EX-99.1

Published on February 11, 2014

The PNC

Financial Services Group, Inc. Credit Suisse Financial Services Forum

February 11, 2014

Exhibit 99.1 |

2

Cautionary Statement Regarding Forward-Looking

Information and Adjusted Information

Our earnings conference call presentation includes snapshot information about PNC

used by way of illustration. It is not intended as a full business or financial review

and should be viewed in the context of all of the information made available by PNC in its SEC

filings. The presentation also contains forward-looking statements regarding our

outlook for earnings, revenues, expenses, capital and liquidity levels and ratios, asset levels, asset quality, financial position, and other matters

regarding or affecting PNC and its future business and operations. Forward-looking

statements are necessarily subject to numerous assumptions, risks and uncertainties,

which change over time. The forward-looking statements in this presentation are qualified by the factors affecting forward-looking statements identified

in the more detailed Cautionary Statement included in the Appendix, which is included in the

version of the presentation materials posted on our corporate website at

www.pnc.com/investorevents, and in our SEC filings. We provide greater detail regarding these

as well as other factors in our 2012 Form 10-K and our 2013 Form 10- Qs,

including in the Risk Factors and Risk Management sections and in the Legal Proceedings and Commitments and Guarantees Notes of the Notes To Consolidated

Financial Statements in those reports, and in our subsequent SEC filings. Our

forward-looking statements may also be subject to other risks and uncertainties,

including those we may discuss in this presentation or in SEC filings, accessible on the

SECs website at www.sec.gov and on PNCs corporate website at

www.pnc.com/secfilings. We have included web addresses in this presentation as inactive

textual references only. Information on those websites is not part of this

presentation. Future events or circumstances may change our outlook and may also affect the

nature of the assumptions, risks and uncertainties to which our forward- looking

statements are subject. Forward-looking statements in this presentation speak only as of the date of this presentation. We do not assume any duty and do not

undertake to update those statements. Actual results or future events could differ, possibly

materially, from those anticipated in forward-looking statements, as well as from

historical performance. In this presentation, we may sometimes refer to adjusted results to help illustrate the impact

of certain types of items. This information supplements our results as reported in

accordance with GAAP and should not be viewed in isolation from, or as a substitute for, our GAAP results. We believe that this additional information and

the reconciliations we provide may be useful to investors, analysts, regulators and others to

help evaluate the impact of these respective items on our operations. We may also

provide information on the components of net interest income (purchase accounting accretion and the core remainder), on the impact of purchase accounting

accretion on net interest margin (core net interest margin calculated as net interest margin

less (annualized purchase accounting accretion divided by average interest-earning

assets)), on pretax pre-provision earnings (total revenue less noninterest expense), and on tangible book value per common share (calculated based

on tangible common shareholders equity (common shareholders equity less goodwill

and other intangible assets, other than servicing rights, net of deferred tax

liabilities on such intangible assets) divided by common shares outstanding). Where

applicable, we provide GAAP reconciliations for such additional information, including

in the slides, the Appendix and/or other slides and materials on our corporate website at www.pnc.com/investorevents and in our SEC filings. In certain

discussions, we may also provide information on yields and margins for all

interest-earning assets calculated using net interest income on a taxable-equivalent basis

by increasing the interest income earned on tax-exempt assets to make it fully equivalent

to interest income earned on taxable investments. We believe this adjustment may be

useful when comparing yields and margins for all earning assets. We may also use annualized, proforma, estimated or third party numbers for

illustrative or comparative purposes only. These may not reflect actual results.

This presentation may also include discussion of other non-GAAP financial measures, which,

to the extent not so qualified therein or in the Appendix, is qualified by GAAP

reconciliation information available on our corporate website at www.pnc.com under About PNCInvestor Relations.

|

3

Agenda

2013 financial performance

Strategic priorities update

Continued focus on expense management

and capital flexibility |

4

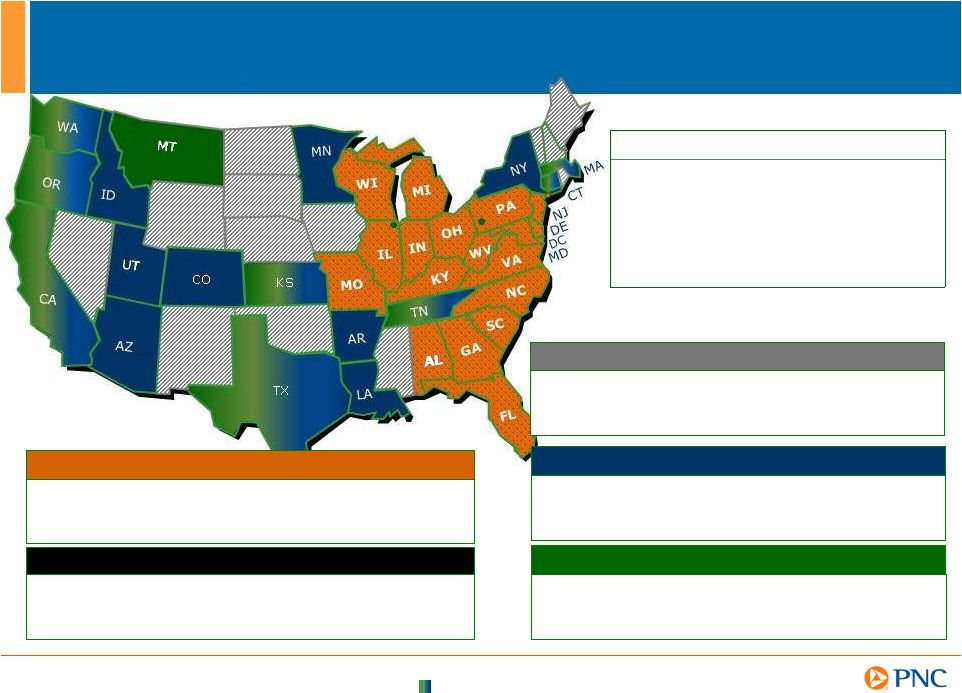

Corporate & Institutional

A leader in serving middle-market,

large corporate, government and non-

profit entities

Residential Mortgage

A primary consumer product

National distribution capabilities

(1) Rankings source: SNL DataSource; Holding companies (for assets) or Banks (for deposits,

branches and ATMs) headquartered in U.S. Assets rank excludes Morgan Stanley and

Goldman Sachs. Both Residential Mortgage Banking and Corporate & Institutional

Banking offices located in these states.

BlackRock

A leader in investment management, risk

management and advisory services

worldwide

December 31, 2013

U.S. Rank

(1)

Deposits

$221B

7

th

Assets

$320B

7

th

Branches

2,714

4

th

ATMs

7,445

3

rd

Footprint covering nearly half of the U.S.

population

Retail Banking

PNCs Leading Franchise

A top 10 U.S. bank-held wealth

manager

Asset Management |

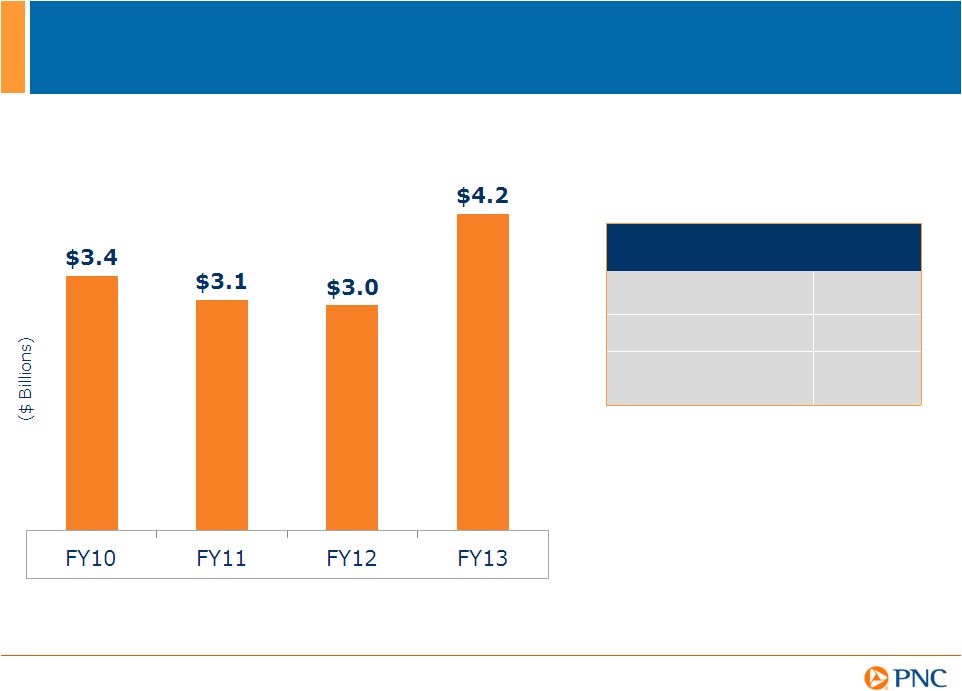

5

Record FY13 Net Income

Financial Highlights -

FY13

ROAA

(1)

1.38%

ROACE

(1)

10.88%

Noninterest income

to total revenue

43%

(1) See Note A in the Appendix for additional details. |

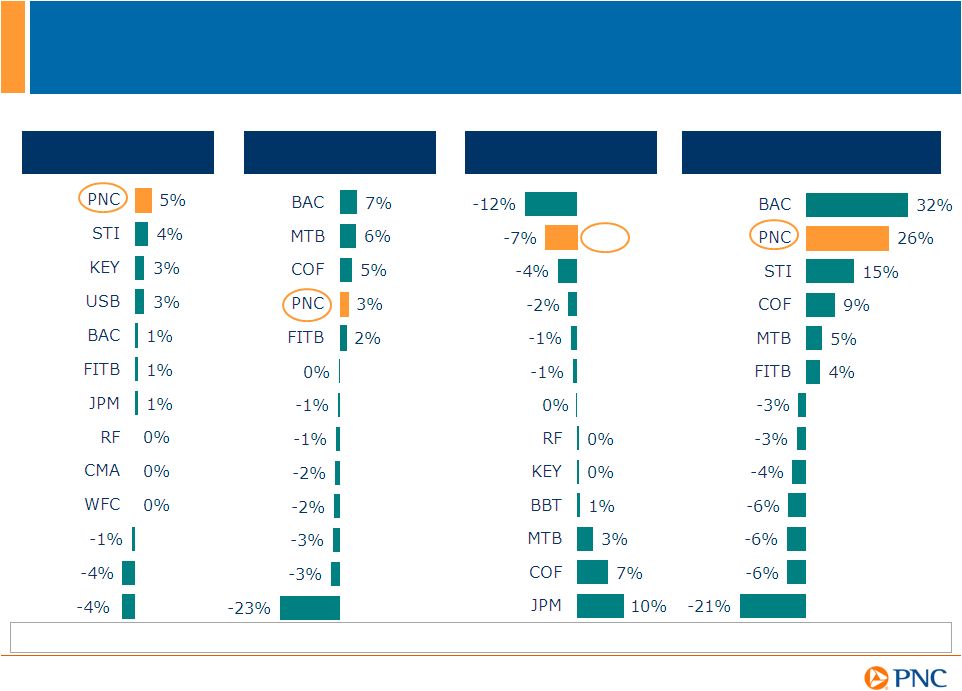

6

STI

PNC

FITB

BAC

WFC

USB

CMA

FY12-FY13

Expense growth

FY12-FY13

Loan growth

(1)

Strong Relative Performance

FY12-FY13

Pre-tax pre-provision growth

(2)

Peer Source: SNL Datasource. (1) Loan balances as of 12/31/2012 and 12/31/2013. (2) See Note B

and PNC reconciliation in the Appendix for further details. (2) Average refers to the

average of the peers listed in the graph. JPM

KEY

BBT

CMA

RF

WFC

USB

STI

KEY

CMA

WFC

USB

RF

BBT

JPM

FY12-FY13

Revenue growth

BBT

MTB

COF

Average

(2)

0%

-1%

0%

3% |

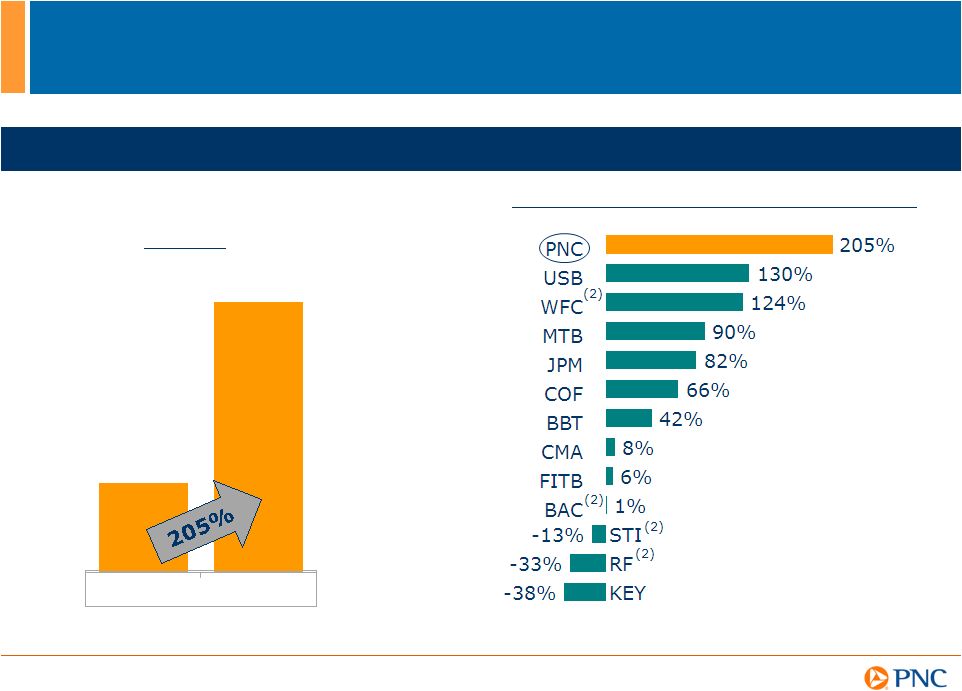

7

Value Creation Through the Cycles

(1)

Peer

source:

SNL

Datasource.

See

Note

C

and

PNC

reconciliation

in

Appendix

for

further

details.

PNCs

book

value

per

common

share

was

$43.60

at

12/31/2007

and

$72.21

at

12/31/2013.

(2)

WFC,

BAC,

STI

and

RF

tangible

book

value

per

share

for

12/31/2013

not

yet

available.

Included

in

the

graph

on

this

slide

is

the

percentage

change

in

their

reported

tangible

book

value

per

common

share

from

12/31/2007

to

9/30/13.

% change 12/31/2007 to 12/31/2013

Tangible Book Value Per Common Share

(1)

$17.93

$54.68

PNC

12/31/13

12/31/07 |

8

Drive growth in

acquired &

underpenetrated

markets

Capture more

investable assets

Build a stronger

Residential

Mortgage business

Bolster

infrastructure

&

streamline

processes

Revenue Growth and Efficiency Improvement

Opportunities

Targeted Outcomes

(1)

Increase

fee income

Expand

market share

Deepen

relationships

Improve

operating

efficiencies

Strategic Priorities

(1) Refer to Cautionary Statement in the Appendix, including economic and other assumptions.

Does not take into account impact of potential legal and regulatory or Federal debt

ceiling contingencies. Redefine

the

Retail

Banking

business |

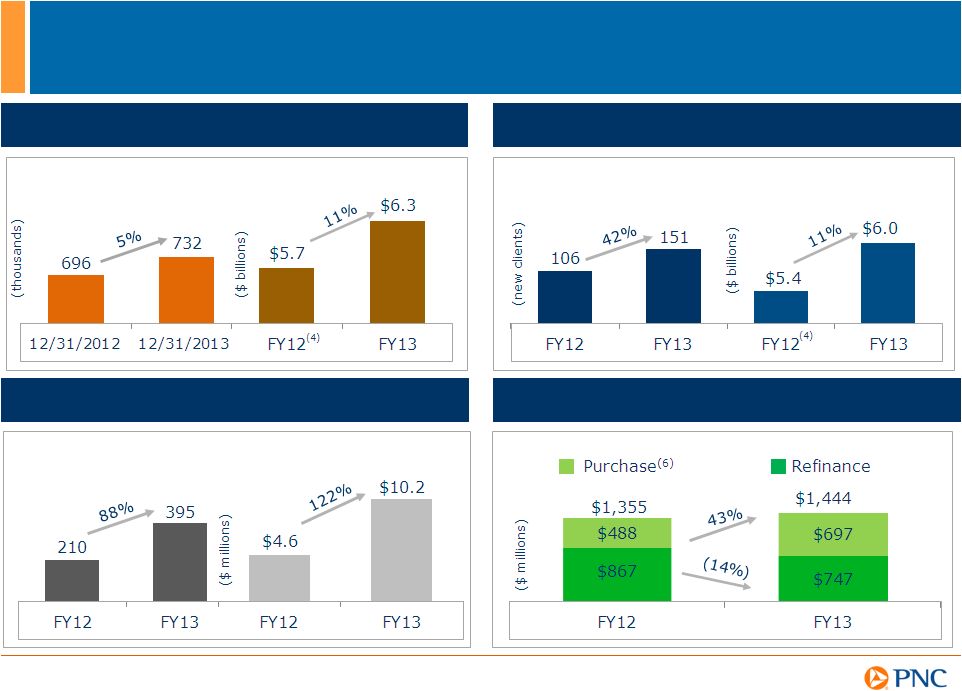

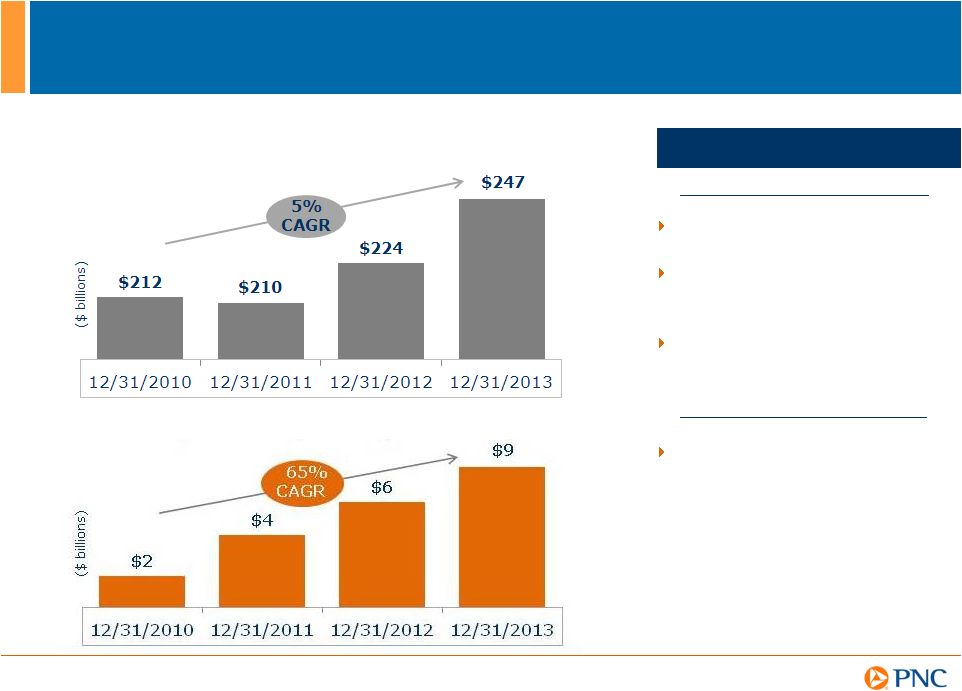

9

Deeper Penetration in Underpenetrated and Acquired

Markets

Total Corporate Banking and AMG sales

Total Corporate Banking and AMG cross-sales

AMG

refers

to

Asset

Management

Group.

(1)

Southeast

markets

defined

as

Alabama,

Georgia,

North

Carolina,

South

Carolina,

Florida

East,

Florida

West.

Includes

the

impact

of

RBC

Bank

(USA),

which

we

acquired

on

March

2,

2012.

(2)

Represents

PNCs

Corporate

Banking

clients

excluding

new

clients

of

less

than

three

years

as

of

12/31/13.

A

Corporate

Banking

primary

client

is

defined

as

a

corporate

banking

relationship

with

annual

revenue

generation

of

$50,000

or

more

or,

within

corporate

banking,

a

commercial

banking

client

relationship

with

annual

revenue

generation

of

$10,000

or

more.

Deepening client relationships

Northeast

Midwest

Northeast

Midwest

New client

Year 1

New client

Year 2

Existing

clients

(2)

Southeast

(1)

Southeast

(1)

Product Growth

Corporate Banking Primary Clients |

10

Gaining Momentum in Southeast Markets

(1)

(1)

Southeast

markets

defined

as

Alabama,

Georgia,

North

Carolina,

South

Carolina,

Florida

East,

Florida

West.

Includes

the

impact

of

RBC

Bank

(USA),

which

we

acquired

on

March

2,

2012.

(2)

Total

DDA

households

refers

to

consumer

and

small

business

relationships.

(3)

A

Corporate

Banking

primary

client

is

defined

in

Note

2

on

slide

9.

(4)

FY12

average

loans

reflect

nine

months

of

activity

as

the

RBC

Bank

(USA)

acquisition

occurred

in

1Q12.

(5)

Asset

Management

Group

primary

client

is

defined

as

a

client

relationship

with

annual

revenue

generation

of

$10,000

or

more.

(6)

A

mortgage

with

a

borrower

as

part

of

a

residential

real

estate

purchase

transaction.

Asset Management Group

Residential Mortgage Banking

Retail Banking

Corporate & Institutional Banking

Total DDA households

(2)

Corporate Banking

new primary clients

(3)

New primary clients

(5)

Average Loans

Average Loans

Referral sales

Loan origination volume |

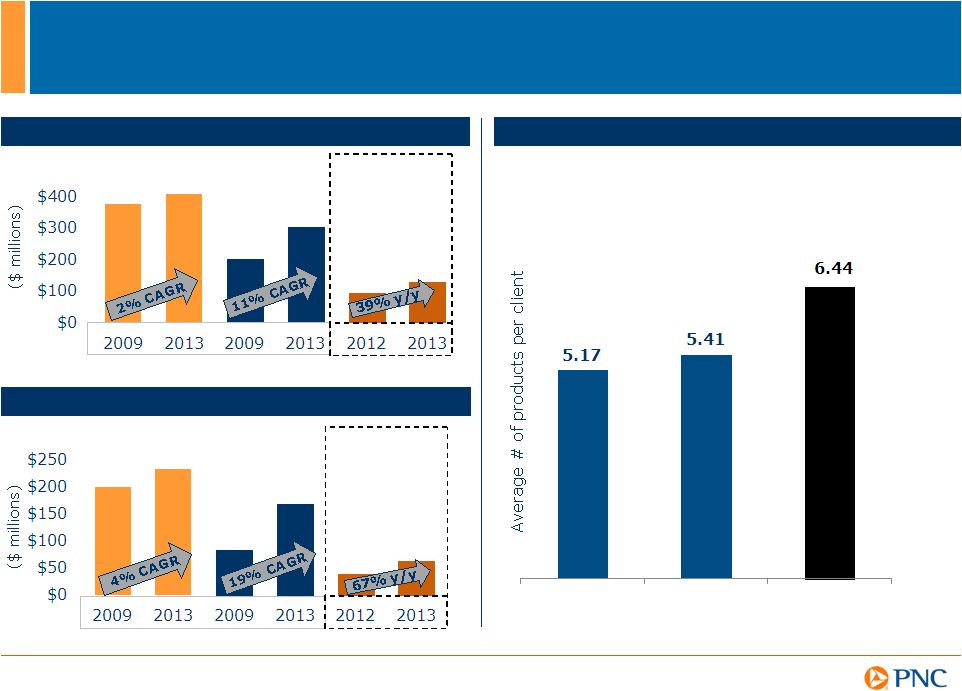

11

Capturing More Investable Assets

Highlights

Retail Banking -

Brokerage Managed Account Assets

Asset Management Group

Continued momentum in asset

growth

Managed Account assets

increased 50% from 12/31/12

to 12/31/13

Total Brokerage account

assets of $41 billion up 8% at

end of 2013 compared to end

of prior year

AUA increased 10% from

12/31/12 to 12/31/13

Core net flows

(1)

of $4.7 billion

in Discretionary AUM in 2013,

up 84% over 2012

Noninterest income increased

11% in 2013 compared to 2012

AMG -

Assets Under Administration (AUA)

AMG

refers

to

Asset

Management

Group.

AUM

refers

to

assets

under

management.

(1)

After

adjustment

to

total

net

flows

for

cyclical

client

activities.

Retail Banking Brokerage |

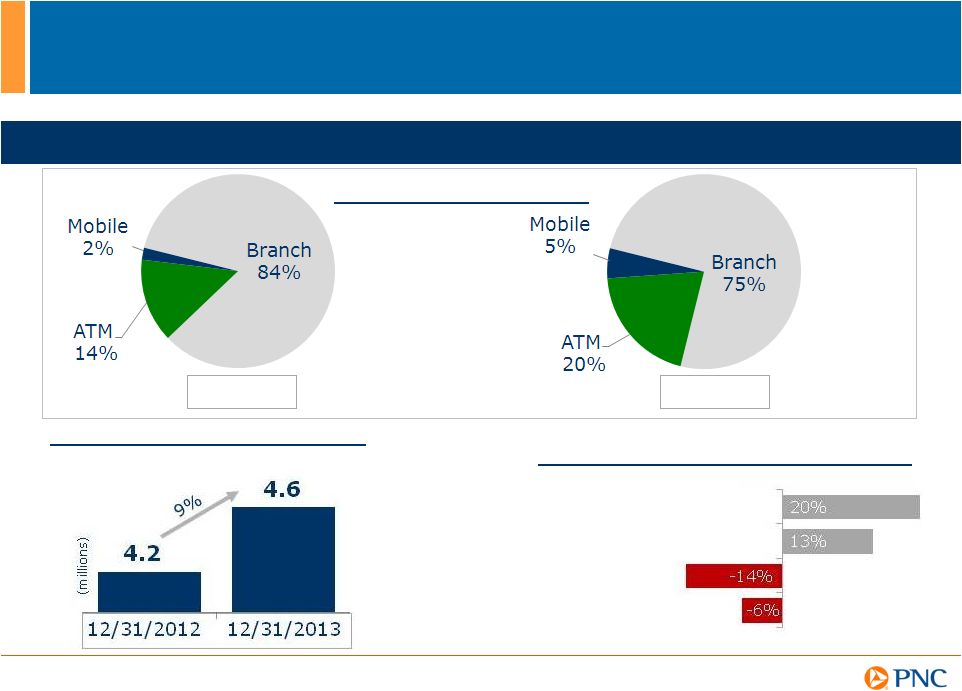

12

Successfully

migrating

customers

to

self-service

ATM/Mobile

usage

increasing

Retail Banking

Redefining the Branch Network

2012

2013

Active online banking customers

Total deposit transactions

Retail Banking Headcount (HC)

12 month change

Investment Professionals

Call Center Sales Reps.

Tellers

Total HC

(Dec. 2012 vs. Dec. 2013)

|

13

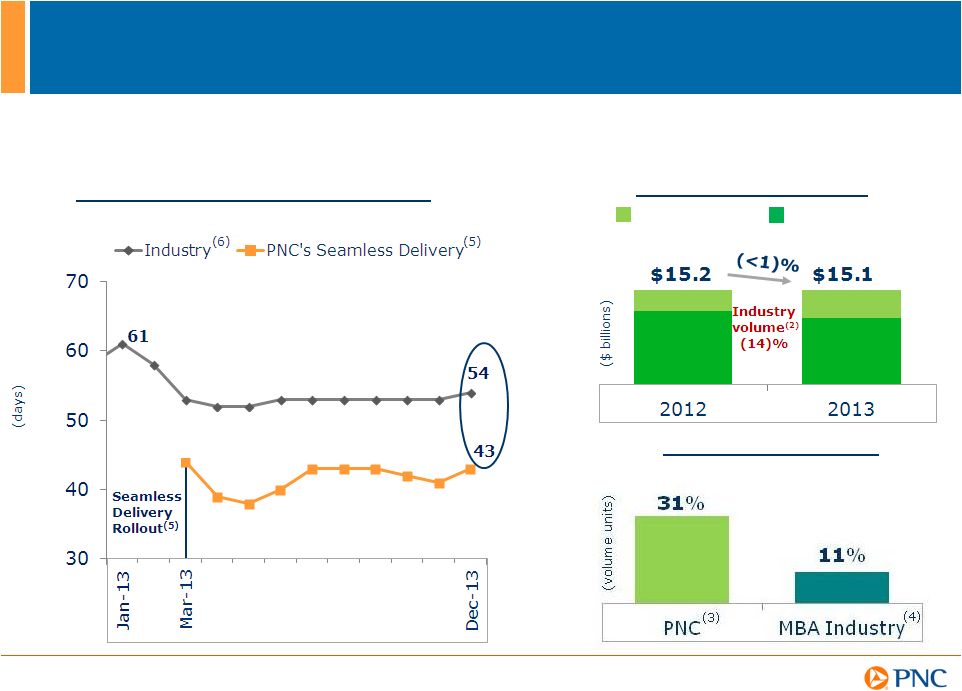

Building a Stronger Residential Mortgage Banking

Business

Closing applications faster

than industry

Purchase Applications to Close Date

(1)

A

mortgage

with

a

borrower

as

part

of

a

residential

real

estate

purchase

transaction.

(2)

Industry

loan

origination

volume

source:

Mortgage

Bankers

Association

(MBA),

January

14,

2014

publication.

(3)

PNC

Purchase

Fundings

Source:

Mortgage

Finance

data

warehouse.

(4)

MBA

Purchase

Fundings

Source:

Monthly

profile

of

state

and

national

mortgage

activity

YTD

December

2012

and

YTD

December

2013

publications.

(5)

Impact

on

the

majority

of

Purchase

applications

to

close

date

since

seamless

delivery

program

rollout

began

in

March

2013.

(6)

Industry

source:

MBA.

Growing purchase volume faster

than industry

Purchase

(1)

Fundings

Purchase

(1)

Refinance

2012 vs. 2013 volume increase

Loan Origination Volume |

14

Building Best In Class Technology & Operations

Focused Priorities

Establishing a foundation to support our scale and effectively

respond to our rapidly changing environments

Providing ability to grow with existing investments

Creating

a

competitive

advantage

improved

operational

efficiency

and business agility

Retail transformation

Process management systems

Infrastructure enhancements |

15

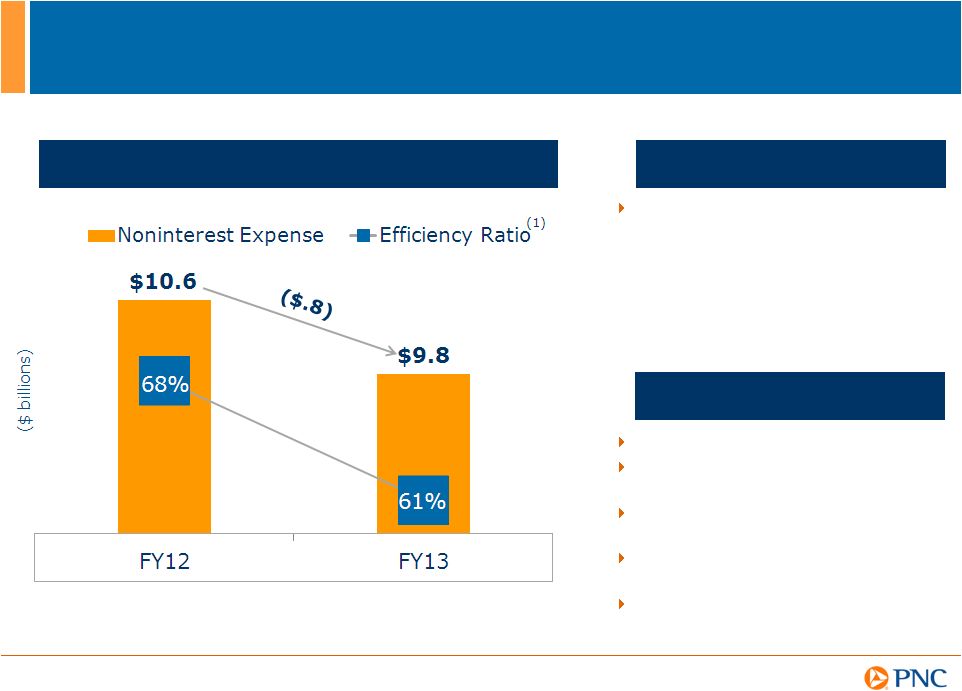

Noninterest Expense Trend

Continued Focus on Expense Management

Decreased expense reflected our

continued focus on disciplined

expense management

FY13 expenses down 7% for

first YOY decline since 2010

Exceeded $700 million FY13

CIP

(2)

targets

2013 Highlights

Lowering service delivery costs

Branch reconfiguration and

consolidations

Re-engineering mortgage

servicing business

Enhancing online investment

platform and centralized services

CIP

(2)

goal of $500 million

2014 expense management

opportunities

(1) See Note D in the Appendix for further details. (2) CIP refers to PNCs Continuous

Improvement Program. |

16

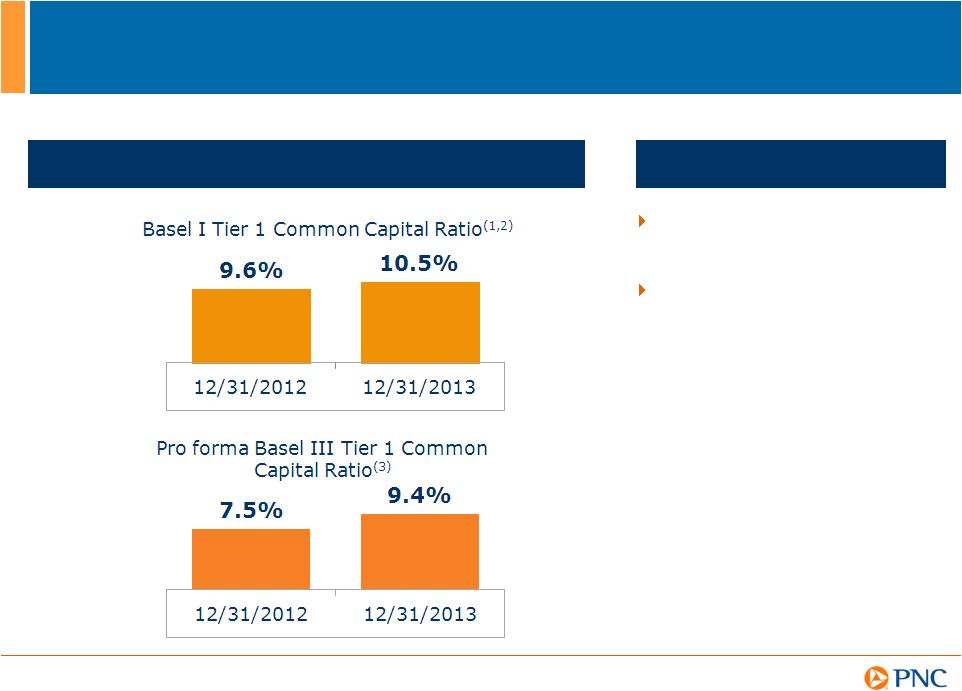

Strong Capital Improvement

Strong Capital Position Provides Capital Flexibility

Highlights

Capital levels and ratios

continued to increase

Capital priorities:

Build capital to support

client growth and

business investment

Maintain appropriate

capital in light of

economic uncertainty

Return excess capital to

shareholders, subject to

the CCAR process

(1)

Estimated

as

of

December

31,

2013.

(2)

See

Note

E

in

the

Appendix

for

further

details.

(3)

PNCs

pro

forma

Basel

III

Tier

1

common

capital

ratio

was

estimated

without

benefit

of

phase-ins

and

based

on

estimated

Basel

III

advanced

approaches

risk-weighted

assets.

See

Estimated

Pro

forma

Basel

III

Tier

1

Common

Capital

and

related

information

in

the

Appendix

for

further

details. |

17

Cautionary Statement Regarding Forward-Looking

Information

Appendix

This presentation includes snapshot

information about PNC used by way of illustration and is not intended as a full business or

financial review. It should not be viewed in isolation but rather in the context

of all of the information made available by PNC in its SEC filings. We also make

statements in this presentation, and we may from time to time make other statements, regarding our outlook for earnings, revenues, expenses,

capital and liquidity levels and ratios, asset levels, asset quality, financial position, and

other matters regarding or affecting PNC and its future business and operations that

are forward-looking statements within the meaning of the Private Securities Litigation Reform Act. Forward-looking statements are typically

identified by words such as believe,

plan,

expect,

anticipate,

see,

look,

intend,

outlook,

project,

forecast,

estimate,

goal,

will,

should

and other similar words and expressions. Forward-looking statements are subject to

numerous assumptions, risks and uncertainties, which change over time.

Forward-looking

statements

speak

only

as

of

the

date

made.

We

do

not

assume

any

duty

and

do

not

undertake

to

update

forward-looking

statements.

Actual

results

or

future

events

could

differ,

possibly

materially,

from

those

anticipated

in

forward-looking

statements,

as

well

as

from

historical

performance.

Our forward-looking statements are subject to the following principal risks and

uncertainties. Our

businesses,

financial

results

and

balance

sheet

values

are

affected

by

business

and

economic

conditions,

including

the

following:

Changes in interest rates and valuations in debt, equity and other financial markets.

Disruptions in the liquidity and other functioning of U.S. and global financial

markets.

The

impact

on

financial

markets

and

the

economy

of

any

changes

in

the

credit

ratings

of

U.S.

Treasury

obligations

and

other

U.S.

government-

backed

debt,

as

well

as

issues

surrounding

the

levels

of

U.S.

and

European

government

debt

and

concerns

regarding

the

creditworthiness

of

certain

sovereign

governments,

supranationals

and

financial

institutions

in

Europe.

Actions

by

the

Federal

Reserve,

U.S.

Treasury

and

other

government

agencies,

including

those

that

impact

money

supply

and

market

interest

rates.

Changes

in

customers,

suppliers

and

other

counterparties

performance

and

creditworthiness.

Slowing

or

reversal

of

the

current

U.S.

economic

expansion.

Continued

residual

effects

of

recessionary

conditions

and

uneven

spread

of

positive

impacts

of

recovery

on

the

economy

and

our

counterparties,

including

adverse

impacts

on

levels

of

unemployment,

loan

utilization

rates,

delinquencies,

defaults

and

counterparty

ability

to

meet

credit

and

othe

r obligations.

Changes

in

customer

preferences

and

behavior,

whether

due

to

changing

business

and

economic

conditions,

legislative

and

regulatory

initiatives,

or

other factors.

Our forward-looking

financial

statements

are

subject

to

the

risk

that

economic

and

financial

market

conditions

will

be

substantially

different

than

we

are

currently

expecting.

These

statements

are

based

on

our

current

view

that

the

U.S.

economic

expansion

will

speed

up

to

a

trend

growth

rate

near

2.5

percent

in

2014

as

drags

from

Federal

fiscal

restraint

subside,

and

that

short-term

interest

rates

will

remain

very

low

and

bond

yields

will

rise

only

slowly

in

2014.

These

forward-

looking

statements

also

do

not,

unless

otherwise

indicated,

take

into

account

the

impact

of

potential

legal

and

regulatory

contingencies

or

the

potential

impacts

of

the

Congress

failing

to

timely

address

the

authorized

level

of

the

Federal

borrowing

debt

ceiling. |

18

Cautionary Statement Regarding Forward-Looking

Information (continued)

Appendix

PNCs ability to take certain capital actions, including paying dividends and any plans to increase common stock dividends,

repurchase

common stock under

current or future programs, or issue or redeem preferred stock or other regulatory capital instruments, is subject to

the review of such proposed actions by the Federal Reserve as part of PNCs comprehensive

capital plan for the applicable period in connection

with

the

regulators

Comprehensive

Capital

Analysis

and

Review

(CCAR)

process

and

to

the

acceptance

of

such

capital

plan

and

non-objection

to

such

capital

actions

by

the

Federal

Reserve

PNCs regulatory capital ratios in the future will depend on, among other things, the companys financial performance, the scope and terms

of final capital regulations then in effect (particularly those implementing the Basel Capital

Accords), and management actions affecting the composition

of

PNCs

balance

sheet.

In

addition,

PNCs

ability

to

determine,

evaluate

and

forecast

regulatory

capital

ratios,

and

to

take

actions (such as capital distributions) based on actual or forecasted capital ratios, will be

dependent on the ongoing development, validation and regulatory approval of related

models. Legal

and

regulatory

developments

could

have

an

impact

on

our

ability

to

operate

our

businesses,

financial

condition,

results

of

operations,

competitive

position,

reputation,

or

pursuit

of

attractive

acquisition

opportunities.

Reputational

impacts

could

affect

matters

such

as

business

generation

and

retention,

liquidity,

funding,

and

ability

to

attract

and

retain

management.

These

developments

could

include:

Changes resulting from legislative and regulatory reforms, including major reform of the

regulatory oversight structure of the financial services industry and changes to laws

and regulations involving tax, pension, bankruptcy, consumer protection, and other

industry aspects, and changes in accounting policies and principles. We will be impacted by extensive reforms provided for

in the Dodd-Frank Wall Street Reform and Consumer Protection Act (the

Dodd-Frank Act) and otherwise growing out of the most recent financial

crisis, the precise nature, extent and timing of which, and their impact on us, remains uncertain.

Changes to regulations governing bank capital and liquidity standards, including due to the

Dodd-Frank Act and to Basel-related initiatives.

Unfavorable

resolution

of

legal

proceedings

or

other

claims

and

regulatory

and

other

governmental

investigations

or

other

inquiries.

In

addition

to

matters

relating

to

PNCs

business

and

activities,

such

matters

may

include

proceedings,

claims,

investigations,

or

inquiries

relating

to

pre-acquisition

business

and

activities

of

acquired

companies,

such

as

National

City.

These

matters

may

result

in

monetary

judgments

or

settlements

or

other

remedies,

including

fines,

penalties,

restitution

or

alterations

in

our

business

practices,

and

in

additional

expenses

and

collateral

costs,

and

may

cause

reputational

harm

to

PNC.

Results

of

the

regulatory

examination

and

supervision

process,

including

our

failure

to

satisfy

requirements

of

agreements

with

governmental

agencies.

Impact

on

business

and

operating

results

of

any

costs

associated

with

obtaining

rights

in

intellectual

property

claimed

by

others

and

of

adequacy

of

our

intellectual

property

protection

in

general. |

19

Cautionary Statement Regarding Forward-Looking

Information (continued)

Appendix

Business

and

operating

results

are

affected

by

our

ability

to

identify

and

effectively

manage

risks

inherent

in

our

businesses,

including,

where

appropriate,

through

effective

use

of

third-party

insurance,

derivatives,

and

capital

management

techniques,

and

to

meet

evolving

regulatory

capital

and

liquidity

standards.

In

particular,

our

results

currently

depend

on

our

ability

to

manage

elevated

levels

of

impaired

assets.

Business

and

operating

results

also

include

impacts

relating

to

our

equity

interest

in

BlackRock,

Inc.

and

rely

to

a

significant

extent

on

information

provided

to

us

by

BlackRock.

Risks

and

uncertainties

that

could

affect

BlackRock

are

discussed

in

more

detail

by

BlackRock

in

its

SEC

filings.

We

grow

our

business

in

part

by

acquiring

from

time

to

time

other

financial

services

companies,

financial

services

assets

and

related

deposits

and

other

liabilities.

Acquisition

risks

and

uncertainties

include

those

presented

by

the

nature

of

the

business

acquired,

including

in

some

cases

those

associated

with

our

entry

into

new

businesses

or

new

geographic

or

other

markets

and

risks

resulting

from

our

inexperience

in

those

new

areas,

as

well

as

risks

and

uncertainties

related

to

the

acquisition

transactions

themselves,

regulatory

issues,

and

the

integration

of

the

acquired

businesses

into

PNC

after

closing.

Competition

can

have

an

impact

on

customer

acquisition,

growth

and

retention

and

on

credit

spreads

and

product

pricing,

which

can

affect

market

share,

deposits

and

revenues.

Industry

restructuring

in

the

current

environment

could

also

impact

our

business

and

financial

performance

through

changes

in

counterparty

creditworthiness

and

performance

and

in

the

competitive

and

regulatory

landscape.

Our

ability

to

anticipate

and

respond

to

technological

changes

can

also

impact

our

ability

to

respond

to

customer

needs

and

meet

competitive

demands.

Business

and

operating

results

can

also

be

affected

by

widespread

natural

and

other

disasters,

dislocations,

terrorist

activities,

cyberattacks

or

international

hostilities

through

impacts

on

the

economy

and

financial

markets

generally

or

on

us

or

our

counterparties

specifically.

We

provide

greater

detail

regarding

these

as

well

as

other

factors

in

our

2012

Form

10-K

and

our

2013

Form

10-Qs,

including

in

the

Risk

Factors

and

Risk

Management

sections

and

the

Legal

Proceedings

and

Commitments

and

Guarantees

Notes

of

the

Notes

To

Consolidated

Financial

Statements

in

those

reports,

and

in

our

subsequent

SEC

filings.

Our

forward-looking

statements

may

also

be

subject

to

other

risks

and

uncertainties,

including

those

we

may

discuss

elsewhere

in

this

presentation

or

in

SEC

filings,

accessible

on

the

SECs

website

at

www.sec.gov

and

on

our

corporate

website

at

www.pnc.com/secfilings.

We

have

included

these

web

addresses

as

inactive

textual

references

only.

Information

on

these

websites

is

not

part

of

this

document.

Any

annualized,

proforma,

estimated,

third

party

or

consensus

numbers

in

this

presentation

are

used

for

illustrative

or

comparative

purposes

only

and

may

not

reflect

actual

results.

Any

consensus

earnings

estimates

are

calculated

based

on

the

earnings

projections

made

by

analysts

who

cover

that

company.

The

analysts

opinions,

estimates

or

forecasts

(and

therefore

the

consensus

earnings

estimates)

are

theirs

alone,

are

not

those

of

PNC

or

its

management,

and

may

not

reflect

PNCs

or

other

companys

actual

or

anticipated

results. |

20

Notes

Appendix

Explanatory Notes

(B) Pretax pre-provision earnings is defined as total revenue less noninterest expense. We

believe that pretax pre-provision earnings, a non-GAAP measure, is useful as a

tool to help evaluate the ability to provide for credit costs through operations. (A)

ROAA is Return on Average Assets and ROACE is Return on Average Common Shareholders' Equity.

(E) Basel I Tier 1 common capital ratio is period-end Basel I Tier 1 common capital

divided by period-end Basel I risk-weighted assets.

(D) Efficiency ratio calculated as noninterest expense divided by total revenue.

(C) Tangible book value per common share calculated based on tangible common shareholders'

equity (common shareholders' equity less goodwill and other intangible assets, other

than servicing rights, net of deferred tax liabilities on such intangible assets)

divided by common shares outstanding. Peer source: SNL Datasource. PNC's book value per share was $43.60 and $72.21

at 12/31/07 and 12/31/13, respectively. See Appendix, Slide 25 for PNC reconciliation.

|

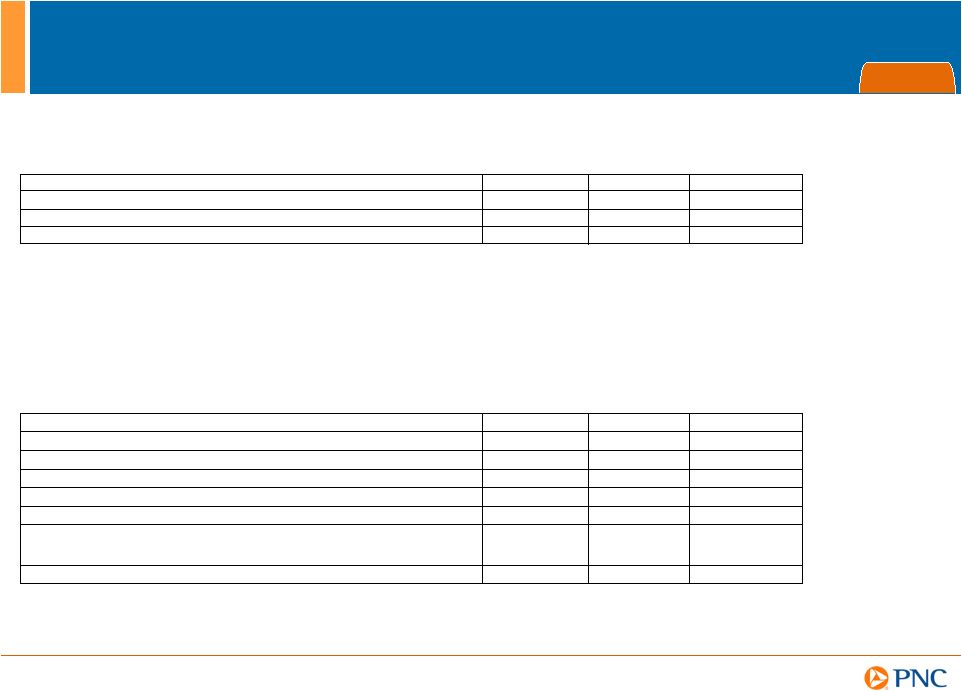

21

Estimated Pro forma Basel III Tier I Common Capital

Appendix

Basel I Tier 1 Common Capital Ratio

Dollars in millions

Dec. 31, 2013 (a)

Sept. 30, 2013

Dec. 31, 2012

Basel I Tier 1 common capital

$28,488

$27,540

$24,951

Basel I risk-weighted assets

271,192

266,698

260,847

Basel I Tier 1 common capital ratio

10.5%

10.3%

9.6%

(a) Estimated as of December 31, 2013.

Estimated Pro forma Basel III Tier 1 Common Capital Ratio

Dollars in millions

Dec. 31, 2013

Sept. 30, 2013

Dec. 31, 2012

Basel I Tier 1 common capital

$28,488

$27,540

$24,951

Less regulatory capital adjustments:

Basel III quantitative limits

(1,398)

(2,011)

(2,330)

Accumulated other comprehensive income (a)

196

(231)

276

All other adjustments

144

(49)

(396)

Estimated Basel III Tier 1 common capital

$27,430

$25,249

$22,501

Estimated Basel III advanced approaches risk-weighted assets

290,906

289,063

301,006

Pro forma Basel III Tier 1 common capital ratio

9.4%

8.7%

7.5%

(a) Represents net adjustments related to accumulated other comprehensive income for available

for sale securities and pension and other postretirement benefit plans. We provide

information below regarding PNCs pro forma fully phased-in Basel III Tier 1 common capital ratio and how it differs from the Basel I

Tier 1 common capital ratio. This Basel III ratio is calculated using PNC's estimated

risk-weighted assets under the Basel III advanced approaches.

Tier 1 common capital as defined under the Basel III rules differs materially from Basel I.

For example, under Basel III, significant common stock investments in unconsolidated

financial institutions, mortgage servicing rights and deferred tax assets must be deducted from capital to the

extent they individually exceed 10%, or in the aggregate exceed 15%, of the institution's

adjusted Tier 1 common capital. Also, Basel I regulatory capital excludes certain other

comprehensive income related to both available for sale securities and pension and other

postretirement plans, whereas under Basel III these items are a component of PNC's capital.

Basel III risk-weighted assets were estimated under the advanced approaches

included in the Basel III rules and application of Basel II.5, and reflect credit, market and operational risk.

PNC utilizes this capital ratio estimate to assess its Basel III capital position (without the

benefit of phase-ins), including comparison to similar estimates made by other

financial institutions. This Basel III capital estimate is likely to be impacted by any additional regulatory guidance and

the ongoing evolution, validation and regulatory approval of PNC's models integral to the

calculation of advanced approaches risk-weighted assets.

|

22

Non-GAAP to GAAP Reconcilement

Appendix

$ in millions

Dec. 31, 2013

Dec. 31, 2012

% Change

Net interest income

$9,147

$9,640

-5%

Noninterest income

$6,865

$5,872

17%

Total revenue

$16,012

$15,512

3%

Noninterest expense

($9,801)

($10,582)

-7%

Pretax pre-provision earnings (1)

$6,211

$4,930

26%

Net income

$4,227

$3,001

41%

(1) PNC believes that pretax, pre-provision earnings, a non-GAAP measure, is

useful as a tool to help evaluate the ability to provide for credit costs through

operations.

For

the year ended |

23

Non-GAAP to GAAP Reconcilement

Appendix

$ in millions

Dec. 31, 2013

Dec. 31, 2012

% change

Asset management

$1,342

$1,169

Consumer services

$1,253

$1,136

Corporate services

$1,210

$1,166

Residential mortgage

$871

$284

Deposit service charges

$597

$573

Total fee income, as reported

$5,273

$4,328

22%

Residential mortgage

($871)

($284)

$4,402

$4,044

9%

Fee income, adjusted for Residential mortgage

For

the year ended

$ in millions

Dec. 31, 2013

Dec. 31, 2012

% change

Asset management

$1,342

$1,169

Consumer services

$1,253

$1,136

Corporate services

$1,210

$1,166

Residential mortgage

$871

$284

Deposit service charges

$597

$573

Total fee income, as reported

$5,273

$4,328

22%

Net gains on sales of securities less net OTTI

$83

$93

Other

$1,509

$1,451

Total noninterest income, as reported

$6,865

$5,872

17%

For

the year ended |

24

Non-GAAP to GAAP Reconcilement

Appendix

Tangible Book Value per Common Share Ratio

Dollars in millions, except per share data

Dec. 31, 2013

Dec. 31, 2007

Change

Book value per common share

72.21

$

43.60

$

Tangible book value per common share

Common shareholders' equity

38,467

$

14,847

$

Goodwill and Other Intangible Assets (a)

(9,654)

(8,853)

Deferred tax liabilities on Goodwill and

Other Intangible Assets (a) 333

119

Tangible common

shareholders' equity 29,146

$

6,113

$

Period-end common shares outstanding (in

millions) 533

341

Tangible book value

per common share 54.68

$

17.93

$

205%

(a) Excludes the impact from mortgage servicing rights of $1.6 billion at December 31, 2013

and $701 million at December 31, 2007. PNC's tangible book value per common share at

December 31, 2007 and December 31, 2013 without including the impact of deferred tax

liabilities on goodwill and other intangible assets other than mortgage servicing rights would

have been $17.58 and $54.06, respectively. Tangible book value per common share is a

non-GAAP financial measure and is calculated based on tangible common shareholders' equity

divided by period-end common shares outstanding. We believe this non-GAAP financial

measure serves as a useful tool to help evaluate the strength and discipline of a

company's capital management strategies and as an additional, conservative measure of total company value. |

25

Peer Group of Banks

Appendix

The PNC Financial Services Group, Inc.

PNC

BB&T Corporation

BBT

Bank of America Corporation

BAC

Capital One Financial, Inc.

COF

Comerica Inc.

CMA

Fifth Third Bancorp

FITB

JPMorgan Chase

JPM

KeyCorp

KEY

M&T Bank

MTB

Regions Financial Corporation

RF

SunTrust Banks, Inc.

STI

U.S. Bancorp

USB

Wells Fargo & Co.

WFC |