunities

(1)

Prior

period

amounts

have

been

updated

to

reflect

the

first

quarter

2014

adoption

of

Accounting

Standards

Update

(ASU)

2014-01

related to investments in low income housing tax credits. (2) CIP refers to PNCs

Continuous Improvement Program. Investing for Future Growth

Ongoing CIP

(2)

initiatives

including cost savings from

additional efficiencies should

fund future investments

Infrastructure

Product and technology

Underpenetrated markets

9 |

10

Balance Sheet Positioned for Rising Rates

Assumptions

(1)

As

of

6/30/2014.

Reflects

the

interest

rate

risk

exposure

on

PNCs

net

interest

income.

See

2Q14

Form

10-Q

disclosure

for

further

details

on

interest

rate

exposure.

(2)

Reflects

the

percentage

change

in

net

interest

income

in

first

year

as

a

result

of

gradual

100

bps

interest

rate

increase

over

following

twelve

months.

(3)

Reflects

the

percentage

change

in

net

interest

income

in

second

year

as

a

result

of

gradual

100bps

interest

rate

increase

over

preceding

twelve

months.

Net Interest Income Sensitivity

2Q14

(1)

Deposit betas are more

conservative and higher

than historical

Assumes re-investment

yield of 1.54% on

6/30/14 and 2.54% on

6/30/15 on 4 year

average life securities

Yr1

(2)

Yr2

(3)

2Q14 10-Q

2.0%

6.8%

Yr1

Yr2

Yr3

Yr4

Invest $20 billion immediately

$210

$156

$156

156

Invest $20 billion one year forward

-

356

356

356

Impact of delaying investment

($210)

$200

$200

$200

100 Bps Parallel Increase

$ in millions |

11

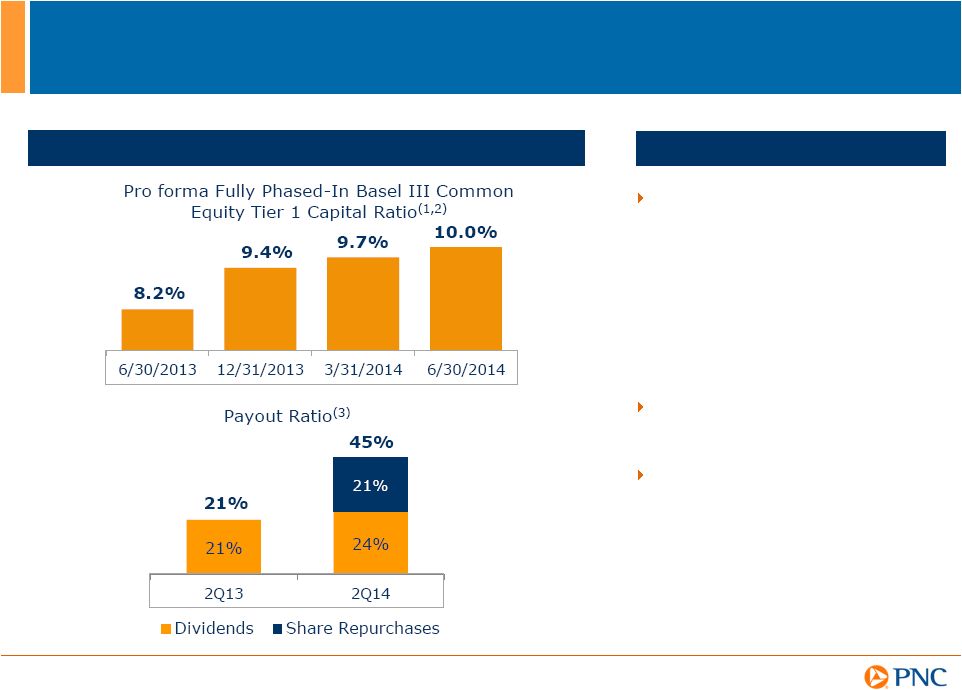

Stronger Capital Position

Capital Position Provides Capital Flexibility

Highlights

Capital priorities:

Increased quarterly common

stock dividend by 9% to $0.48

for 2Q14

Repurchased 2.6 million

common shares for $223

million in 2Q14 under our

capital plan authorization of up

to $1.5 billion of common stock

through 1Q15

(4)

(1) We previously referred to Basel III common equity Tier 1 capital ratio as the Basel III

Tier 1 common capital ratio. (2) Calculated on a pro forma basis without the benefit of the Basel III phase-in

provisions. For 2Q14, 1Q14 and 4Q13, the resulting pro forma fully phased-in Basel III

common equity Tier 1 ratios were calculated based on the standardized approach RWAs. Advanced approaches RWAs

were utilized for 2Q13. See Transitional Basel III and Pro forma

Fully Phased-In Basel III Common Equity Tier 1 Capital Ratios and related information in

the Appendix for further details. (3) Payout ratio refers to amount used to fund common

stock dividends and share repurchases as a percentage of net income. (4) For four quarter period through 1Q15, subject to factors such as market and general

economic conditions, economic capital and regulatory capital conditions, alternative uses of

capital, regulatory and contractual limitations, issuances related to employee benefit

plans and the potential impact on credit ratings.

11

Build capital to support client

growth and business

investment

Maintain appropriate capital in

light of economic uncertainty

Return excess capital to

shareholders, subject to the

CCAR process |

12

Strategies to Drive Long-Term Potential

Strategic Priorities Update

Long-Term

Potential

(1)

Incremental annual

revenue of $500M

Total investable assets

growth of $100 billion+

Fee income

(2)

growth of

mid to upper single digit

Increase product

penetration to

8%-10%

(3)

Scalable

Drive growth in acquired &

underpenetrated markets

Capture more investable assets

Redefine the Retail Banking

business

Build a stronger Residential

Mortgage business

Bolster infrastructure &

streamline processes

(1)

Refer

to

Cautionary

Statement

in

Appendix,

including

economic

and

other

assumptions.

Does

not

take

into

account

the

impact

of

potential

legal

and

regulatory

contingencies.

(2)

Retail

Banking

fee

income

refers

to

noninterest

income

in

the

following

categories:

service

charges

on

deposits,

brokerage,

and

consumer

services.

(3)

Residential

Mortgage

product

penetration

based

on

cross-sales

to

existing

Retail

Banking

households

with

current

penetration

of

6%. |

13

Well-Positioned for the Future

Opportunity to grow share in underpenetrated markets

and deepen product penetration

Focused on growing fee income businesses

Creating opportunities to drive positive operating

leverage

Stronger capital provides opportunity to return more

capital to shareholders |

14

Cautionary Statement Regarding Forward-Looking

Information

Appendix

This presentation includes snapshot

information about PNC used by way of illustration and is not intended as a full business or

financial review. It should not be viewed in isolation but rather in the context of all

of the information made available by PNC in its SEC filings. We also make statements in

this presentation, and we may from time to time make other statements, regarding our outlook for earnings,

revenues, expenses, capital and liquidity levels and ratios, asset levels, asset quality,

financial position, and other matters regarding or affecting PNC and its future

business and operations that are forward-looking statements within the meaning of the Private Securities Litigation Reform Act.

Forward-looking statements are typically identified by words such as

believe, plan,

expect,

anticipate,

see,

look,

intend,

outlook,

project,

forecast,

estimate,

goal,

will,

should

and other similar words and expressions.

Forward-looking statements are subject to numerous assumptions, risks and uncertainties,

which change over time. Forward-looking statements speak only as of the date made.

We do not assume any duty and do not undertake to update forward-looking

statements. Actual results or future events could differ, possibly materially, from

those anticipated in forward-looking statements, as well as from historical

performance. Our forward-looking statements are subject to the following principal

risks and uncertainties.

Our businesses, financial results and balance sheet values are affected by business and

economic conditions, including the following:

Changes in interest rates and valuations in debt, equity and other financial markets.

Disruptions in the liquidity and other functioning of U.S. and global financial markets.

The impact on financial markets and the economy of any changes in the credit ratings of U.S.

Treasury obligations and other U.S. government-backed debt, as well as issues

surrounding the levels of U.S. and European government debt and concerns regarding the

creditworthiness of certain sovereign governments, supranationals and financial

institutions in Europe.

Actions by the Federal Reserve, U.S. Treasury and other government agencies, including those

that impact money supply and market interest rates.

Changes in customers, suppliers

and other counterparties

performance and creditworthiness.

Slowing or reversal of the current U.S. economic expansion.

Continued residual effects of recessionary conditions and uneven

spread of positive impacts of recovery on the economy and our

counterparties, including adverse impacts on levels of unemployment, loan utilization rates,

delinquencies, defaults and counterparty ability to meet credit and other obligations.

Changes in customer preferences and behavior, whether due to changing business and economic

conditions, legislative and regulatory initiatives, or other factors.

Our forward-looking financial statements are subject to the risk that economic and

financial market conditions will be substantially different than we are currently

expecting. These statements are based on our current view that the U.S. economic expansion will speed

up to an above trend growth rate near 3.0 percent in the second half of 2014 and that

short-term interest rates will remain very low and bond yields will rise only

slowly in the latter half of 2014. These forward-looking statements also do not, unless otherwise indicated, take

into account the impact of potential legal and regulatory contingencies.

|

15

Cautionary Statement Regarding Forward-Looking

Information (continued)

Appendix

PNCs ability to take certain capital actions, including paying dividends and any plans

to increase common stock dividends, repurchase common stock under current or future

programs, or issue or redeem preferred stock or other regulatory capital instruments, is

subject to the review of such proposed actions by the Federal Reserve as part of PNCs

comprehensive capital plan for the applicable period

in

connection

with

the

regulators

Comprehensive

Capital

Analysis

and

Review

(CCAR)

process

and

to

the

acceptance

of

such

capital plan and non-objection to such capital actions by the Federal Reserve.

PNCs regulatory capital ratios in the future will depend on, among other things, the

companys financial performance, the scope and terms of final capital regulations

then in effect (particularly those implementing the Basel Capital Accords), and management actions

affecting the composition of PNCs balance sheet. In addition, PNCs ability to

determine, evaluate and forecast regulatory capital ratios, and to take actions (such as

capital distributions) based on actual or forecasted capital ratios, will be dependent at least in part

on the development, validation and regulatory approval of related models.

Legal and regulatory developments could have an impact on our ability to operate our

businesses, financial condition, results of operations, competitive position,

reputation, or pursuit of attractive acquisition opportunities. Reputational impacts could affect

matters such as business generation and retention, liquidity, funding, and ability to attract

and retain management. These developments could include:

Changes resulting from legislative and regulatory reforms, including major reform of the

regulatory oversight structure of the financial services industry and changes to laws

and regulations involving tax, pension, bankruptcy, consumer protection, and other

industry aspects, and changes in accounting policies and principles. We will be impacted by extensive reforms provided

for in the Dodd-Frank Wall Street Reform and Consumer Protection Act (the

Dodd-Frank Act) and otherwise growing out of the

most

recent

financial

crisis,

the

precise

nature,

extent

and

timing

of

which,

and

their

impact

on

us,

remains

uncertain.

Changes to regulations governing bank capital and liquidity standards, including due to the

Dodd-Frank Act and to Basel- related initiatives.

Unfavorable resolution of legal proceedings or other claims and regulatory and other

governmental investigations or other inquiries. In addition to matters relating to

PNCs current and historical business and activities, such matters may include

proceedings, claims, investigations, or inquiries relating to pre-acquisition business

and activities of acquired companies, such as National City. These matters may result

in monetary judgments or settlements or other remedies, including fines, penalties,

restitution or alterations in our business practices, and in additional expenses and

collateral costs, and may cause reputational harm to PNC.

Results of the regulatory examination and supervision process, including our failure to

satisfy requirements of agreements with governmental agencies.

Impact on business and operating results of any costs associated

with obtaining rights in intellectual property claimed by others

and of adequacy of our intellectual property protection in general.

|

16

Cautionary Statement Regarding Forward-Looking

Information (continued)

Appendix

Business and operating results are affected by our ability to identify and effectively manage

risks inherent in our businesses, including, where appropriate, through effective use

of third-party insurance, derivatives, and capital management techniques, and to

meet evolving regulatory capital and liquidity standards. In particular, our results

currently depend on our ability to manage elevated levels of impaired assets.

Business and operating results also include impacts relating to our equity interest in

BlackRock, Inc. and rely to a significant extent

on information provided to us by BlackRock. Risks and uncertainties that could affect

BlackRock are discussed in more detail by BlackRock in its SEC filings.

We grow our business in part by acquiring from time to time other financial services

companies, financial services assets and related deposits and other liabilities.

Acquisition risks and uncertainties include those presented by the nature of the business acquired,

including

in

some

cases

those

associated

with

our

entry

into

new

businesses

or

new

geographic

or

other

markets

and

risks

resulting

from our inexperience in those new areas, as well as risks and uncertainties related to the

acquisition transactions themselves, regulatory issues, and the integration of the

acquired businesses into PNC after closing. Competition can have an impact on customer

acquisition, growth and retention and on credit spreads and product pricing, which can

affect market share, deposits and revenues. Industry restructuring in the current environment

could also impact our business and financial performance through changes in counterparty

creditworthiness and performance and in the competitive and regulatory landscape. Our

ability to anticipate and respond to technological changes can also impact our ability to respond to customer needs

and meet competitive demands.

Business and operating results can also be affected by widespread natural and other disasters,

dislocations, terrorist activities, cyberattacks

or

international

hostilities

through

impacts

on

the

economy

and

financial

markets

generally

or

on

us

or

our

counterparties specifically.

We provide greater detail regarding these as well as other factors in our 2013 Form 10-K

and our 2014 Form 10-Qs, including in the Risk Factors and Risk Management sections

and the Legal Proceedings and Commitments and Guarantees Notes of the Notes To Consolidated

Financial Statements in those reports, and in our subsequent SEC

filings. Our forward-looking statements may also be subject to other

risks

and

uncertainties,

including

those

we

may

discuss

elsewhere

in

this

presentation

or

in

our

SEC

filings,

accessible

on

the

SECs website

at www.sec.gov and on our corporate website at www.pnc.com/secfilings. We have included these

web addresses as inactive textual references only. Information on these websites is not

part of this document. Any annualized, pro forma, estimated, third party or consensus

numbers in this presentation are used for illustrative or comparative purposes only and

may not reflect actual results. Any consensus earnings estimates are calculated based on the earnings projections made

by analysts who cover that company. The analysts

opinions, estimates or forecasts (and therefore the consensus earnings estimates) are

theirs alone, are not those of PNC or its management, and may not reflect PNCs or other

companys actual or anticipated results. |

17

Notes

Appendix

Explanatory Notes

(A) Tangible book value (TBV) per common share calculated based on tangible common

shareholders' equity (common shareholders' equity less goodwill and other intangible

assets, other than servicing rights, net of deferred tax liabilities on such intangible

assets) divided by period-end common shares outstanding. Peer source: SNL Datasource and company

filings. See Appendix for PNC reconciliation.

(B) Tangible book value 12/31/2007 PNC data has not been updated to reflect PNC's first

quarter 2014 adoption of Accounting Standards Update (ASU) 2014-01 related to

investments in low income housing credits. (C) All time high percent change reflects the

difference between the all time high closing stock price using the highest closing

price since 12/31/1989 as reported by SNL DataSource and the 9/4/14 closing price. |

18

Transitional Basel III and Pro forma Fully Phased-In Basel III

Common Equity Tier 1 Capital Ratios

Appendix

As a result of the staggered effective dates of the final U.S. capital rules issued in July

2013, as well as the fact that PNC remains in the parallel run qualification phase for

the advanced approaches, PNCs regulatory risk-based capital ratios during

2014 are based on the definitions of, and deductions from, capital under Basel III (as

such definitions and deductions are phased-in for 2014) and Basel I risk-weighted assets (but subject

to certain adjustments as defined by the Basel III rules). We refer to the capital ratios

calculated using these Basel III phased-in provisions and Basel I risk-weighted

assets as the Transitional Basel III ratios. These capital ratios became effective for

PNC on January 1, 2014. We provide information on the next slide regarding PNCs

Transitional Basel III common equity Tier 1 ratio and PNCs pro forma fully

phased-in Basel III common equity Tier 1 ratio. We previously referred to the

Basel III common equity Tier 1 ratio as the Basel III Tier 1 common ratio. In addition,

on the next slide we provide information regarding PNCs Basel I Tier 1 common capital

ratio, which was applicable to PNC through 2013 under the U.S. regulatory capital

rules. Common equity Tier 1 capital as defined under the Basel III rules adopted by the

U.S. banking agencies differs materially from Basel I Tier 1 common capital. For

example, under Basel III, significant common stock investments in unconsolidated

financial institutions, mortgage servicing rights and deferred tax assets must be

deducted from capital to the extent they individually exceed 10%, or in the aggregate

exceed 15%, of the institutions adjusted common equity Tier 1 capital. Also,

Basel I regulatory capital excludes accumulated other comprehensive income related to

securities currently and previously held as available for sale, as well as pension and other

postretirement plans, whereas under Basel III these items are a component of PNC's

capital. |

19

Transitional Basel III and Pro forma Fully Phased-In Basel III

Common Equity Tier 1 Capital Ratios

Appendix

Transitional Basel III

Pro forma Fully Phased-In Basel III

Dollars in millions

June 30, 2014

March 31, 2014

June 30, 2014

March 31, 2014

December 31, 2013(a)

June 30, 2013(a)

Common stock, related surplus, and retained earnings, net of treasury stock

$39,380

$38,722

$39,380

$38,722

$38,031

$36,302

Less regulatory capital adjustments:

Goodwill and disallowed intangibles, net of deferred tax liabilities

(8,923)

(8,932)

(9,262)

(9,291)

(9,321)

(9,381)

Basel III total threshold deductions

(216)

(214)

(1,075)

(1,186)

(1,386)

(2,224)

Accumulated other comprehensive income (b)

115

82

576

410

196

(241)

All other adjustments (c)

(5)

(16)

(74)

(106)

(64)

(536)

Common equity Tier 1 capital

30,351

29,642

29,545

28,549

27,456

23,920

Basel I risk-weighted assets calculated in accordance with transition rules for

2014 (d)

277,126

$

273,826

$

N/A

N/A

N/A

N/A

Estimated Basel III standardized approach risk-weighted assets (e)

N/A

N/A

295,217

293,310

291,977

N/A

Estimated Basel III advanced approaches risk-weighted assets (f)

N/A

N/A

290,063

289,441

290,080

290,838

Basel III Common equity Tier 1 capital ratio

11.0%

10.8%

10.0%

9.7%

9.4%

8.2%

Risk-weight and associated rules utilized

Basel I (with 2014

transition

adjustments)

Basel I (with

2014 transition

adjustments)

Standardized

Standardized

Standardized

Advanced

(a) Amounts have not been updated to reflect the first quarter 2014 adoption of ASU 2014-01

related to investments in low income housing tax credits. (b) Represents net adjustments

related to accumulated other comprehensive income for securities currently and previously held as available for sale, as well as

pension and other postretirement plans.

(c) Includes adjustments as required based on whether the standardized approach or advanced

approaches are utilized. (d) Includes credit and market risk-weighted assets.

(e) Basel III standardized approach risk-weighted assets were estimated based on the Basel

III standardized approach rules and include credit and market risk-weighted assets.

(f) Basel III advanced approaches risk-weighted assets were estimated based on the Basel

III advanced approach rules, and include credit, market and operational risk-weighted assets.

2013 Basel I Tier 1 Common Capital Ratios (a) (b)

Dollars in millions

Dec. 31, 2013

Jun. 30, 2013

Basel I Tier 1 common capital

$28,484

$26,668

Basel I risk-weighted assets

272,169

264,750

Basel I Tier 1 common capital ratio

10.5%

10.1%

(a) Effective January 1, 2014, the Basel I Tier 1 common capital ratio no longer applies to PNC

(except for stress testing purposes). Our 2013 Form 10-K included additional

information regarding our Basel I capital ratios. PNC utilizes the pro forma fully

phased-in Basel III capital ratios to assess its capital position (without the benefit of phase-ins), including comparison to similar estimates made by other financial

institutions. Our Basel III capital ratios and estimates may be impacted by additional

regulatory guidance or analysis, and in the case of those ratios calculated using the advanced approaches, the

ongoing evolution, validation and regulatory approval of PNCs models integral to the

calculation of advanced approaches risk-weighted assets. (b) Amounts have not been

updated to reflect the first quarter 2014 adoption of ASU 2014-01 related to investments in low income

housing tax credits. |

20

Tangible Book Value per Common Share

Appendix

Tangible Book Value per Common Share Ratio

6/30/14 vs.

12/31/07

Dollars in millions, except per share data

June 30, 2014

Dec. 31, 2007

(a)

Book value per common share (a)

75.62

$

43.60

$

73%

Tangible book value per common share

Common shareholders' equity (a)

40,261

$

14,847

$

Goodwill and Other Intangible Assets (b)

(9,590)

(8,850)

Deferred tax liabilities on Goodwill and Other Intangible Assets (b)

327

594

Tangible common shareholders' equity

30,998

$

6,591

$

Period-end common shares outstanding (in millions)

532

341

Tangible book value per common share (Non-GAAP)

58.22

$

19.36

$

201%

(b) Excludes the impact from mortgage servicing rights of $1.5 billion at June 30, 2014 and

$.7 billion at December 31, 2007. Tangible book value per common share is a non-GAAP

financial measure and is calculated based on tangible common shareholders equity

divided by period-end common shares outstanding. We believe this non-GAAP financial measure serves as a

useful tool to help evaluate the strength and discipline of a company's capital management

strategies and as an additional, conservative measure of total company value.

(a) Amounts for the 2007 period have not been updated to reflect the first quarter 2014

adoption of Accounting Standards Update (ASU) 2014-01 related to investments in low

income housing tax credits. % Change |

21

Non-GAAP to GAAP Reconcilement

Appendix

For the three months ended

$ in millions

June 30, 2014

June 30, 2013

% change

Service charges on deposits

$148

$141

Brokerage

$61

$58

Consumer Services

$248

$229

Total Retail Banking fee income

$457

$428

7%

Other

$84

$114

Total Retail Banking noninterest income, as reported

$541

$542

0%

For the six months ended

$ in millions

June 30, 2014

June 30, 2012

2 year cagr

Asset management

$726

$562

Consumer services

$613

$554

Corporate services

$644

$522

Residential mortgage

$343

$57

Deposit service charges

$303

$271

Total fee income

$2,629

$1,966

16%

Net gains on sales of securities less OTTI

$1

$47

Other

$633

$525

Total noninterest income, as reported

$3,263

$2,538

13% |

22

Peer Group of Banks

Appendix

The PNC Financial Services Group, Inc.

PNC

BB&T Corporation

BBT

Bank of America Corporation

BAC

Capital One Financial, Inc.

COF

Comerica Inc.

CMA

Fifth Third Bancorp

FITB

JPMorgan Chase

JPM

KeyCorp

KEY

M&T Bank

MTB

Regions Financial Corporation

RF

SunTrust Banks, Inc.

STI

U.S. Bancorp

USB

Wells Fargo & Co.

WFC |