ELECTRONIC PRESENTATION SLIDES AND RELATED MATERIALS

Published on March 3, 2009

The PNC

Financial Services Group, Inc. Sandler ONeill West Coast Financial Services Conference March 3, 2009 Exhibit 99.1 * * * * * * * * * * |

2 Cautionary Statement Regarding Forward-Looking Information and Adjusted Information This presentation includes snapshot information about PNC used by way of illustration. It is not intended as a full business or financial review and should be viewed in the context of all of the information made available by PNC in its SEC filings. The presentation also contains forward-looking statements regarding our outlook or expectations relating to PNCs future business, operations, financial condition, financial performance, capital and liquidity levels, and asset quality. Forward-looking statements are necessarily subject to numerous assumptions, risks and uncertainties, which change over time. The forward-looking statements in this presentation are qualified by the factors affecting forward-looking statements identified in the more detailed Cautionary Statement included in the Appendix, which is included in the version of the presentation materials posted on our corporate website at www.pnc.com/investorevents. We provide greater detail regarding these factors in our 2008 Form 10-K, including in the Risk Factors and Risk Management sections, and in our other SEC filings (accessible on the SECs website at www.sec.gov and on or through our corporate website at www.pnc.com/secfilings). We have included these web addresses as inactive textual references only. Information on these websites is not part of this document. Future events or circumstances may change our outlook or expectations and may also affect the nature of the assumptions, risks and uncertainties to which our forward-looking statements are subject. The forward-looking statements in this presentation speak only as of the date of this presentation. We do not assume any duty and do not undertake to update those statements. In this presentation, we will sometimes refer to adjusted results to help illustrate the impact of certain types of items. This information supplements our results as reported in accordance with GAAP and should not be viewed in isolation from, or a substitute for, our GAAP results. We provide these adjusted amounts and reconciliations so that investors, analysts, regulators and others will be better able to evaluate the impact of these items on our results for the periods presented. We believe that information as adjusted for the impact of the specified items may be useful due to the extent to which these items are not indicative of our ongoing operations. In certain discussions, we may also provide information on yields and margins for all interest-earning assets calculated using net interest income on a taxable-equivalent basis by increasing the interest income earned on tax-exempt assets to make it fully equivalent to interest income earned on taxable investments. We believe this adjustment may be useful when comparing yields and margins for all earning assets. This presentation may also include a discussion of other non-GAAP financial measures, which, to the extent not so qualified therein or in the Appendix, is qualified by GAAP reconciliation information available on our corporate website at www.pnc.com under About PNCInvestor Relations. |

3 Key Take-Aways The PNC business model has performed well on a relative basis given the difficult environment A significant portion of National Citys credit risk has been recognized through purchase accounting The National City acquisition presents a tremendous opportunity to leverage PNCs business model and demonstrated ability to execute |

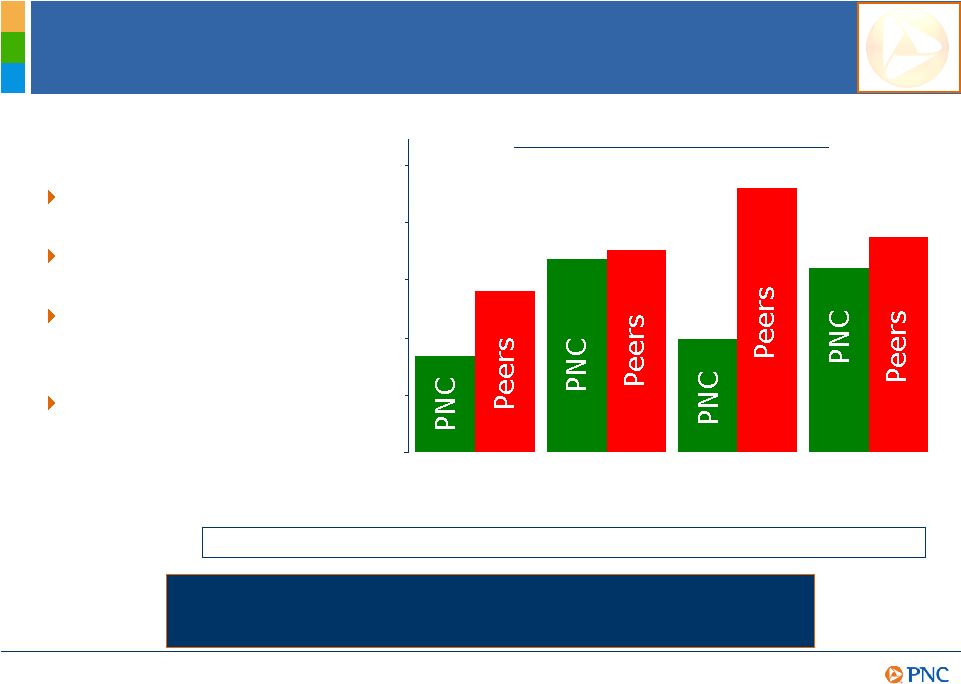

4 A Leader in Executing the Banking Basics (32%) 11% 3 year CAGR (28%) 9% 5 year CAGR (37%) 15% 1 year Pretax pre-provision earnings²

growth 11% 14% Average noninterest-bearing deposits 10% 8% (3%) 7% 13% Peers¹

12% 11% 6% 12% 19% PNC 4Q08 growth versus 2Q07 Average total loans Average total deposits Average noninterest-bearing deposits Average total deposits Average total loans 4Q08 annualized linked quarter growth (1) Peer comparison source: SNL DataSource; Peers represents average of super-regional

banks identified in the Appendix other than PNC. (2) Total revenue less

noninterest expense. Further information is provided in the Appendix. PNC has

remained open for business throughout the credit crunch

and remains committed to meeting the needs of our clients

Note: PNC average balances and pretax pre-provision earnings were not impacted by the

National City acquisition, which closed on December 31, 2008.

while delivering long term value for our shareholders. PNCs Business Model |

5 Balance Sheet Composition PNCs Commitment to Prudent Risk Management Remains a Top Priority for Creating Long Term Value. 100% 9 7 18 66% 100% 15 60 15 2 8% 2008 % of total $291 25 21 52 $193 $291 43 176 44 4 $24 Dec 31 2008 100% 11 7 22 60% 100% 19 49 22 3 7% 2007 % of total Total liabilities and shareholders equity Shareholders equity Other liabilities, interests in consolidated entities Borrowed funds Deposits Total assets Other assets and loan and lease loss allowance Loans, net of unearned income Investment securities Loans held for sale Cash and short-term investments in billions Dec 31, 2008 Key Ratios Loans/Assets PNC Peers¹

60% 69% Loans/Deposits PNC Peers¹

91% 111% (1) Peers represents average of super-regional banks identified in the Appendix other than

PNC. PNCs Business Model |

6 Risk Management Overview PNCs Business Model PNC Is a Recognized Leader in Risk Management. PNC Is a Recognized Leader in Risk Management. PNC monitors multiple risk areas under our Enterprise Wide Risk program - Reputational - Liquidity - Credit - Market - Operational - Strategic PNCs well-established committee structure requires multiple scenario analysis - Economic capital impacts - Summary risk assessment - Alternate planning - Stress testing - Threshold compliance - Inherent risk trends |

7 Relative Credit Risk Profile Peers represents average of super-regional banks identified in the Appendix other than PNC. Net charge-offs percentage is annualized. PNC 4Q08 as reported information includes the impact of National City, which we acquired as of December 31, 2008. The 4Q08 information excluding the impact of National City is reconciled to GAAP in the Appendix. The 4Q08 net charge-off ratio was not impacted by the National City acquisition. 0.00% 0.55% 1.10% 1.65% 2.20% 2.75% Nonperforming loans to total loans Nonperforming assets to total assets Net charge- offs to average loans (three months ended) Allowance for loan and lease losses to loans 1.86% 1.94% .92% 1.55% 1.09% 2.54% 1.77% 2.07% Key 4Q08 Metrics (excluding the impact of National City) Credit migration accelerated in 4Q08 Strengthened loan loss reserve coverage Substantially de-risked the National City loan portfolio at closing Positioned to outperform on a relative basis PNCs Business Model PNCs Credit Risk Profile Is Positioned to Outperform the Peer Group. PNC 4Q08 as reported

..74% .95%

1.09% 2.23% |

8 Capital and Liquidity PNC Is Well-Positioned in Terms of Capital and Liquidity. 21% 88% 5.1% 3.6% 8.2% Sept 30 2008 15% 91% 4.3% 2.9% 9.7% Dec 31 2008 Substantial 12/31/08 liquidity position should enable PNC to meet all 2009 debt maturities

Dec 31 2007 Key Capital Ratios 6.8% Tier 1 risk-based 4.7% Tangible common equity¹

4.8% Tangible common equity excluding accumulated other comprehensive loss 1,2 22% Investment securities to total assets 83% Loans to deposits Key Liquidity Ratios (1) Common shareholders equity less goodwill and other intangible assets net of eligible deferred taxes (excluding mortgage servicing rights) divided by period-end assets less goodwill and other intangible assets net of eligible deferred taxes (excluding mortgage servicing rights). (2) Accumulated other comprehensive loss as of 12/31/08, 9/30/08, and 12/31/07 was $3.9 billion, $2.2 billion, and $147 million, respectively. Adjusted percentages are reconciled to GAAP in the Appendix. PNCs Business Model |

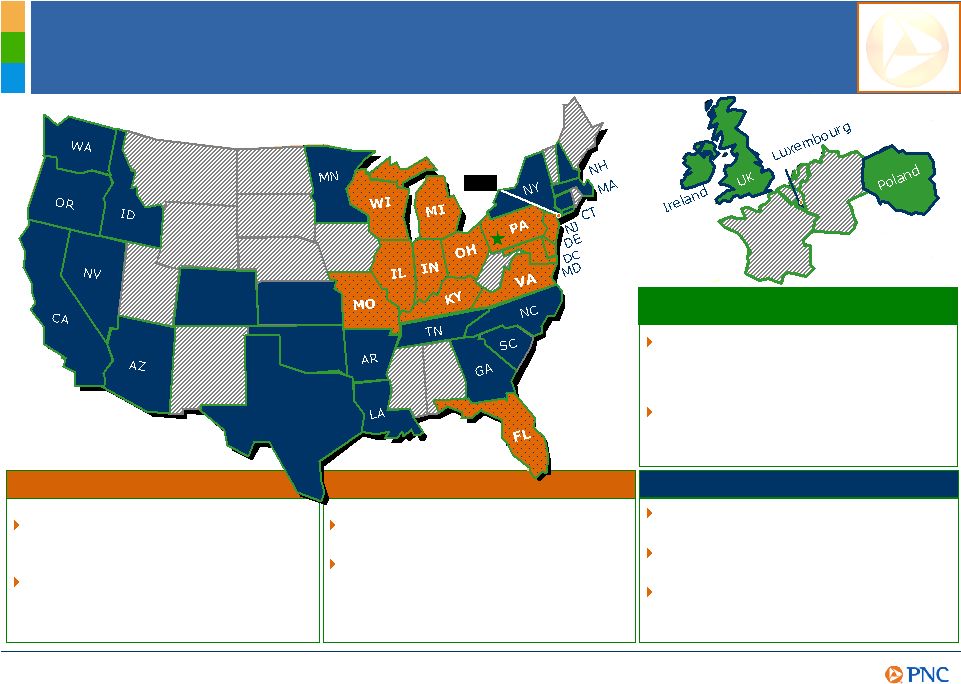

9 Asset Management One of the top 10 largest bank- held asset managers 70% of footprint population in MSAs with median household incomes greater than the national aggregate Footprint population now 95 million, represents almost 1/3rd

of U.S. total A significant presence in 33 of the Top 100 MSAs with offices in 10 state capitals Retail Powerful Opportunities Across the Franchise BlackRock (offices in 22 countries) BLK CO TX KS OK Leveraging PNCs Business Model Global Investment Servicing (international offices) A leading provider of processing, technology and business intelligence services to asset managers, broker- dealers, and financial advisors $2.0 trillion in assets serviced and 72 million shareholder accounts at December 31, 2008 Corporate & Institutional Access to 300 of Fortune 1000 companies and nearly 700 hospitals One of the top 10 Treasury Management businesses in the U.S. One of the nations largest M&A advisory firms for middle market companies |

10

Key Integration Objectives Distressed and core loan portfolios identified, purchase accounting marks established Credit approval and loan/deposit pricing processes aligned Return the balance sheet to a moderate risk profile Extensive client communications and outreach efforts gathered over $1 billion in corporate deposit relationships to date Systems application selection nearly complete and conversion timelines set Schedule for branch conversion complete Process underway, expect significant portion to be achieved through attrition and elimination of open positions Cost save plan being implemented Status Leverage combined strengths to capture clients Convert branch network Achieve $1.2 billion of annualized cost saves Integrate technology platforms Eliminate 5,800 positions across organization Objective The Foundation for a Smooth and Successful Integration Has Been The Foundation for a Smooth and Successful Integration Has Been Established and Communicated. Established and Communicated. Leveraging PNCs Business Model |

11

Key System Integration Milestones Leveraging PNCs Business Model Closing System discovery Application selection Product mapping Programming 1H09 Programming Testing Phase 1 Bank conversion Final stand alone systems conversions Credit reporting Financial reporting Management reporting 2H09 1H10 2H10 Phase 2 Bank conversion Phase 3 Bank conversion Phase 4 Bank conversion Planning and actions will be customer focused and in accordance with our focus on managing toward a moderate risk profile PNCs core suite of systems will be augmented with value added systems of NCC The combination should create a more valuable platform from business continuity to enhanced enterprise-wide reporting tools System integration guiding principles |

12

Significant Retail and Asset Management Revenue Opportunity Combine products and platforms for full impact delivery across our attractive high net worth markets Gain synergies by leveraging the strengths of personal wealth areas and institutional product sets Leverage our established branch referral processes $110B AUM $125B AUA $57B AUM $87B AUA Asset management Expand touch point opportunities to increase our brand awareness and convenience 6,232 4,041 ATMs³

Leverage one of the largest branch distribution networks in the U.S. 2,589 1,148 Branches³

2.9 million Legacy PNC¹

6+ million PNC²

Allows for deeper penetration of our product set, especially fee based and payment business related products Combine focus on on-line innovation and platform integration efficiencies Leverage strengths in small business client area to provide highly profitable sources of funding Consumer and small business customers Opportunity As of December 31, 2008. PNC acquired National City Corporation on December 31, 2008. (1) Does not include and (2) includes the impact of National City. (3) None of anticipated branch divestitures or closings assumed. Leveraging PNCs Business Model |

13

Significant Corporate & Institutional Banking Revenue Opportunity Combine expertise across top industries Retain and deepen long-term relationships Right size portfolios to meet risk/return criteria $45 billion $17 billion Commercial loans (excluding

real estate) Combine strengths across DUS, FHA, Mezzanine, REIT, and low income housing capabilities Scale back residential development exposures $28 billion $9 billion Commercial real estate loans Leverage established deposit gathering strategy and relationship based approach $27 billion $15 billion Deposits Leverage our demonstrated cross selling capabilities Significant opportunity to leverage our range of relationship-based products and services $400 million $336 million Capital markets revenue Leverage combined strengths in the middle market Opportunity to significantly improve risk adjusted returns through fee-based product offerings $975 million $545 million Treasury management revenue Legacy PNC¹

PNC²

Opportunity As of or for the year ended December 31, 2008. PNC acquired National City Corporation on

December 31, 2008. (1) Does not include and (2) includes the impact of National

City. Revenue items include PNC estimates of National City revenue as if the acquisition had been completed at the beginning of 2008. Leveraging PNCs Business Model |

14

A relentless focus on implementing the PNC model Managing toward an overall moderate risk profile Leverage the brand to grow high quality revenue streams A focus on continuous improvement while investing in innovation Disciplined approach to capital management Strong execution capabilities Summary PNC Continues to Build a Great Company. PNC Continues to Build a Great Company. PNCs Business Model |

15

Cautionary Statement Regarding Forward-Looking Information Appendix This presentation includes snapshot information about PNC used by way of illustration and is not intended as a full business or financial review. It should not be viewed in isolation but rather in the context of all of the information made available by PNC in its SEC filings. We also make statements in this presentation, and we may from time to time make other statements, regarding our outlook or expectations for earnings, revenues, expenses, capital levels, liquidity levels, asset quality and/or other matters regarding or affecting PNC that are forward-looking statements within the meaning of the Private Securities Litigation Reform Act. Forward-looking statements are typically identified by words such as believe, expect, anticipate, intend, outlook, estimate, forecast, will, project and other similar words and expressions. Forward-looking statements are subject to numerous assumptions, risks and uncertainties, which change over time. Forward-looking statements speak only as of the date they are made. We do not assume any duty and do not undertake to update our forward- looking statements. Actual results or future events could differ, possibly materially, from those that we anticipated in our forward-looking statements, and future results could differ materially from our historical performance. Our forward-looking statements are subject to the following principal risks and uncertainties. We provide greater detail regarding some of these factors in our 2008 Form 10-K, including in the Risk Factors and Risk Management sections of that report, and in our other SEC filings. Our forward- looking statements may also be subject to other risks and uncertainties, including those that we may discuss elsewhere in this presentation or in our filings with the SEC, accessible on the SECs website at www.sec.gov and on or through our corporate website at www.pnc.com/secfilings. We have included these web addresses as inactive textual references only. Information on these websites is not part of this document. Our businesses and financial results are affected by business and economic conditions, both

generally and specifically in the principal markets in which we operate. In particular,

our businesses and financial results may be impacted by: o Changes in interest rates and valuations in the debt, equity and other financial markets. o Disruptions in the liquidity and other functioning of financial markets, including such disruptions

in the markets for real estate and other assets commonly securing financial

products. o Actions by the Federal Reserve and other government agencies, including those that impact money

supply and market interest rates. o Changes in our customers, suppliers and other counterparties performance in general and their creditworthiness in particular. o Changes in customer preferences and behavior, whether as a result of changing business and economic conditions or other factors. A continuation of recent turbulence in significant portions of the US and global financial markets, particularly if it worsens, could impact our performance, both directly by affecting our revenues and the value of our assets and liabilities and indirectly by affecting our counterparties and the economy generally. Our business and financial performance could be impacted as the financial industry restructures in the current environment, both by changes in the creditworthiness and performance of our counterparties and by changes in the competitive

landscape. Given current economic and financial market conditions, our forward-looking financial

statements are subject to the risk that these conditions will be substantially

different than we are currently expecting. These statements are based on our current expectations that interest rates will remain low through 2009 with continued wide market credit spreads, and our view that national economic trends currently point to a continuation of severe recessionary conditions in 2009 followed by a subdued recovery. |

16

Cautionary Statement Regarding Forward-Looking Information (continued)

Appendix Legal and regulatory developments could have an impact on our ability to operate our businesses or our financial condition or results of operations or our competitive position or reputation. Reputational impacts, in turn, could affect matters such as business generation and retention, our ability to attract and retain management, liquidity, and funding. These legal and regulatory developments could include: o Changes resulting from the Emergency Economic Stabilization Act of 2008, the American Recovery and Reinvestment Act of 2009, and other developments in response to the current economic and financial industry environment, including current and future conditions or restrictions imposed as a result of our participation in the TARP Capital Purchase Program. o Legislative and regulatory reforms generally, including changes to laws and regulations involving tax, pension, bankruptcy, consumer protection, and other aspects of the financial institution industry. o Increased litigation risk from recent regulatory and other governmental developments. o Unfavorable resolution of legal proceedings or regulatory and other governmental inquiries. o The results of the regulatory examination and supervision process, including our failure to satisfy the requirements of agreements with governmental agencies. o Changes in accounting policies and principles. Our issuance of securities to the US Department of the Treasury may limit our ability to return capital to our shareholders and is dilutive to our common shares. If we are unable previously to redeem the shares, the dividend rate increases substantially after five years. Our business and operating results are affected by our ability to identify and effectively manage risks inherent in our businesses, including, where appropriate, through the effective use of third-party insurance, derivatives, and capital management techniques. The adequacy of our intellectual property protection, and the extent of any costs associated with obtaining rights in intellectual property claimed by others, can impact our business and operating results. Our ability to anticipate and respond to technological changes can have an impact on our ability to respond to customer needs and to meet competitive demands. Our ability to implement our business initiatives and strategies could affect our financial performance over the next several years. Competition can have an impact on customer acquisition, growth and retention, as well as on our credit spreads and product pricing, which can affect market share, deposits and revenues. Our business and operating results can also be affected by widespread natural disasters, terrorist activities or international hostilities, either as a result of the impact on the economy and capital and other financial markets generally or on us or on our customers, suppliers or other counterparties specifically. Also, risks and uncertainties that could affect the results anticipated in forward-looking statements or from historical performance relating to our equity interest in BlackRock, Inc. are discussed in more detail in BlackRocks filings with the SEC, including in the Risk Factors sections of BlackRocks reports. BlackRocks SEC filings are accessible on the SECs website and on or through BlackRocks website at www.blackrock.com. This material is referenced for informational purposes only and should not be deemed to constitute a part of this document. In addition, our recent acquisition of National City Corporation (National City) presents us with a number of risks and uncertainties related both to the acquisition transaction itself and to the integration of the acquired businesses into PNC. These risks and uncertainties include the following: The transaction may be substantially more expensive to complete (including the required divestitures and the integration of National Citys businesses) and the anticipated benefits, including anticipated cost savings and strategic gains, may be significantly harder or take longer to achieve than expected or may not be achieved in their entirety as a result of unexpected factors or events. |

17

Cautionary Statement Regarding Forward-Looking Information (continued)

Appendix Our ability to achieve anticipated results from this transaction is dependent on the state going forward of the economic and financial markets, which have been under significant stress recently. Specifically, we may incur more credit losses from National Citys loan portfolio than expected. Other issues related to achieving anticipated financial results include the possibility that deposit attrition or attrition in key client, partner and other relationships may be greater than expected. Litigation and governmental investigations currently pending against National City, as well as others that may be filed or commenced relating to National Citys business and activities before the acquisition, could adversely impact our financial results. Our ability to achieve anticipated results is also dependent on our ability to bring National Citys systems, operating models, and controls into conformity with ours and to do so on our planned time schedule. The integration of National Citys business and operations into PNC, which will include conversion of National Citys different systems and procedures, may take longer than anticipated or be more costly than anticipated or have unanticipated adverse results relating to National Citys or PNCs existing businesses. PNCs ability to integrate National City successfully may be adversely affected by the fact that this transaction will result in PNC entering several markets where PNC did not previously have any meaningful retail presence. In addition to the National City transaction, we grow our business from time to time by acquiring other financial services companies. Acquisitions in general present us with risks, in addition to those presented by the nature of the business acquired, similar to some or all of those described above relating to the National City acquisition. Any annualized, proforma, estimated, third party or consensus numbers in this presentation are used for illustrative or comparative purposes only and may not reflect actual results. Any consensus earnings estimates are calculated based on the earnings projections made by analysts who cover that company. The analysts opinions, estimates or forecasts (and therefore the consensus earnings estimates) are theirs alone, are not those of PNC or its management, and may not reflect PNCs, National Citys, or other companys actual or anticipated results. |

18

Non-GAAP to GAAP Reconcilement Appendix In millions, except percentages Tier 1 risk-based capital ratio December 31 2008 Tier 1 risk-based capital $24,287 Less: TARP issuance (7,579) Tier 1 risk-based capital less TARP issuance $16,708 Risk weighted assets (assumes no decrease in assets without TARP issuance) $251,106 Tier 1 risk-based capital ratio as reported 9.7% Less: TARP issuance (3.0)% Tier 1 risk-based capital ratio as adjusted 6.7% Tangible common equity ratio (a) December 31 September 30 December 31 2008 2008 2007 Common shareholders' equity $17,490 $13,711 $14,847 Less intangible assets, net of deferred taxes (9,206) (8,812) (8,734) Tangible common equity 8,284 4,899 6,113 Add back: accumulated other comprehensive loss (AOCL) 3,949 2,230 147 Tangible common equity, before AOCL $12,233 $7,129 $6,260 Tangible assets $281,874 $136,798 $130,185 Add back: AOCL assets 3,252 3,332 (11) Total assets, excluding AOCL $285,126 $140,130 $130,174 Tangible common equity ratio, as reported 2.9% 3.6% 4.7% Add back: AOCL assets 1.4% 1.5% 0.1% Tangible common equity ratio, as adjusted 4.3% 5.1% 4.8% (a) Common shareholders equity less goodwill and other intangible assets net of eligible deferred taxes (excluding mortgage servicing rights) divided by period-end assets less goodwill and other intangible assets net of eligible deferred taxes (excluding mortgage servicing rights). |

19

Non-GAAP to GAAP Reconcilement Appendix For the year ended December 31, in millions 2003 2004 2005 2006 (c) 2007 2008 '04-'07 CAGR '07-'08 Change '05-'08 CAGR '03-'08 CAGR Total revenue $5,253 $5,541 $6,327 $8,572 $6,705 $7,190 7% 7% Noninterest expense 3,476 3,712 4,306 4,443 4,296 4,430 5% 3% Pretax pre-provision earnings $1,777 $1,829 $2,021 $4,129 $2,409 $2,760 15% 11% 9% Operating leverage 2% 4% (c) Includes the impact on both revenue and expense of the BlackRock/MLIM transaction. In millions, except per share data THREE MONTHS ENDED Adjustments, Net Diluted Adjustments, Net Diluted Pretax Income EPS Pretax Income EPS Net income (loss), as reported $(248) $(.77) $248 $.71 Adjustments: Conforming provision for credit losses - National City $504 328 .94 Other integration costs 81 52 .15 $14 9 .02 Net income, as adjusted $132 $.32 $257 $.73 Adjustments, Net Diluted Pretax Income EPS Net income, as reported $178 $.52 Adjustments: Integration costs $79 (a) 50 .15 Net income, as adjusted $228 $.67 YEAR ENDED Adjustments, Net Diluted Adjustments, Net Diluted Pretax Income EPS Pretax Income EPS Net income, as reported $882 $2.46 $1,467 $4.35 Adjustments: Conforming provision for credit losses - National City $504 328 .95 Other integration costs 145 (b) 94 .27 $151 (a) 99 .30 Net income, as adjusted $1,304 $3.68 $1,566 $4.65 (a) Includes the $45 million conforming provision for credit losses related to the Yardville

acquisition. (b) Includes the $23 million conforming provision for credit losses related to the Sterling

acquisition. December 31, 2008 September 30, 2008 December 31, 2007 December 31, 2008 December 31, 2007 |

20

Non-GAAP to GAAP Reconcilement Appendix As of December 31, 2008 ($ in millions) PNC, excluding National City (a) National City Purchase accounting, eliminations, and reclassifications (b) PNC, as reported Total assets $157,373 $153,069 ($19,361) $291,081 Nonperforming assets 1,443 722 2,165 Nonperforming assets to total assets 0.92% 0.74% Total loans, net of unearned income $75,830 $108,077 ($8,418) $175,489 Nonperforming loans 1,412 250 1,662 Nonperforming loans to total loans 1.86% 0.95% Total loans, net of unearned income $75,830 $108,077 ($8,418) $175,489 Allowance for loan and lease losses 1,343 4,856 (2,282) 3,917 Allowance for loan and lease losses to loans 1.77% 2.23% (a) Includes $7.6 billion related to the issuance to the US Treasury under the US Treasury's

Troubled Asset Relief Program ("TARP") on December 31, 2008 of (1) Fixed Rate

Cumulative Perpetual Preferred Stock, Series N, and (2) a warrant for the US Treasury to purchase PNC common stock. (b) Includes conforming provision for credit losses, elimination of intercompany funding and

capital transactions, redesignation of loans held for sale to loans held for

investment, and other reclassifications. |

21

The PNC Financial Services Group, Inc. PNC BB&T Corporation BBT Comerica CMA Fifth Third Bancorp FITB KeyCorp KEY Regions Financial RF SunTrust Banks, Inc. STI U.S. Bancorp USB Wells Fargo & Company WFC Ticker Peer Group of Super-Regional Banks Appendix List represents 2008 peer group after acquisitions. |