SLIDE PRESENTATION

Published on March 11, 2010

The PNC

Financial Services Group, Inc. Citigroup Financial Services Conference March 11, 2010 Exhibit 99.1 * * * * * * * * * * * |

2 Cautionary Statement Regarding Forward-Looking Information and Adjusted Information This presentation includes snapshot information about PNC used by way of illustration. It is not intended as a full business or

financial review and should be viewed in the context of all of the information made

available by PNC in its SEC filings. The presentation also contains forward-looking statements regarding our outlook or expectations relating to PNCs future business,

operations, financial condition, financial performance, capital and liquidity levels,

and asset quality. Forward-looking statements are necessarily subject to numerous assumptions, risks and uncertainties, which change over time. The forward-looking statements in this presentation are qualified by the factors affecting

forward-looking statements identified in the more detailed Cautionary Statement included in the Appendix, which is included in the version of the presentation materials posted on our corporate website at www.pnc.com/investorevents. We provide greater detail regarding some of these factors in our most recent Form 10-K, including in the Risk Factors and Risk Management sections of that report, and in our subsequent SEC filings (accessible on the

SECs website at www.sec.gov and on or through our corporate website at

www.pnc.com/secfilings). We have included web addresses here and elsewhere in this presentation as inactive textual references only. Information on these websites is not part of this document. Future events or circumstances may change our outlook or expectations and may also affect the

nature of the assumptions, risks and uncertainties to which our forward-looking

statements are subject. The forward-looking statements in this presentation speak only as of the date of this presentation. We do not assume any duty and do not undertake to update those statements. In this presentation, we will sometimes refer to adjusted results to help illustrate the impact of

certain types of items, such as our fourth quarter 2009 gain related to

BlackRocks acquisition of Barclays Global Investors (the BLK/BGI gain), our fourth quarter 2008 conforming provision for credit losses for National City, and other integration costs in the 2009 and 2008 periods.

This information supplements our results as reported in accordance with GAAP and should not be viewed in isolation from, or a substitute for, our GAAP results. We believe that this additional information and the reconciliations we provide may be useful to investors, analysts, regulators and others as

they evaluate the impact of these respective items on our results for the periods

presented due to the extent to which the items are not indicative of our ongoing operations. In certain discussions, we may also provide information on yields and margins for all

interest-earning assets calculated using net interest income on a

taxable-equivalent basis by increasing the interest income earned on tax-exempt assets to make it fully equivalent to interest income earned on taxable investments. We believe this adjustment may be useful when comparing yields and

margins for all earning assets. This presentation may also include discussion of other

non-GAAP financial measures, which, to the extent not so qualified therein or in the Appendix, is qualified by GAAP reconciliation information available on our corporate website at www.pnc.com under About PNCInvestor Relations.

|

3 Todays Discussion PNC Continues to Build a Great Company. PNC Continues to Build a Great Company. An overview of the PNC business model and franchise Our performance has positioned us well with a strong balance sheet Our earnings capacity is expected to deliver strong results in 2010 We are well-positioned to meet our strategic financial objectives |

4 PNCs Business Model Staying core funded and disciplined in our deposit pricing Returning to a moderate risk profile Leveraging customer relationships and our strong brand to grow high quality, diverse revenue streams Creating positive operating leverage while investing in innovation Remaining disciplined with our capital Executing on our strategies Overview of PNC PNCs Business Model Is Designed to Deliver Strong Results. |

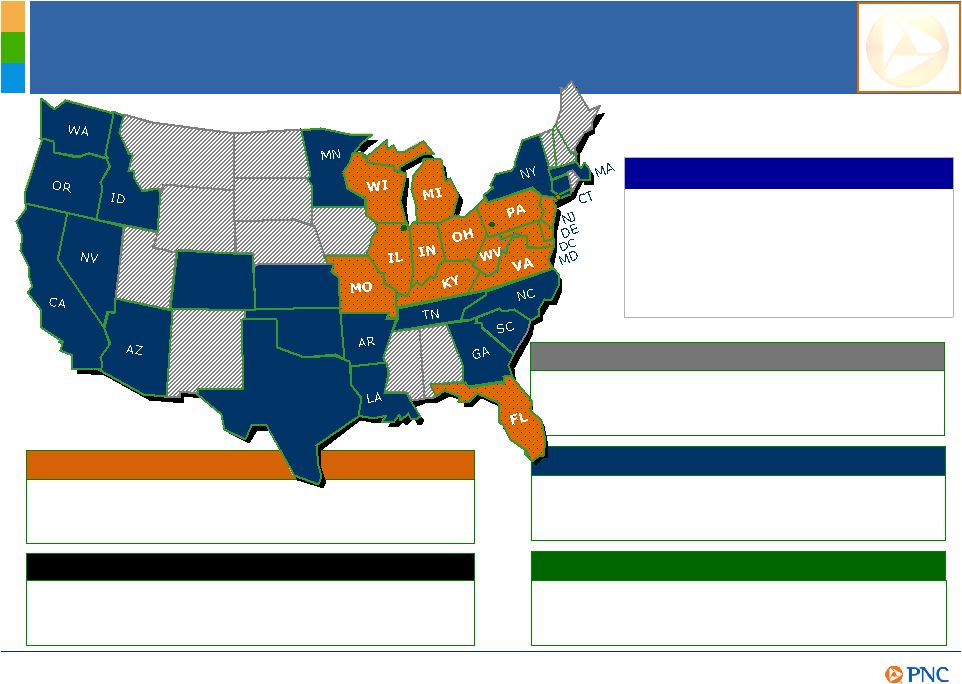

5 Footprint covering nearly 1/3 of the U.S. population Retail Corporate & Institutional A leader in serving middle-market customers and government entities One of the largest bank-held asset managers in the U.S. Asset Management Residential Mortgage One of the nations largest mortgage platforms PNCs Powerful Franchise 8 th $270 billion Assets U.S. Rank¹

Dec. 31, 2009 6,473 2,512 $187 billion 5 th ATMs 5 th Branches 5 th Deposits (1) Rankings source: SNL DataSource; Headquartered in U.S. CO TX KS OK BlackRock A leader in investment management, risk management and advisory services worldwide Overview of PNC |

6 2009 Performance Summary Execution of the PNC business model delivered strong financial results net income of $2.4 billion Well-positioned balance sheet at year end with an improved risk profile, increased loan loss reserves, more liquidity and more capital Strong revenue performance of $16.2¹

billion from diversified sources Disciplined expense management - increased acquisition cost savings goal to $1.5 billion annualized Pretax pre-provision earnings 1,2 exceeded credit costs by $3.2 billion (1) Revenue and noninterest expense reflect presentation of results of operations of PNC Global Investment Servicing (GIS) as income from discontinued operations. (2) Total revenue less noninterest expense. Revenue includes the $1.076 billion BLK/BGI gain. Further information is provided in the Appendix. 2009 Performance Summary |

7 PNCs Higher Quality, Differentiated Balance Sheet Core funded - loans to deposits ratio of 84% Appropriately reserved Improved quality and pricing of deposit base Asset sensitive duration of equity negative 1.2 years Higher quality capital - Proforma Tier 1 common ratio of 8.0% 1 Balance sheet positioning - 8 Preferred equity ($21) $270 Total liabilities and equity ($13) $39 Borrowed funds (11) 12 Other time/savings ($6) $187 Total deposits (7) 14 Other liabilities (10) 49 Retail CDs $15 $126 Transaction deposits 5 22 Common equity (16) 57 Other assets (18) 157 Total loans ($21) $270 Total assets $56 Dec. 31, 2009 $13 YoY change Investment securities Category (billions)

PNC Made Substantial Progress in 2009 Transitioning the PNC Made Substantial Progress in 2009 Transitioning the Balance Sheet to Reflect Our Business Model. Balance Sheet to Reflect Our Business Model. (1) Reported Tier 1 common capital ratio was 6.0% as of December 31, 2009. Proforma ratio reflects Tier 1 common ratio had it included the estimated net impact of TARP preferred stock redemption, February 2010 common equity offering, and pending sale of GIS. Further information is provided in the Appendix. 2009 Performance Summary |

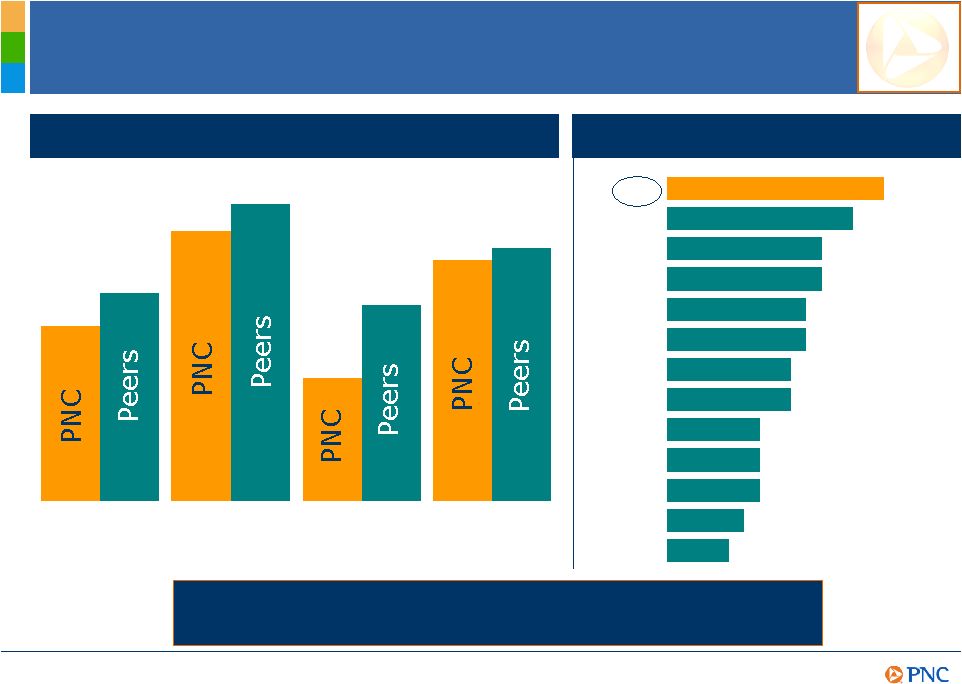

8 4Q09 loans/deposits 4Q09 loans/assets 4Q09 comml real estate loans/assets Relative Balance Sheet Strength Information as of quarter end. Peer source: SNL DataSource and company reports. 68% 78% 84% 90% 90% 91% 91% 92% 93% 95% 106% 107% 109% JPM COF PNC KEY BBT BAC FITB RF STI WFC CMA USB MTB 31% 40% 53% 58% 63% 63% 63% 64% 65% 68% 69% 71% 75% JPM BAC COF PNC BBT WFC KEY RF STI FITB USB CMA MTB 3% 3% 8% 9% 11% 11% 12% 13% 16% 17% 18% 24% 30% JPM BAC COF PNC WFC BBT USB STI KEY FITB CMA RF MTB 2009 Performance Summary |

9 Relative Credit Risk Profile (1) As of or for the year ended December 31, 2009. Peers represents average of banks identified in

the Appendix. Sources: SNL DataSource, company reports. Nonperforming loans to total loans Nonperforming assets to total assets Net charge- offs to average loans Allowance for loan and lease losses to loans 3.60% 3.96% 2.34% 2.77% 1.64% 2.62% 3.22% 3.38% PNCs Commitment to Prudent Risk Management Is Reflected in Our Credit Metrics. 2009 reserves / net charge-offs 1.9 1.7 1.5 1.5 1.4 1.4 1.3 1.3 1.1 1.1 1.1 1.0 0.9 PNC MTB BBT FITB RF JPM WFC USB CMA KEY BAC STI COF X Key 2009 Metrics¹

2009 Performance Summary |

10

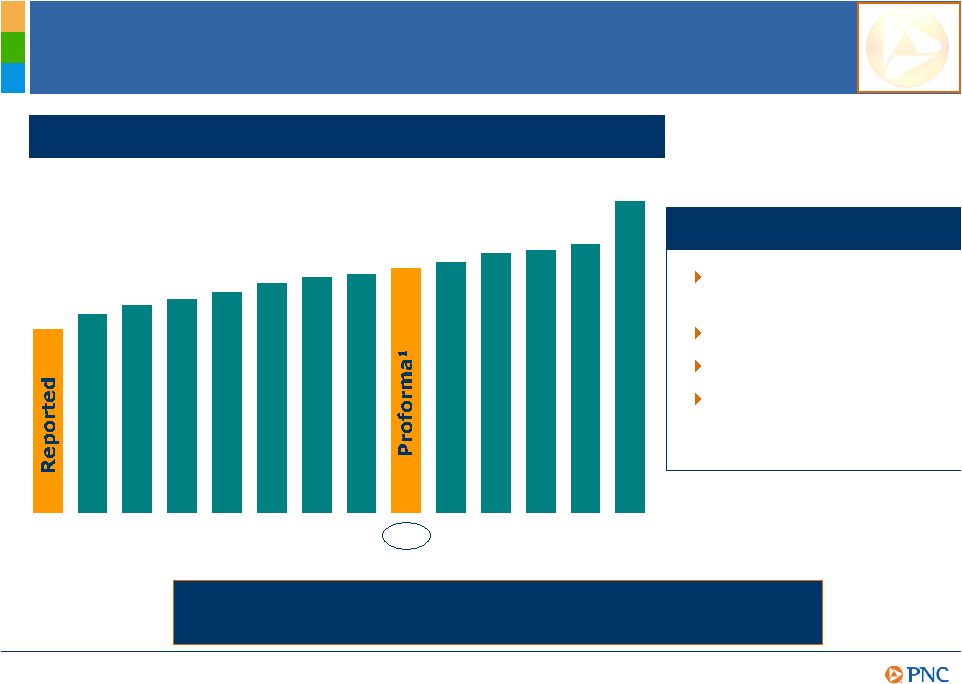

6.5% 6.8% 7.0% 7.2% 7.5% 7.7% 7.8% 8.2% 8.5% 8.6% 8.8% 10.2% 8.0% 6.0% PNC WFC USB FITB RF KEY STI BAC PNC CMA BBT MTB JPM COF Relative Capital Positioning December 31, 2009 Tier 1 common ratio (1) Further information is provided in the Appendix. Peer source: company reports. PNCs capital priorities Maintain strong capital levels Support our clients Invest in our businesses Return capital to shareholders when appropriate PNCs Proforma Tier 1 Common Capital Ratio¹

of 8.0% Provides Flexibility for Future Growth. 2009 Performance Summary |

11

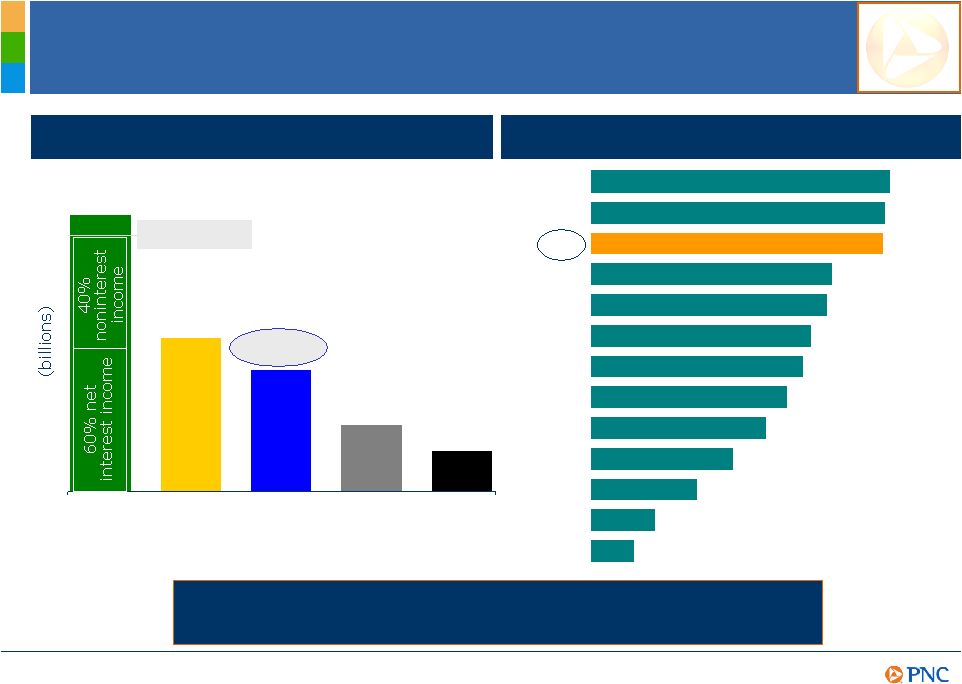

Pretax Pre-Provision Earnings²

Substantially Exceeded Credit Costs $16.2 $9.1 $7.1 $3.9 PNC full year 2009 (1) Revenue and noninterest expense reflect presentation of results of operations of GIS as income from discontinued operations. (2) Total revenue less noninterest expense. Full year 2009 revenue of $16.228 billion includes the $1.076 billion BLK/BGI gain. Full year 2009 noninterest expense was $9.073 billion. Further information is provided in the Appendix. (3) Further information is provided in the Appendix. $2.4 1.86 1.83 1.82 1.50 1.47 1.37 1.32 1.22 1.09 0.89 0.66 0.40 0.27 MTB WFC PNC JPM USB BBT COF FITB BAC CMA RF STI KEY 2009 pretax pre-provision earnings²/provision Excluding the BLK/BGI gain 1.55x³

X Revenue¹

Noninterest expense¹

Pretax pre- provision earnings²

Provision Net income PNC Is Recognized for the Ability to Create Positive Operating PNC Is Recognized for the Ability to Create Positive Operating Leverage to Help Offset Credit Costs. Leverage to Help Offset Credit Costs. 2009 Performance Summary $15.2 excluding the BLK/BGI gain |

12

Strong Earnings Capacity in 2010 (1) 2010 expectations exclude the impact of the 2009 $1.076 billion pretax BLK/BGI gain and the

2010 impact of the pending sale of GIS. (2) Total revenue less noninterest

expense. (3) Annualized acquisition-related cost savings goal. Net interest income

and net interest margin consistent with 3Q09 annualized Lower noninterest income due to 2009 impact of MSR hedging gains Reduced expenses driven by increased acquisition cost saves and lower integration costs Credit cost improvement as the economy recovers Significant pretax pre-provision earnings²

will continue to exceed credit costs 2010 Expectations¹

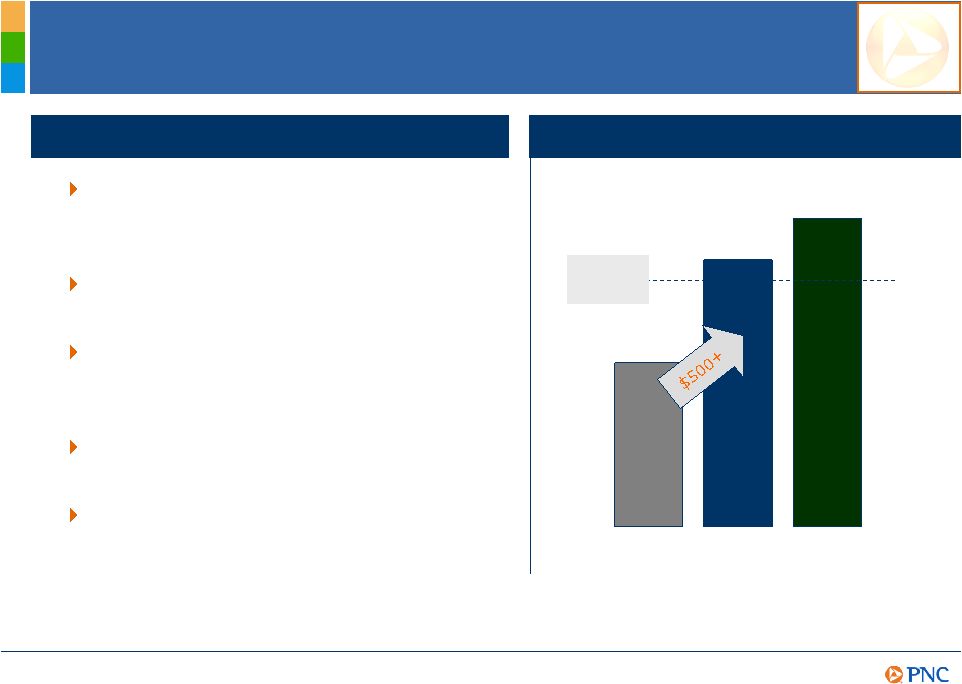

2009 captured $800 $1,300+ 2011 goal³

$1,500 2010 expectation 4Q09 annualized >$1,200 PNC acquisition cost saves (millions) 2010 expectations¹

|

13

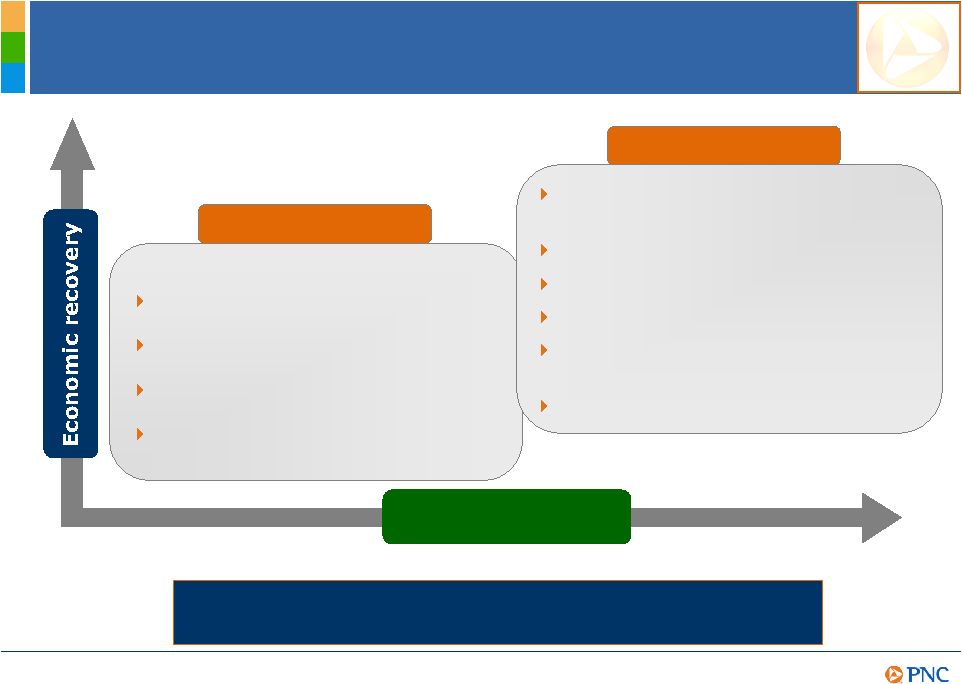

Strategic benefits Immediate benefits PNCs Opportunities for Growth Strategic Financial Objectives Lower deposit costs Leveraging cross sell capabilities Acquisition cost savings Improvement in credit costs Leveraging PNC brand to grow clients across our businesses Product innovation Higher loan utilization rates Commercial real estate refinancings Improved capital markets and asset management fees Higher interest rates PNC Is Positioned to Deliver Even Greater Shareholder Value as PNC Is Positioned to Deliver Even Greater Shareholder Value as the Economy Recovers. the Economy Recovers. Execution |

14

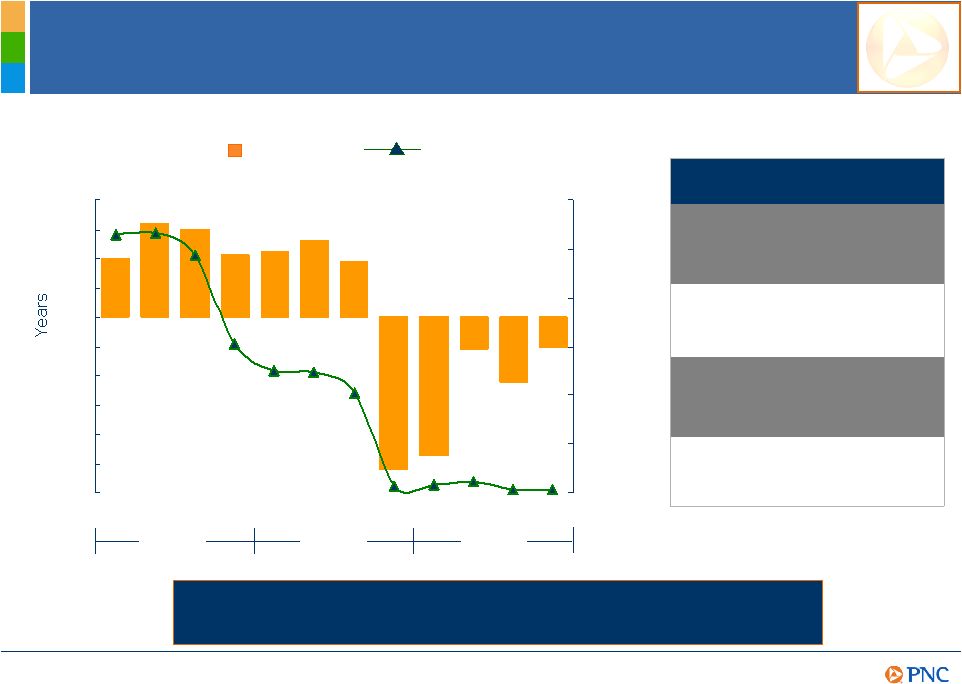

(6) (5) (4) (3) (2) (1) 0 1 2 3 4 0% 1% 2% 3% 4% 5% 6% Balance Sheet Management PNC Duration of Equity (At Quarter End) Fed Funds Effective Rate (At Quarter End) 2007 2008 2009 1.4% 100 bps increase (6.0%) 100 bps decrease Effect on NII in 2 nd year from gradual interest rate change over preceding 12 months Effect on NII in 1 st year from gradual interest rate change over following 12 months PNC 4Q09 NII Sensitivity (2.0%) 1.1% 100 bps decrease 100 bps increase Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 PNCs Balance Sheet Is Well-Positioned to Take Advantage of Economic Recovery. Strategic Financial Objectives |

15

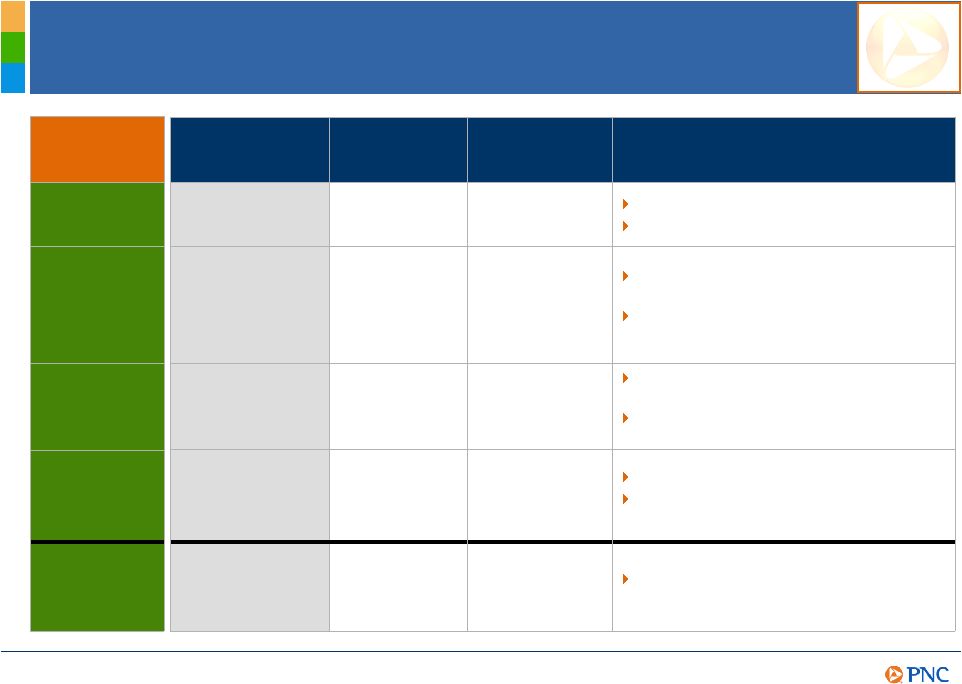

PNCs Framework for Success Execute on and deliver the PNC business model Capitalize on integration opportunities Emphasize continuous improvement culture Leverage credit that meets our risk/return criteria Focus on cross selling PNCs deep product offerings Focus front door on risk-adjusted returns Leverage back door credit liquidation capabilities Maximize credit portfolio value Reposition deposit gathering strategies Action Plans 0.62%²

>$1.2 billion 40% 1,2 2.4% 84% Dec. 31, 2009 1.30%+ $1.5 billion >50% 0.3%-0.5% 80%-90% Strategic Objective Return on average assets (for the year ended) Key Metrics Loans to deposits ratio (as of) Provision to average loans (for the year ended) Noninterest income/total revenue (for the year ended) Acquisition cost savings (4Q09, annualized) Executing our strategies PNC Business Model Staying core funded Returning to a moderate risk profile Growing high quality, diverse revenue streams Creating positive operating leverage (1) Total revenue and noninterest income reflect presentation of results of operations of GIS as income from discontinued operations. (2) Excludes the impact of the $1.076 billion pretax, $687 million after-tax, BLK/BGI gain. Including the gain, noninterest income to total revenue percentage for the year was 44% and the return on average assets for the year was .87%. Further information is provided in the Appendix. Strategic Financial Objectives |

16

Summary The execution of its business model resulted in a strong 2009 performance leaving PNC well-positioned for an economic recovery PNCs earnings capacity is expected to deliver a solid 2010 financial performance PNC is positioned to achieve its strategic financial objectives PNC Continues to Build a Great Company. PNC Continues to Build a Great Company. |

17

Cautionary Statement Regarding Forward-Looking Information Appendix This presentation includes snapshot information about PNC used by way of illustration and is not intended as a full business or financial review. It should not be viewed in isolation but rather in the context of all of the information made available by PNC in its SEC filings. We also make statements in this presentation, and we may from time to time make other statements, regarding our outlook or expectations for earnings, revenues, expenses, capital levels, liquidity levels, asset quality and/or other matters regarding or affecting PNC that are forward-looking statements within the meaning of the Private Securities Litigation Reform Act. Forward-looking statements are typically identified by words such as believe, plan, expect, anticipate, intend, outlook, estimate, forecast, will, project and other similar words and expressions. Forward- looking statements are subject to numerous assumptions, risks and uncertainties, which change over time. Forward-looking statements speak only as of the date they are made. We do not assume any duty and do not undertake to update our forward- looking statements. Actual results or future events could differ, possibly materially, from those that we anticipated in our forward-looking statements, and future results could differ materially from our historical performance. Our forward-looking statements are subject to the following principal risks and uncertainties. We provide greater detail regarding some of these factors in our most recent Form 10-K, including in the Risk Factors and Risk Management sections of that report, and in our subsequent SEC filings. Our forward-looking statements may also be subject to other risks and uncertainties, including those that we may discuss elsewhere in this presentation or in our filings with the SEC, accessible on the SECs website at www.sec.gov and on or through our corporate website at www.pnc.com/secfilings. We have included these web addresses as inactive textual references only. Information on these websites is not part of this document. Our businesses and financial results are affected by business and economic conditions, both generally and specifically in the principal markets in which we operate. In particular, our businesses and financial results may be impacted by:

o Changes in interest rates and valuations in the debt, equity and other financial markets; o Disruptions in the liquidity and other functioning of financial markets, including such disruptions

in the markets for real estate and other assets commonly securing financial

products; o Actions by the Federal Reserve and other government agencies, including those that impact money

supply and market interest rates; o Changes in our customers, suppliers and other counterparties performance in general and their creditworthiness in particular; o Changes in levels of unemployment; and o Changes in customer preferences and behavior, whether as a result of changing business and economic

conditions, climate-related physical changes or legislative and regulatory

initiatives, or other factors. A continuation of recent turbulence in significant portions of the US and global financial markets, particularly if it worsens, could impact our performance, both directly by affecting our revenues and the value of our assets and liabilities and indirectly by affecting our counterparties and the economy generally. Our business and financial performance could be impacted as the financial industry restructures in the current environment, both by changes in the creditworthiness and performance of our counterparties and by changes in the competitive and regulatory landscape. Given current economic and financial market conditions, our forward-looking financial statements are subject to the risk that these conditions will be substantially different than we are currently expecting. These statements are based on our current expectations that interest rates will remain low in the first half of 2010 but will move upward in the second half of the year and our view that the modest economic recovery that began last year will extend through 2010. |

18

Cautionary Statement Regarding Forward-Looking Information (continued)

Appendix Legal and regulatory developments could have an impact on our ability to operate our

businesses or our financial condition or results of operations or our competitive position or reputation. Reputational impacts, in turn, could affect matters such as business generation and retention, our ability to attract and retain management, liquidity, and funding. These legal and regulatory developments

could include: o Changes resulting from legislative and regulatory responses to the current economic and financial

industry environment; o Other legislative and regulatory reforms, including broad-based restructuring of financial

industry regulation as well as changes to laws and regulations involving tax, pension,

bankruptcy, consumer protection, and other aspects of the financial institution industry; o Increased litigation risk from recent regulatory and other governmental developments; o Unfavorable resolution of legal proceedings or other claims and regulatory and other governmental

inquiries; o The results of the regulatory examination and supervision process, including our failure to satisfy

the requirements of agreements with governmental agencies; o Changes in accounting policies and principles; o Changes resulting from legislative and regulatory initiatives relating to climate change that have or may have a negative impact on our customers demand for or use of our products and services in general and their creditworthiness in particular; and o Changes to regulations governing bank capital, including as a result of the so-called Basel 3 initiatives. Our business and operating results are affected by our ability to identify and effectively manage risks inherent in our businesses, including, where appropriate, through the effective use of third-party insurance, derivatives, and capital management techniques, and by our ability to meet evolving regulatory capital standards. The adequacy of our intellectual property protection, and the extent of any costs associated with obtaining rights in intellectual property claimed by others, can impact our business and operating results. Our ability to anticipate and respond to technological changes can have an impact on our

ability to respond to customer needs and to meet competitive demands. Our ability to implement our business initiatives and strategies could affect our financial performance over the next several years. Competition can have an impact on customer acquisition, growth and retention, as well as on

our credit spreads and product pricing, which can affect market share, deposits and

revenues. Our business and operating results can also be affected by widespread

natural disasters, terrorist activities or international hostilities, either as a result of the impact on the economy and capital and other financial markets generally or on us or on our customers, suppliers or other counterparties specifically. Also, risks and uncertainties that could affect the results anticipated in

forward-looking statements or from historical performance relating to our equity

interest in BlackRock, Inc. are discussed in more detail in BlackRocks filings with the SEC, including in the Risk Factors sections of BlackRocks reports. BlackRocks SEC filings are accessible on the SECs website and on or through

BlackRocks website at www.blackrock.com. This material is referenced for

informational purposes only and should not be deemed to constitute a part of this document. In addition, our acquisition of National City Corporation (National City) on December

31, 2008 presents us with a number of risks and uncertainties related both to the acquisition itself and to the integration of the acquired businesses into PNC. These risks and uncertainties include the following: The anticipated benefits of the transaction, including anticipated cost savings and strategic gains, may be significantly harder or take longer to achieve than expected or may not be achieved in their entirety as a result of unexpected factors or

events. |

19

Cautionary Statement Regarding Forward-Looking Information (continued)

Appendix Our ability to achieve anticipated results from this transaction is dependent on the state going forward of the economic and financial markets, which have been under significant stress recently. Specifically, we may incur more credit losses from National Citys loan portfolio than expected. Other issues related to achieving anticipated financial results include the possibility that deposit attrition or attrition in key client, partner and other relationships may be greater than expected. Legal proceedings or other claims made and governmental investigations currently pending against National City, as well as others that may be filed, made or commenced relating to National Citys business and activities before the acquisition, could adversely impact our financial results. Our ability to achieve anticipated results is also dependent on our ability to bring National Citys systems, operating models, and controls into conformity with ours and to do so on our planned time schedule. The integration of National Citys business and operations into PNC, which includes conversion of National Citys different systems and procedures, may take longer than anticipated or be more costly than anticipated or have unanticipated adverse results relating to National Citys or PNCs existing businesses. PNCs ability to integrate National City successfully may be adversely affected by the fact that this transaction has resulted in PNC entering several markets where PNC did not previously have any meaningful retail presence. In addition to the National City transaction, we grow our business from time to time by acquiring other financial services companies. Acquisitions in general present us with risks, in addition to those presented by the nature of the business acquired, similar to some or all of those described above relating to the National City acquisition. Any annualized, proforma, estimated, third party or consensus numbers in this presentation are used for illustrative or comparative purposes only and may not reflect actual results. Any consensus earnings estimates are calculated based on the earnings projections made by analysts who cover that company. The analysts opinions, estimates or forecasts (and therefore the consensus earnings estimates) are theirs alone, are not those of PNC or its management, and may not reflect PNCs or other companys actual or anticipated results. |

20

Impact of Pending Sale of PNC Global Investment Servicing¹

(0.2) (0.0) Adjustments / other²

1.1 Net intangible assets 1.3 Goodwill and other intangible assets Elimination of net intangible assets: Less: (1.5) Book equity / intercompany debt Cash Book (billions) $1.6 (0.2) 0.5 (0.3) 0.8 $2.3 Estimated PNC tangible capital improvement Eligible deferred income taxes on goodwill and other intangible assets After-tax gain / increase in cash Taxes Pretax gain Sales price $1.8 (0.3) 2.1 $2.3 Estimated gain, cash proceeds and capital enhancement Appendix (1) The transaction is currently expected to close in the third quarter of 2010, subject to regulatory approvals and certain other closing conditions. (2) Book column amount reflects transaction expenses of $46 million; cash column amount reflects transaction expenses of $46 million and $138 million of deferred tax reversal. |

21

Risk-Based Capital Ratios 1.6 1.6 Net impact of pending sale of GIS³

10.3% 8.0% Proforma ratios $23.5 $18.2 Proforma 11.4% 6.0% Ratios 3.0 (.3) $13.9 Tier 1 common 3.0 Common equity offering February 2010²

(7.6) TARP preferred stock redemption February 2010¹

$26.5 December 31, 2009 - Capital Tier 1 risk-based $ in billions (1) Tier 1 common column reflects acceleration of accretion of remaining issuance discount. (2) Does not reflect underwriters over- allotment option. (3) Pending sale of PNC Global Investment Servicing (GIS) is anticipated to occur in the third quarter of 2010 subject to regulatory approvals and certain other closing conditions. Appendix |

22

Non-GAAP to GAAP Reconcilement Appendix For the three months ended, in millions

Pretax Income taxes (benefit) 1 Net income Reported net income (loss) ($246) Conforming provision for credit losses - National City $504 ($176) 328 Net income excluding conforming provision for credit losses - National City $82 Year ended, in millions except per share data

Pretax Income taxes (benefit) 1 Net income Diluted EPS from net income Reported net income $2,403 $4.36 Gain on BlackRock/BGI transation ($1,076) $389 (687) (1.51) Net income excluding gain on BlackRock/BGI transaction $1,716 $2.85 Year ended, in millions except percentages

Net income Average assets Return on average assets Reported $2,403 $276,876 0.87% Excluding gain on BlackRock/BGI transaction $1,716 $276,876 0.62% Dec. 31, 2008 PNC believes that information adjusted for the impact of certain items may be useful due to the extent to which the items are not indicative of our ongoing operations. (1) Calculated using a marginal federal income tax rate of 35%. The after-tax gain on the BlackRock/BGI transaction also reflects the impact of state income taxes. Dec. 31, 2009 PNC believes that information adjusted for the impact of certain items may be useful due to the extent to which the items are not indicative of our ongoing operations. Dec. 31, 2009 |

23

Non-GAAP to GAAP Reconcilement Appendix in millions except percentages Reported 1 Gain on BlackRock/BGI transaction Reported excluding BlackRock/BGI gain Net interest income $9,083 $9,083 Noninterest income 7,145 $1,076 6,069 Total revenue $16,228 $1,076 $15,152 Noninterest income/total revenue 44% 40% Net interest income/total revenue 56% 60% Year ended Dec. 31, 2009 in millions except ratios Total revenue $16,228 Noninterest expense 9,073 Pretax pre-provision earnings 7,155 Provision for credit losses 3,930 Excess of pretax pre-provision earnings over credit losses $3,225 Net charge-offs $2,711 Pretax pre-provision earnings / provision 1.82 Total revenue $16,228 Gain on BlackRock/BGI transaction 1,076 Total revenue excluding BlackRock/BGI gain 15,152 Noninterest expense 9,073 Pretax pre-provision earnings excluding BlackRock/BGI gain 6,079 Provision for credit losses 3,930 Excess of pretax pre-provision earnings excluding BlackRock/BGI gain over credit losses

$2,149 Net charge-offs $2,711 Pretax pre-provision earnings excluding BlackRock/BGI gain / provision 1.55 (1) Reported net interest income, noninterest income, total revenue, noninterest expense, and pretax pre-provision earnings reflect presentation of results of operations of GIS as income from discontinued operations. Year ended Dec. 31, 2009 PNC believes that information adjusted for the impact of certain items may be useful due to the extent to which the items are not indicative of our ongoing operations. PNC believes that pretax pre-provision earnings is useful as a tool to help evaluate ability to provide for credit costs through operations. PNC believes that information adjusted for the impact of certain items may be useful due to the extent to which the

items are not indicative of our ongoing operations. |

24

Non-GAAP to GAAP Reconcilement Appendix Adjustments, pretax Income taxes (benefit) 1 Net income Diluted EPS from net income Adjustments, pretax Income taxes (benefit) 1 Net income Diluted EPS from net income $1,107 $2.17 $559 $1.00 ($1,076) $389 (687) (1.49) 155 (54) 101 .22 $89 ($31) 58 .12 $521 $.90 $617 $1.12 Adjustments, pretax Income taxes (benefit) 1 Net income (loss) Diluted EPS from net income (loss) ($246) $(.77) $504 ($176) 328 .94 81 (29) 52 .15 $134 $.32 Adjustments, pretax Income taxes (benefit) 1 Net income Diluted EPS from net income Adjustments, pretax Income taxes (benefit) 1 Net income Diluted EPS from net income $2,403 $4.36 $914 $2.44 $(1,076) $389 (687) (1.51) $504 ($176) 328 .95 421 (147) 274 .60 145 (51) 94 .27 For the three months ended, in millions except per share data

Net income, as reported Adjustments: Gain on BlackRock/BGI transaction Integration costs Net income, as adjusted For the three months ended, in millions except per share data

Net income (loss), as reported Adjustments: Conforming provision for credit losses - National City Other integration costs Net income, as adjusted Year ended, in millions except per share data

Net income, as reported Adjustments: Gain on BlackRock/BGI transaction Conforming provision for credit losses - National City Other integration costs Net income, as adjusted $1,990 $3.45 $1,336 $3.66 Dec. 31, 2009 Sept. 30, 2009 (1) Calculated using a marginal federal income tax rate of 35%. The after-tax gain on the BlackRock/BGI transaction also reflects the impact of state income

taxes. Dec. 31, 2008 Dec. 31, 2009 Dec. 31, 2008 PNC believes that information adjusted for the impact of certain items may be useful due to the extent to which the items are not indicative of our ongoing operations. |

25

Peer Group of Banks Appendix The PNC Financial Services Group, Inc. PNC BB&T Corporation BBT Bank of America Corporation BAC Capital One Financial, Inc. COF Comerica Inc. CMA Fifth Third Bancorp FITB JPMorgan Chase JPM KeyCorp KEY M&T Bank MTB Regions Financial Corporation RF SunTrust Banks, Inc. STI U.S. Bancorp USB Wells Fargo & Co. WFC Ticker |