SLIDE PRESENTATION

Published on September 10, 2012

The PNC

Financial Services Group, Inc. Barclays Global Financial Services

Conference

September 10, 2012

Exhibit 99.1 |

2

Cautionary Statement Regarding Forward-Looking

Information and Adjusted Information

This presentation includes snapshot information about PNC used by way of

illustration. It is not intended as a full business or financial review and

should be viewed in the context of all of the information made available by PNC in its SEC

filings. The presentation also contains forward-looking statements regarding

our outlook for earnings, revenues, expenses, capital levels and ratios, liquidity levels, asset levels, asset quality, financial

position, and other matters regarding or affecting PNC and its future business and

operations. Forward-looking statements are necessarily subject to numerous

assumptions, risks and uncertainties, which change over time.

The forward-looking statements in this presentation are qualified by the factors affecting

forward-looking statements identified in the more detailed Cautionary Statement

included in the Appendix, which is included in the version of the presentation materials posted on our corporate website at

www.pnc.com/investorevents. We provide greater detail regarding these as well as other

factors in our 2011 Form 10-K, as amended by Amendment No. 1 thereto, and 2012 Form

10-Qs, including in the Risk Factors and Risk Management sections and in the Legal Proceedings and Commitments and

Guarantees Notes of the Notes to Consolidated Financial Statements in those reports, and in

our subsequent SEC filings. Our forward-looking statements may also be

subject to other risks and uncertainties, including those we may discuss in this presentation or in SEC filings, accessible on

the SECs website at www.sec.gov and on PNCs corporate website at

www.pnc.com/secfilings. We have included web addresses in this presentation as

inactive textual references only. Information on these websites is not part of this presentation.

Future events or circumstances may change our outlook and may also affect the nature of the

assumptions, risks and uncertainties to which our forward-looking statements are

subject. Forward-looking statements in this presentation speak only as of the date of this presentation. We do not

assume any duty and do not undertake to update those statements. Actual results or

future events could differ, possibly materially, from those anticipated in

forward-looking statements, as well as from historical performance.

In this presentation, we sometimes refer to adjusted results to help illustrate the impact of

certain types of items, such as provisions for residential mortgage repurchase

obligations, non-cash charges related to redemptions of trust preferred securities, expenses for residential mortgage

foreclosure-related matters, legal, regulatory and OREO costs, and integration

costs. This information supplements our results as reported in accordance with

GAAP and should not be viewed in isolation from, or as a substitute for, our GAAP results. We believe that this additional information

and the reconciliations we provide may be useful to investors, analysts, regulators and others

as they evaluate the impact of these respective items on our results for the periods

presented due to the extent to which the items may not be indicative of our ongoing operations. We may also provide

information on pretax pre-provision earnings (total revenue less noninterest expense) and

on tangible book value per share (calculated as book value per share less total

intangible assets, other than servicing rights, per share). We believe that pretax pre-provision earnings, a non-GAAP measure, is

useful as a tool to help evaluate the ability to provide for credit costs through operations.

And we believe that tangible book value per share, a non- GAAP measure, is useful as

a tool to help to better evaluate growth of the companys business apart from the amount, on a per share basis, of

intangible assets other than servicing rights included in book value. Where applicable, we

provide GAAP reconciliations for such additional information, including in the Appendix

and/or other slides and materials on our corporate website at www.pnc.com/investorevents.

In certain discussions, we may also provide information on yields and margins for all

interest-earning assets calculated using net interest income on a

taxable-equivalent basis by increasing the interest income earned on tax-exempt assets

to make it fully equivalent to interest income earned on taxable investments. We

believe this adjustment may be useful when comparing yields and margins for all earning assets. We may also use

annualized, proforma, estimated or third party numbers for illustrative or comparative

purposes only. These may not reflect actual results.

This presentation may also include discussion of other non-GAAP financial measures, which,

to the extent not so qualified therein or in the Appendix, is qualified by GAAP

reconciliation information available on our corporate website at www.pnc.com under About PNCInvestor Relations.

|

DRAFT

3

Navigating The Current Environment

Revenue

growth

Mortgage-

related issues

Manage risks and

capital

Global

economy

Control costs while

investing for growth

Regulatory

change

Grow customers and

quality revenues

Industry challenges

PNCs priorities |

DRAFT

4

Launching New Products That Enhance Customer

Experience

Investing in technology across all

customer segments

Product innovation driving customer

growth

PNCs customer service differentiation:

Information organized based on

how customers think

Integrated experience

Giving customers choice

Driven by product innovation

Future service delivery model

SM |

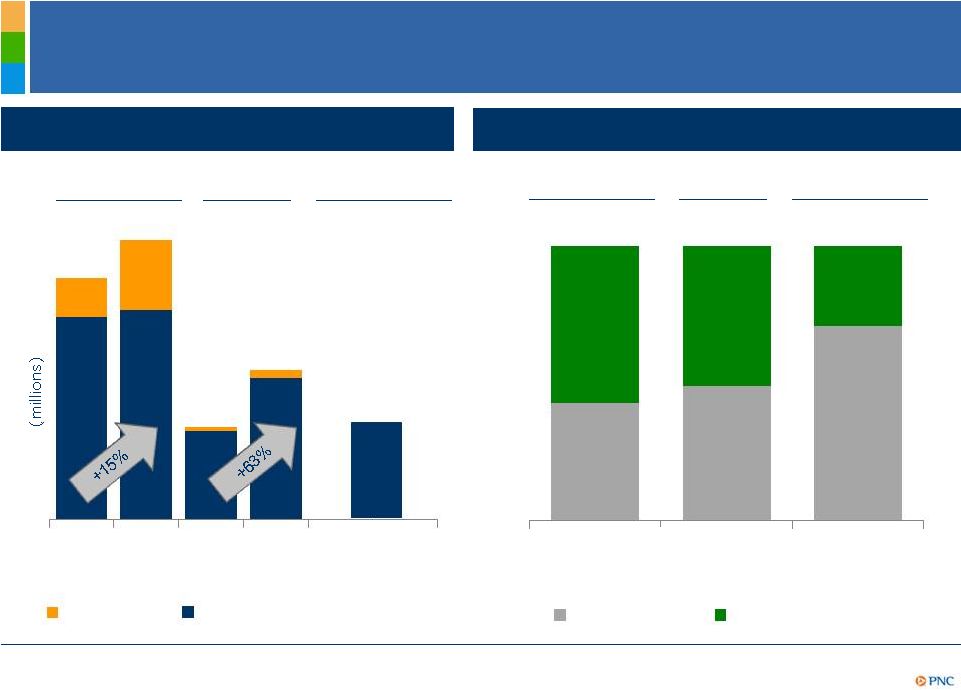

DRAFT

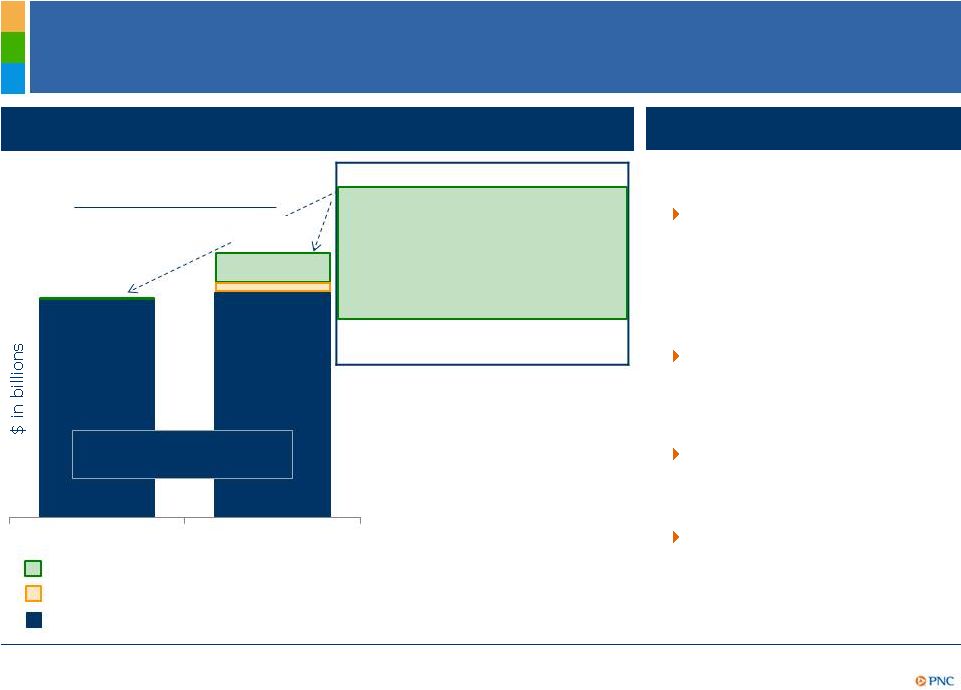

Growing Customers

Long-Term Revenue Potential

Retail Banking

Corporate Banking new

primary clients

Total checking relationships

Asset Management Group

New primary clients

(for the period indicated)

(for the period indicated)

(at period end)

5.4

5.6

6.3

2Q10

2Q11

2Q12

1,012

1,165

492

FY10

FY11

1H12

467

696

866

1H10

1H11

1H12

(1) Total checking relationships refers to consumer and small business accounts including

460,000 relationships acquired from RBC Bank (USA) in March 2012, 9,000 relationships

acquired from the Flagstar branch acquisition in December 2011, and 32,000 relationships

acquired from the BankAtlantic branch acquisition in June 2011. (2) A Corporate Banking

primary client is defined as a corporate banking relationship with annual revenue

generation of $50,000 or more or, within corporate banking, a commercial banking client relationship

with annual revenue generation of $10,000 or more. (3) Asset Management Group primary client

is defined as a client relationship with annual revenue generation of $10,000 or more.

Corporate & Institutional

Banking 1

2

3

5 |

DRAFT

6

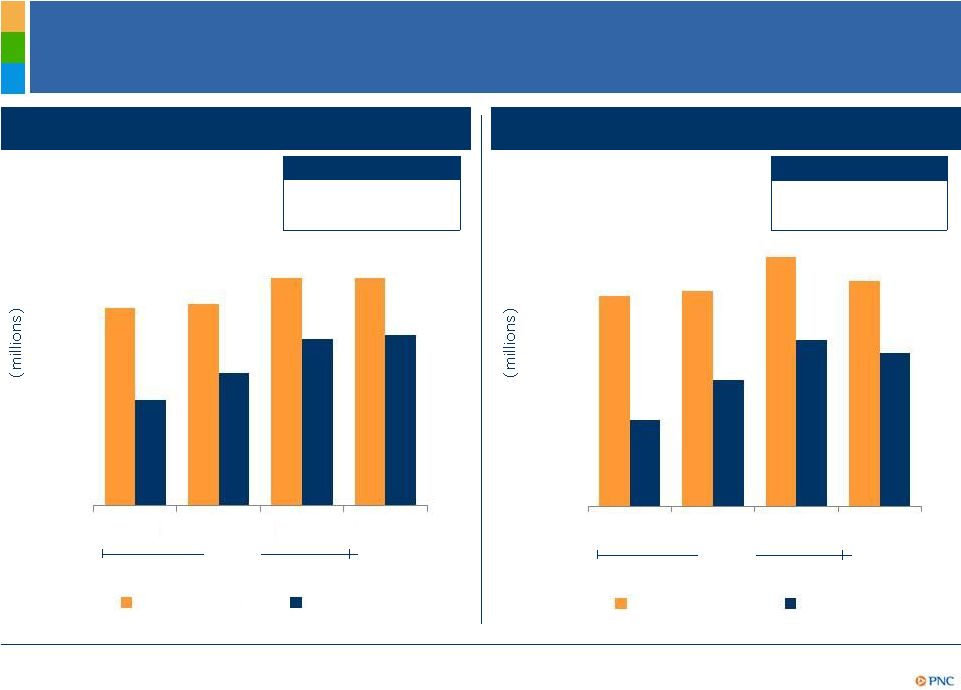

Our Sales Momentum is Strong

Total Corporate Banking and AMG sales

Total Corporate Banking and AMG cross-sell

Actual

Annualized

Actual

Annualized

3-year CAGR

Northeast

5%

Midwest

17%

AMG refers to Asset Management Group. (1) Annualized.

3-year CAGR

Northeast

2%

Midwest

20%

1

1

$0

$100

$200

$300

$400

$500

$600

2009

2010

2011

2012

Northeast

Midwest

$50

$100

$150

$200

$250

$300

2009

2010

2011

2012

Northeast

Midwest

$0 |

DRAFT

7

Philadelphia

3

AMG refers to Asset Management Group. (1) 2010 vs. 2012 annualized total market sales. (2) RBC

markets defined as Eastern Carolina, Western Carolina, Greater Georgia, Northern

Alabama and Gulf Coast. AMG sales not yet significant to RBC markets as we are in the build-out

phase. (3) For the first half 2012. (4) 12-month annualized sales calculated based on

April-July 2012 sales. (5) 12-month annualized. Expanding the Successful PNC

Model in Underpenetrated Markets

Philadelphia

1

Chicago

1

$xx

$105

$121

$40

$65

AMG sales

Corporate Banking sales

RBC markets

2

Chicago

3

Total Corporate Banking and AMG sales

Corporate Banking cross-sell sales by type

YTD12

$42

RBC markets

2

Apr-Jul

2012

2010

2012

5

2010

2012

5

2012

4

43%

49%

71%

57%

51%

29%

Non-Credit Sales

Credit Sales

1

2

3

1

3

2 |

DRAFT

8

Key Retail Revenue Strategies

Overall revenue strategies

Opportunities to reduce cost to serve in

existing traditional branch network

Optimize branches and increase

customer loyalty

Examples

Pittsburgh, Cleveland

markets

Grow select customer segments

Broaden

revenue

opportunities

by

expanding

our

share

of

customers

wallets

Rethink our delivery network by creating a customer experience that improves customer

loyalty and our business margins

Secular trends in targeted segments

provide opportunity to grow using fewer

branches and more technology

Invest in multi-channel experiences

Applies in growth markets; such as:

Traditional branch network

Fewer branches/more technology

Migrate branch transactions to

image-enabled ATMs

Mobile deposit

PNC advantages

brand, non-branch

sales, differentiated offers

Southeast, e.g. Atlanta

Midwest, e.g. Chicago |

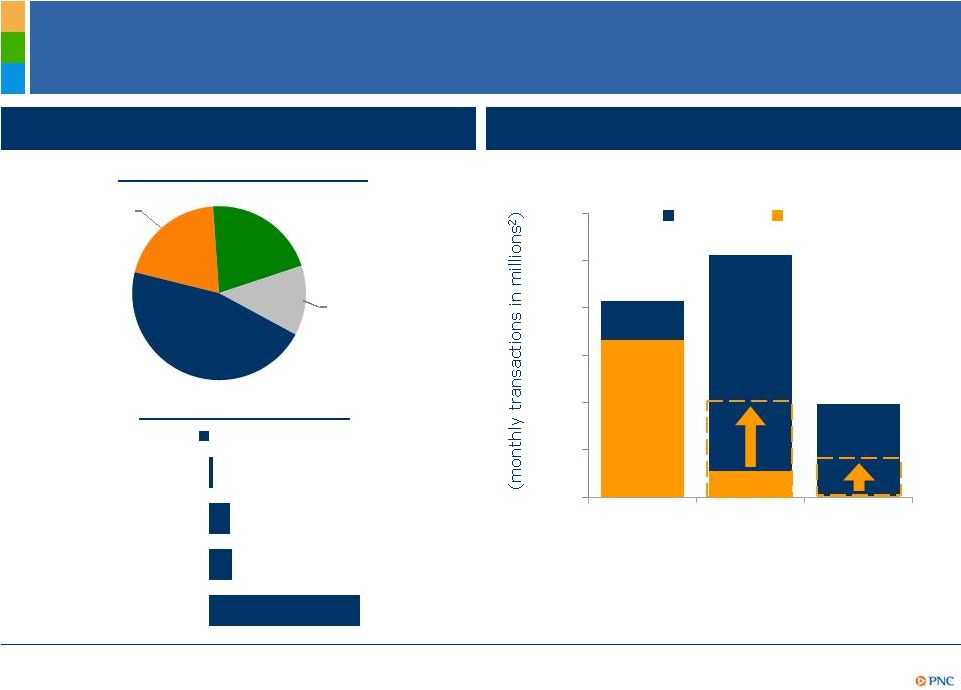

DRAFT

9

Improving Customer Experience, Loyalty and Margins

ATM channel migration strategy

PNCs customers changing preferences

Withdrawals

Deposits

Check

cashing

40%

potential

20%

potential

Transaction

behavior

mix

1

Cost per transaction

High online

13%

0

2

4

6

8

10

12

Teller

ATM

Traditional

Branch

20%

Virtual

21%

Multi-

channel

46%

$3.97

$0.59

$0.56

$0.10

Branch

ATM

Online/ Mobile

Call center -

Interactive

voice response

Consumer

(1) Percentages reflect the proportion of PNC customers considered to be traditional branch,

virtual, high online usage or multi-channel customers based upon channel utilized for

transactions. Transactions refer to service transactions which include deposits, withdrawals and payments. Traditional branch customer is a customer who

conducts greater than 80% of monthly transactions in a branch. Virtual customer is a customer

who conducts the majority of monthly transactions at non-branch channels (i.e., ATM,

Online, Call Center, Mobile). High online usage customer is a customer with 10 or more monthly of the following: online sessions, transfers, online

bill pays and two or fewer branch transactions. Multi-channel customer is a customer who

uses all the channels including branch but is not dominant in any. (2) Monthly

transactions reflect the monthly average for transactions conducted from October 2010-November 2011. |

DRAFT

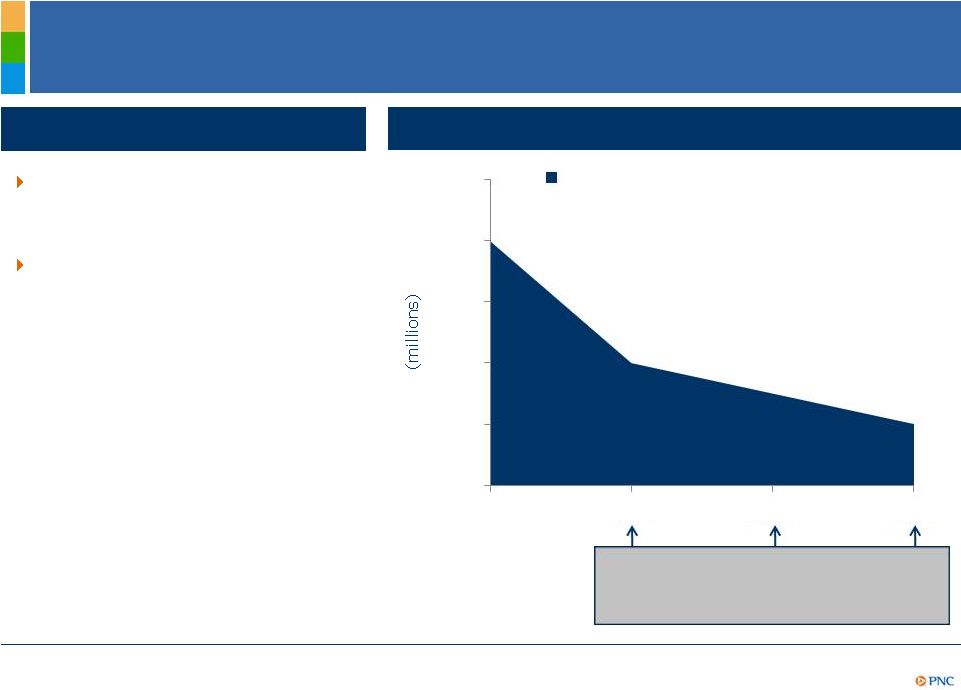

10

Revenue Potential Should Exceed Decline in Purchase

Accounting Accretion

Total revenue in 2013 expected

to increase when compared to

2012

Core NII

2

and noninterest income

growth expected to exceed the

purchase accounting decline of

approximately $400 million

Purchase accounting accretion decline

2013 highlights

(1) Refer to Cautionary Statement in the Appendix, including assumptions. (2) Core NII is

total net interest income less purchase accounting accretion.

$400

$200

$100

$0

$100

$200

$300

$400

$500

2013

2014

2015

2016

Expected year over year decline in

purchase accounting accretion

PAA decline in 2014 is less than 1.5% of total

revenue and declining going

forward

1

1

$150 |

DRAFT

11

Disciplined Expense Management While Investing For

Growth

Highlights

Noninterest expense overview

Continuous improvement:

Select costs

All other noninterest expense

RBC Bank (USA) operating costs

2012 continuous

improvement initiatives

target of $400 million

4

has

resulted in a financial

impact of $186 million in

1H12

Continuous improvement

cost saves expected to

provide capacity for over

90% of 2012 investments

Goal of CIP is to provide

the capacity to invest in

future growth

RBC Bank (USA)

integration cost saves of

$150 million remain on

track

Components of

Noninterest Expense

1

1

1H11

1H12

Legal/mortgage

foreclosure-related/

OREO costs³

2%

6%

Integration costs

0%

4%

TPS redemption

charges

0%

2%

% of noninterest

expense

2%

12%

$4.2

$5.1

All other noninterest

expense relatively flat

1H11

1H12

2

$4.2

$4.3

(1) Further information is provided in the Appendix. (2) Select costs include legal/mortgage

foreclosure/OREO costs, integration costs and trust preferred securities redemption

charges. (3) Legal represents accruals for legal contingencies and mortgage foreclosure represents costs

to comply with regulatory consent decrees. OREO costs consist of gains/losses on sale of OREO

assets, write-downs on the assets and operating expenses. (4) Continuous improvement

initiatives related to legacy PNCs operational and business efficiency initiatives with an

estimated 2012 impact of $400 million, which is part of the total CIP 2012 goal of $550

million.

|

DRAFT

12

Effectively Managing Credit Risk

2Q12 credit risk metrics

PNC

Peers

Strong credit performance

0.71%

1.03%

PNC

Peers

1.92%

3.26%

PNC

Peers

1.39%

2.09%

PNC

Peers

2.30%

2.26%

3.06%

4

Net charge-offs

to average loans

Nonperforming

assets

2

to

total assets

Nonperforming

loans

2

to

total loans

Loan

loss

reserves

3

to

total loans

(1) Reflects company data for 2Q12 as of quarter-end except net charge-offs, which are

for the quarter and annualized, and average loans, which are for the quarter. Peer

source: SNL database. Peers reflects the average of the peers listed in the Appendix. (2) Nonperforming loans exclude certain government

insured or guaranteed loans, loans held for sale, loans accounted for under the fair value

option and purchased impaired loans. (3) The allowance for loan and leases losses

includes impairment reserves attributable to purchased impaired loans. (4) 2Q12 reserves/loans for PNC would have been 3.06% if both

reserves and loans had been adjusted to include the remaining marks on purchased impaired

loans. Further information is provided in the Appendix. Other peers have made

acquisitions and have marks on purchased impaired loans; however, no adjustments have been made for those peers.

1 |

DRAFT

13

Reserves for Residential Mortgage Repurchase Demands

1

Reflect Expected Lifetime Losses

Elevated levels of residential mortgage

repurchase demands and the change in

behaviors of the GSEs are issues impacting

the entire industry

PNC added provision of approximately $438

million to residential mortgage repurchase

reserves in 2Q12 based on expected lifetime

losses of $1.7 billion

1,3

which includes $1.2

billion of losses incurred to date

Relative to the companies listed in the table,

PNCs reserve levels to outstanding demands

and loss coverage ratio are strong

Highlights

Reserves to outstanding demands

USB

132%

WFC

100

JPM

94

PNC

92

FITB

78

BAC

70

STI

67

Five Quarter Average Loss coverage ratio

BAC

14.3x

JPM

9.9

PNC

9.4

C

8.2

USB

6.7

WFC

5.3

STI

3.7

FITB

3.6

2

2

(1) Does not include home equity loans for PNC. (2) Reserves refer to reserves for

indemnification and repurchase liability for asserted and unasserted claims with

respect to residential mortgages sold. Source: company reports. As of June 30, 2012. (3) Barring significant changes in the future behaviors and demand

patterns of investors/guarantors or other unforeseen circumstances, we believe we are

appropriately reserved against future demands with respect to the sold residential

mortgage portfolio at June 30, 2012. Members of our peer group for which these categories of information was publicly available, plus Citigroup,

are presented.

|

DRAFT

14

Strong Capital and Liquidity Position

(1) Regulatory requirements are inclusive of the capital conservation buffer and subject to

further regulatory guidance and clarity on Basel NPRs. (2) Based on Basel III NPRs and

including application of Basel II (as modified by NPRs) and Basel II.5 rules. (3) Parent company liquidity

coverage

defined

as

liquid

assets

divided

by

funding

obligations

within

a

two

year

period.

2Q12 highlights

Basel I Tier 1 common ratio of 9.3% at June

30, 2012

Capital priorities:

Build capital to support client growth and

business investment

Maintain appropriate capital in light of

economic uncertainty

Return excess capital to shareholders

Basel III Tier 1 common ratio goal of 8.0-8.5%

by year-end 2013 without benefit of phase-ins²

Strong

liquidity position

Loans to deposits ratio of 87%

Parent company two year liquidity

coverage³

of 117%

Basel III Tier 1 common ratio

Basel

III

requirements

8.0% -

8.5%

2013 Goal

Basel III

3.5%

4.0%

4.5%

5.1%

5.8%

6.4%

7.0%

2013

2014

2015

2016

2017

2018

2019

1

Improved capital treatment expected on

sub-investment grade securities |

DRAFT

15

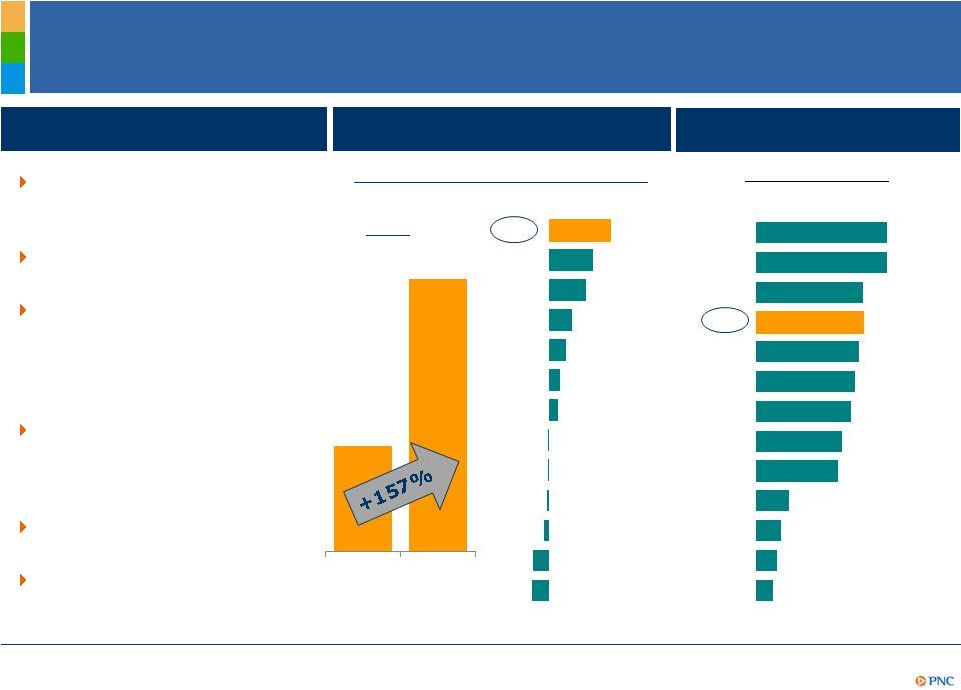

Executing Our Business Model has Delivered Value

CMA

BAC

FITB

STI

RF

KEY

$17.58

$45.19

PNC

Staying core funded and

disciplined in our deposit

pricing

Committed to our

moderate risk philosophy

Leveraging customer

relationships and our

strong brand to grow high

quality, diverse revenue

streams

Focused on creating

positive operating leverage

while investing in

innovation

Remaining disciplined with

our capital

Executing on our strategies

PNCs successful business model

Annualized dividend yield

% change 12/31/2007 to 6/30/2012

As of 8/31/2012

12/31/07

6/30/12

157%

112%

94%

59%

45%

28%

25%

-1%

-2%

-3%

-12%

-39%

-42%

PNC

WFC

USB

JPM

MTB

COF

BBT

3.2%

3.2%

2.6%

2.6%

2.5%

2.4%

2.3%

2.1%

2.0%

0.8%

0.6%

0.5%

0.4%

MTB

JPM

WFC

PNC

BBT

KEY

USB

FITB

CMA

STI

RF

BAC

COF

2

1

Tangible book value per share

Peer Source: SNL DataSource. (1) Tangible book value per share calculated as book value per

share less goodwill and certain other intangible assets. Further information is

provided in the Appendix. (2) Dividend yield calculated as the annualized dividend divided by the

closing stock price.

|

DRAFT

16

Cautionary Statement Regarding Forward-Looking

Information

Appendix

This presentation includes snapshot information about PNC used by way of

illustration and is not intended as a full business or financial review. It

should not be viewed in isolation but rather in the context of all of the information made available by PNC in its SEC filings.

We also make statements in this presentation, and we may from time to time make other

statements, regarding our outlook for earnings, revenues, expenses, capital levels and

ratios, liquidity levels, asset levels, asset quality, financial position, and other matters regarding or

affecting PNC and its future business and operations that are forward-looking statements

within the meaning of the Private Securities Litigation Reform Act.

Forward-looking statements are typically identified by words such as believe, plan, expect, anticipate, see,

look, intend, outlook, project,

forecast, estimate, goal, will, should and other similar words and expressions. Forward-

looking statements are subject to numerous assumptions, risks and uncertainties, which change

over time. Forward-looking statements speak only as of the date made. We do not assume any duty

and do not undertake to update forward-looking statements. Actual results or

future events could differ, possibly materially, from those anticipated in forward-looking statements, as well as

from historical performance.

Our forward-looking statements are subject to the following principal risks and

uncertainties.

Our businesses, financial results and balance sheet values are affected by business and

economic conditions, including the following:

o

Changes in interest rates and valuations in debt, equity and other financial markets.

o

Disruptions in the liquidity and other functioning of U.S. and global financial markets.

o

The impact on financial markets and the economy of any changes in the credit ratings of U.S.

Treasury obligations and other U.S. government-backed debt, as well as issues

surrounding the level of U.S. and European government debt and concerns regarding the

creditworthiness of certain sovereign governments, supranationals and financial institutions

in Europe.

o

Actions by Federal Reserve, U.S. Treasury and other government agencies, including those that

impact money supply and market interest rates.

o

Changes in customers, suppliers and other counterparties performance and

creditworthiness.

o

Slowing or failure of the current moderate economic expansion.

o

Continued effects of aftermath of recessionary conditions and uneven spread of positive

impacts of recovery on the economy and our counterparties, including adverse impacts on

levels of unemployment, loan utilization rates, delinquencies, defaults and counterparty

ability to meet credit and other obligations.

o

Changes in customer preferences and behavior, whether due to changing business and economic

conditions, legislative and regulatory initiatives, or other factors.

Our forward-looking financial statements are subject to the risk that economic and

financial market conditions will be substantially different than we are currently

expecting. These statements are based on our current view that the moderate economic expansion will persist in 2012

and interest rates will remain very low.

|

DRAFT

17

Cautionary Statement Regarding Forward-Looking

Information (continued)

Appendix

Legal and regulatory developments could have an impact on our ability to operate our

businesses, financial condition, results of operations, competitive position,

reputation, or pursuit of attractive acquisition opportunities. Reputational impacts could affect matters such as business

generation and retention, liquidity, funding, and ability to attract and retain

management. These developments could include:

o

Changes resulting from legislative and regulatory reforms, including major reform of the

regulatory oversight structure of the financial services industry and changes to laws

and regulations involving tax, pension, bankruptcy, consumer protection, and other industry aspects,

and changes in accounting policies and principles. We will be impacted by extensive

reforms provided for in the Dodd-Frank Wall Street Reform and Consumer Protection

Act (the Dodd-Frank Act) and otherwise growing out of the recent financial crisis, the precise nature,

extent and timing of which, and their impact on us, remains uncertain.

o

Changes to regulations governing bank capital and liquidity standards, including due to the

Dodd-Frank Act and to Basel-related initiatives.

o

Unfavorable resolution of legal proceedings or other claims and regulatory and other

governmental investigations or other inquiries. In addition to matters relating

to PNCs business and activities, such matters may include proceedings, claims, investigations, or inquiries

relating to pre-acquisition business and activities of acquired companies, such as

National City. These matters may result in monetary judgments or settlements or

other remedies, including fines, penalties, restitution or alterations in our business practices and in additional

expenses and collateral costs, and may cause reputational harm to PNC.

o

Results of the regulatory examination and supervision process, including our failure to

satisfy requirements of agreements with governmental agencies.

o

Impact on business and operating results of any costs associated with obtaining rights in

intellectual property claimed by others and of adequacy of our intellectual property

protection in general.

Business and operating results are affected by our ability to identify and effectively

manage risks inherent in our businesses, including, where appropriate, through

effective use of third-party insurance, derivatives, and capital management techniques, and to meet evolving regulatory

capital standards. In particular, our results currently depend on our ability to manage

elevated levels of impaired assets.

Business and operating results also include impacts relating to our equity interest in

BlackRock, Inc. and rely to a significant extent on information provided to us by

BlackRock. Risks and uncertainties that could affect BlackRock are discussed in more detail by BlackRock in its SEC

filings.

Our acquisition of RBC Bank (USA) presents us with risks and

uncertainties related to the integration of the acquired businesses into PNC,

including:

o

Anticipated benefits of the transaction, including cost savings and strategic gains, may be

significantly harder or take longer to achieve than expected or may not be achieved in

their entirety as a result of unexpected factors or events.

o

Our ability to achieve anticipated results from this transaction is dependent also on the

extent of credit losses in the acquired loan portfolios and the extent of deposit

attrition, in part related to the state of economic and financial markets. Also, litigation and regulatory

and other governmental investigations that may be filed or commenced relating to the

pre-acquisition business and activities of RBC Bank (USA) could impact the timing

or realization of anticipated benefits to PNC.

o

Integration of RBC Bank (USA)s business and operations into PNC may take longer than

anticipated or be substantially more costly than anticipated or have unanticipated

adverse results relating to RBC Bank (USA)s or PNCs existing businesses. PNCs ability to integrate RBC

Bank (USA) successfully may be adversely affected by the fact that this transaction results in

PNC entering several geographic markets where PNC did not previously have any

meaningful retail presence.

|

DRAFT

18

Cautionary Statement Regarding Forward-Looking

Information (continued)

Appendix

In addition to the RBC Bank (USA) transaction, we grow our business in part by acquiring

from time to time other financial services companies, financial services assets and

related deposits and other liabilities. These other acquisitions often present risks and uncertainties

analogous to those presented by the RBC Bank (USA) transaction. Acquisition risks

include those presented by the nature of the business acquired as well as risks and

uncertainties related to the acquisition transactions themselves, regulatory issues, and the integration of the

acquired businesses into PNC after closing.

Competition can have an impact on customer acquisition, growth and retention and on

credit spreads and product pricing, which can affect market share, deposits and

revenues. Industry restructuring in the current environment could also impact our business and financial

performance through changes in counterparty creditworthiness and performance and in the

competitive and regulatory landscape. Our ability to anticipate and respond to

technological changes can also impact our ability to respond to customer needs and meet competitive

demands.

Business and operating results can also be affected by widespread

disasters, dislocations, terrorist activities or international hostilities through

impacts on the economy and financial markets generally or on us or our counterparties specifically.

We provide greater detail regarding these as well as other factors in our 2011 Form 10-K,

as amended by Amendment No. 1 thereto, and first and second quarter 2012 Form

10-Qs, including in the Risk Factors and Risk Management sections and the Legal Proceedings and

Commitments and Guarantees Notes of the Notes to Consolidated Financial Statements in those

reports, and in our subsequent SEC filings. Our forward-looking statements

may also be subject to other risks and uncertainties, including those we may discuss elsewhere in this

presentation or in SEC filings, accessible on the SECs website at www.sec.gov and on our

corporate website at www.pnc.com/secfilings. We have included these web addresses

as inactive textual references only. Information on these websites is not part of this document.

Any annualized, proforma, estimated, third party or consensus numbers in this presentation are

used for illustrative or comparative purposes only and may not reflect actual

results. Any consensus earnings estimates are calculated based on the earnings projections made by

analysts who cover that company. The analysts opinions, estimates or forecasts

(and therefore the consensus earnings estimates) are theirs alone, are not those of PNC

or its management, and may not reflect PNCs or other companys actual or anticipated results.

|

DRAFT

19

Non-GAAP to GAAP Reconcilement

Appendix

In millions except per share data

Dec. 31, 2007

Jun. 30, 2012

% Change

Common shareholders' equity

$14,847

$33,884

Common shares outstanding

341

529

Book value per common share

$43.60

$64.00

47%

Goodwill and other intangible assets other than servicing rights

$8,853

$9,981

Common shareholders' equity less intangible assets

$5,994

$23,903

Common shares outstanding

341

529

Tangible book value per common share

$17.58

$45.19

157%

As of

As of

In millions

June 30, 2012

Allowance for loan and lease losses

$4,156

Remaining mark on purchased impaired loans

$1,400

Allowance for loan and lease losses, adjusted to include remaining mark

$5,556

Loans, as reported

$180,425

Loans, adjusted to include remaining mark on purchased impaired loans

$181,825

Allowance for loan and lease losses to loans

2.30%

Allowance for loan and lease losses plus remaining mark to loans plus remaining mark

3.06%

In millions

Jun. 30, 2012

Jun. 30, 2011

% Change

Total revenue, as reported

7,355

7,233

2%

Provision for residential mortgage repurchase obligation

470

35

Total revenue, as adjusted

$7,825

$7,268

8%

For the six months ended |

DRAFT

20

Non-GAAP to GAAP Reconcilement

Appendix

In millions

Jun. 30, 2012

Jun. 30, 2011

Legal/regulatory/OREO costs

283

74

Integration costs

197

6

TPS redemption-related charges

130

-

RBC Bank (USA) operating costs

189

-

All other

4,304

4,166

Total noninterest expense

$5,103

$4,246

For the six months ended |

DRAFT

21

Peer Group of Banks

Appendix

The PNC Financial Services Group, Inc.

PNC

BB&T Corporation

BBT

Bank of America Corporation

BAC

Capital One Financial, Inc.

COF

Comerica Inc.

CMA

Fifth Third Bancorp

FITB

JPMorgan Chase

JPM

KeyCorp

KEY

M&T Bank

MTB

Regions Financial Corporation

RF

SunTrust Banks, Inc.

STI

U.S. Bancorp

USB

Wells Fargo & Co.

WFC

Ticker |