SLIDE PRESENTATION OF CITIGROUP FINANCIAL SERVICES CONFERENCE

Published on February 1, 2006

The PNC Financial Services Group, Inc. Citigroup Financial Services Conference New York, NY February 1, 2006 The PNC Financial Services Group, Inc. Citigroup Financial Services Conference New York, NY February 1, 2006 EXHIBIT 99.1 |

Cautionary Statement Regarding Forward-Looking Information Cautionary Statement Regarding Forward-Looking Information This presentation contains forward-looking statements regarding our outlook or

expectations relating to PNCs future business, operations, financial condition, financial performance and asset quality. Forward-looking statements are necessarily subject to numerous assumptions, risks and uncertainties. The forward-looking statements in this presentation are qualified by the factors affecting forward-looking statements identified in the more detailed Cautionary Statement included in the Appendix, as well as those factors previously disclosed in our 2004 annual

report on Form 10-K, our third quarter 2005 report on Form 10-Q, and other SEC reports (accessible on the SECs website at www.sec.gov and on or through our corporate website at www.pnc.com). Future events or circumstances may change our outlook or expectations and may also

affect the nature of the assumptions, risks and uncertainties to which our forward-looking statements are subject. The forward-looking statements in this presentation speak only as of the date of this presentation. We do not assume any duty and do not

undertake to update those statements. This presentation may also include a discussion of non-GAAP financial measures, which, to the extent not so qualified therein or in the Appendix, is qualified by GAAP

Investors. reconciliation information available on our corporate website at www.pnc.com under For |

Key Messages Key Messages Accomplished a great deal in 2005 Maintained a moderate risk profile that is key to improving consistency Executing strategies to improve operating leverage |

Record year Earned $1.3 billion Strong client activity business segment earnings* grew 18% Strong revenue growth Average loans and deposits continued to grow Improved operating leverage in 4 th quarter - One PNC initiative ahead of schedule Managed capital effectively and invested in PNC Overall asset quality remained very strong Total business segment earnings are reconciled to total GAAP consolidated earnings in the Appendix 2005 Highlights 2005 Highlights Financial Highlights Net income $1.3 billion EPS (diluted) $4.55 ROCE 16.6% Noninterest income to total revenue 66% Loans to deposits* 81% Year Ended December 31, 2005 Loans to deposits as of December 31, 2005 * * |

Investing in Our Future Growth Investing in Our Future Growth Strengthened management team Investments to grow organically - Expanding and refurbishing branch system - Enhancing technology capabilities - Broadening product set Value-added acquisitions - Riggs expanding into growth market - State Street Research fueling continued fee growth - Harris Williams providing additional product and distribution capabilities |

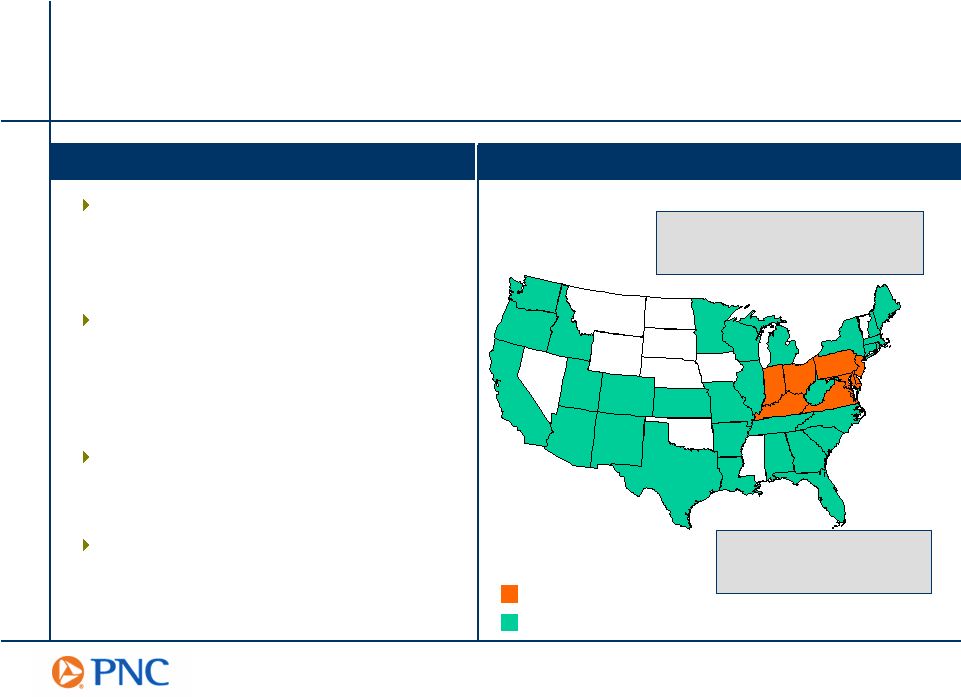

International fund processing: PFPC with offices in U.S., Ireland & Luxembourg International investment management: BlackRock with offices in U.S., Scotland, Hong Kong, Tokyo & Australia Regional, National and International Businesses PNC A Diversified Financial Services Company PNC A Diversified Financial Services Company IN OH PA KY NJ DE Business Leadership Retail Banking - A leading community bank in PNC major markets - Top 10 SBA lender in the U.S. - One of the nations largest wealth management firms Corporate & Institutional Banking - Top 10 Treasury Management business - The nations second largest lead arranger of asset-based loan syndications - Harris Williams - one of the nations largest M&A advisory firms for middle market companies PFPC - Among the largest providers of mutual fund transfer agency and accounting and administration services in the U.S. BlackRock - One of the nations largest publicly traded asset managers PNC Bank Branches PNC Employees / Offices Outside of Retail Footprint VA DC MD |

Accomplished a great deal in 2005 Maintained a moderate risk profile that is key to improving consistency Credit risk Interest rate risk Executing strategies to improve operating leverage Key Messages Key Messages |

Diverse - No large industry concentration Granular - Only 2% of commercial lending exposure is non-investment grade and >$50 million Targeted - Focused on clients that meet risk- adjusted returns Home equity portfolio statistics - % of first lien positions 46% - Weighted average loan to value 68% - Weighted average FICO scores 728 Disciplined Approach Leads to Strong Credit Risk Profile Disciplined Approach Leads to Strong Credit Risk Profile Strong Asset Quality Lending Profile (As of December 31, 2005)

PNC December 31, 2005 Nonperforming loans to loans 0.39% 0.32% Net charge-offs to average loans (full year 2005) 0.06% 0.38% Excluding $53 million loan recovery in 2Q05 0.18% Allowance for loan and lease losses to loans 1.21% 1.15% Peer Group Source: SNL DataSource; PNC as reported Peer group represents average of super-regional banks identified in the Appendix. Peer group excludes PNC. . Commercial Consumer |

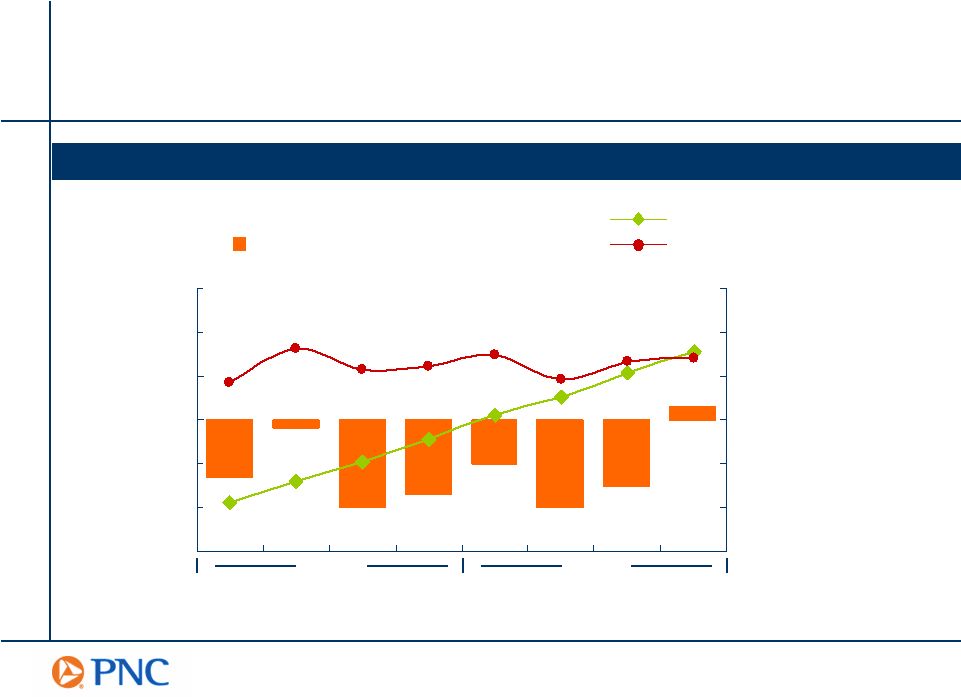

Our Approach to Interest Rate Risk: Preserve and Optimize Long-Term Value Our Approach to Interest Rate Risk: Preserve and Optimize Long-Term Value Neutral Duration of Equity Positions Us Well in This Environment (3) (2) (1) 0 1 2 3 0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% Duration of Equity Years 3 Month LIBOR 10 Year T Note At Quarter End 2004 2005 |

Accomplished a great deal in 2005 Maintained a moderate risk profile that is key to improving consistency Executing strategies to improve operating leverage Invest in and grow fee-based businesses Grow net interest income Make expense control part of our culture Key Messages Key Messages |

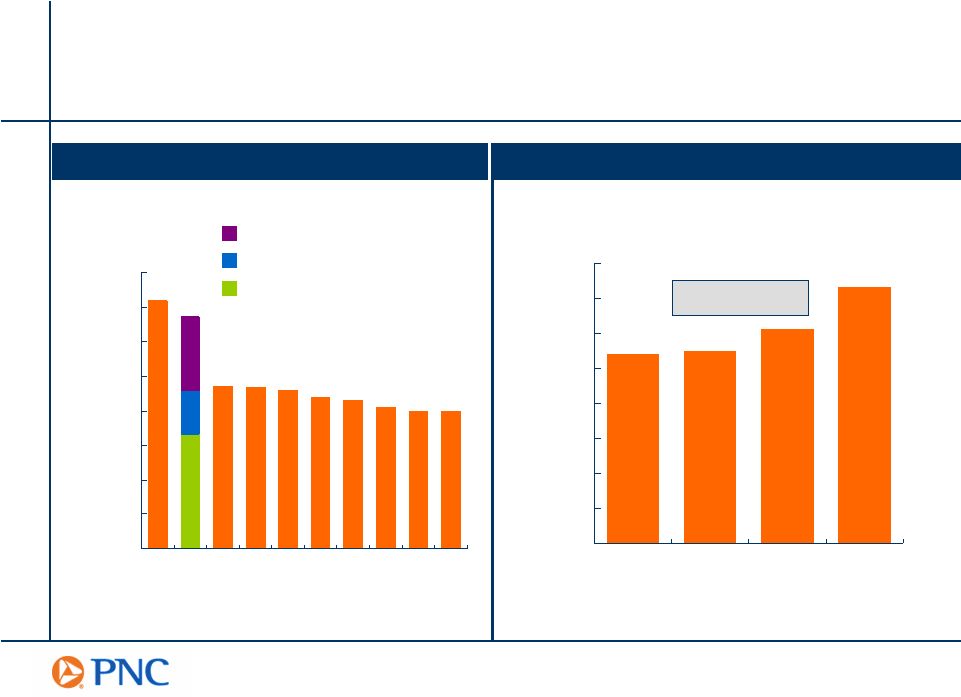

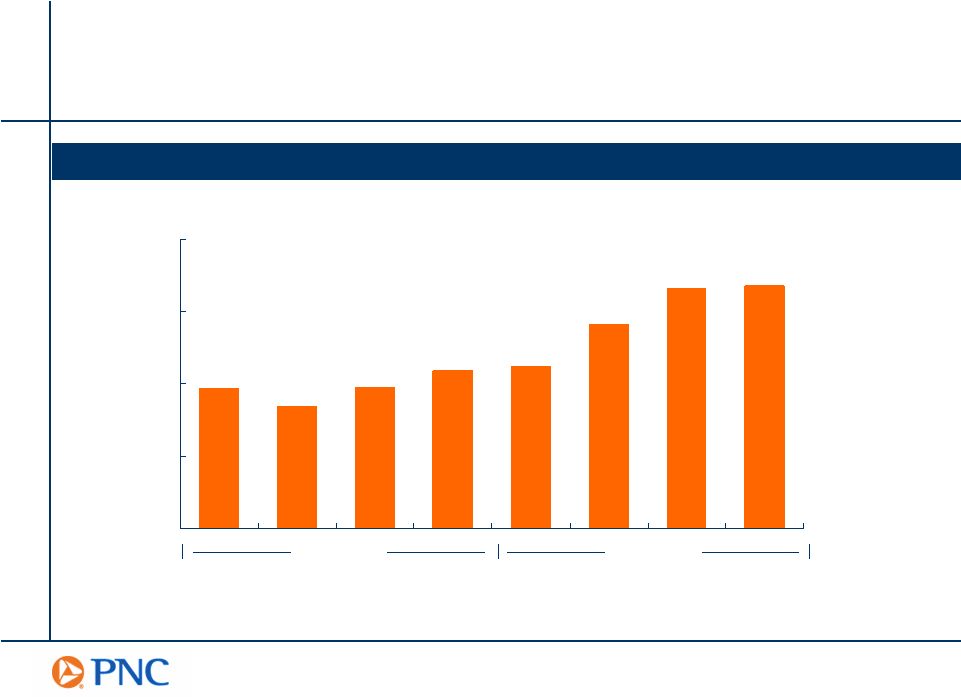

$500 $1,000 $1,500 $2,000 $2,500 $3,000 $3,500 $4,000 $4,500 Fee-Based Businesses Differentiate PNC Fee-Based Businesses Differentiate PNC Noninterest Income to Total Revenue 0% 10% 20% 30% 40% 50% 60% 70% 80% BK PNC FITB USB WB KEY WFC BBT STI NCC Information for the quarter ended 12/31/05 PNC amounts calculated in the Appendix Source: SNL DataSource Banking & Other BlackRock PFPC 9% CAGR 9% CAGR Strong Noninterest Income Growth $ millions Consolidated Noninterest Income 2002 2003 2004 2005 |

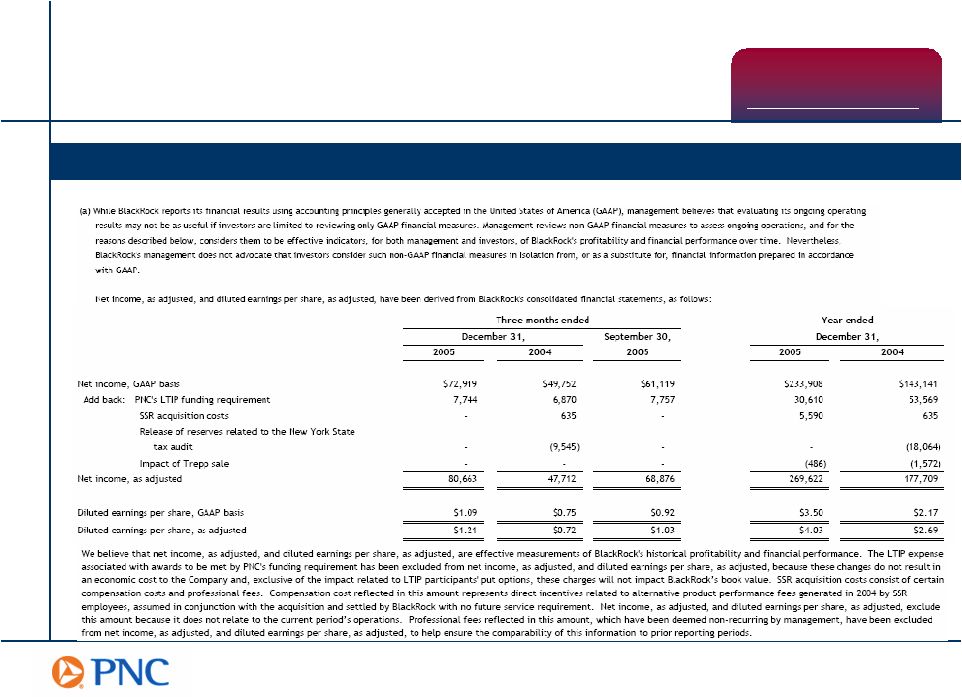

Reflects adjusted earnings for 2004 and 2005 as presented in BlackRocks publicly available filings and are reconciled to GAAP in the Appendix BlackRock A Growth Engine BlackRock A Growth Engine Assets Under Management Earnings $0 $50 $100 $150 $200 $250 $300 2002 2003 2004 2005 $0 $100 $200 $300 $400 $500 2002 2003 2004 2005 December 31 $273 $342 $453 $309 $270 $133 $155 $178 * * $143 $234 Adjusted Earnings* GAAP Earnings $ millions $ billions |

Improve efficiency Expand offshore Invest in and grow alternative investment products PFPC Strong Growth PFPC Strong Growth Servicing Statistics Strategies to Drive Growth Assets serviced ($ billions) Accounting / administration $830 +15% Domestic $754 +14% Offshore $76 +25% Shareholder accounts (in millions) Transfer agency 19 -10% Subaccounting 43 +19% Earnings ($ millions)

$104 +49% % Change vs. 2004 2005 December 31 |

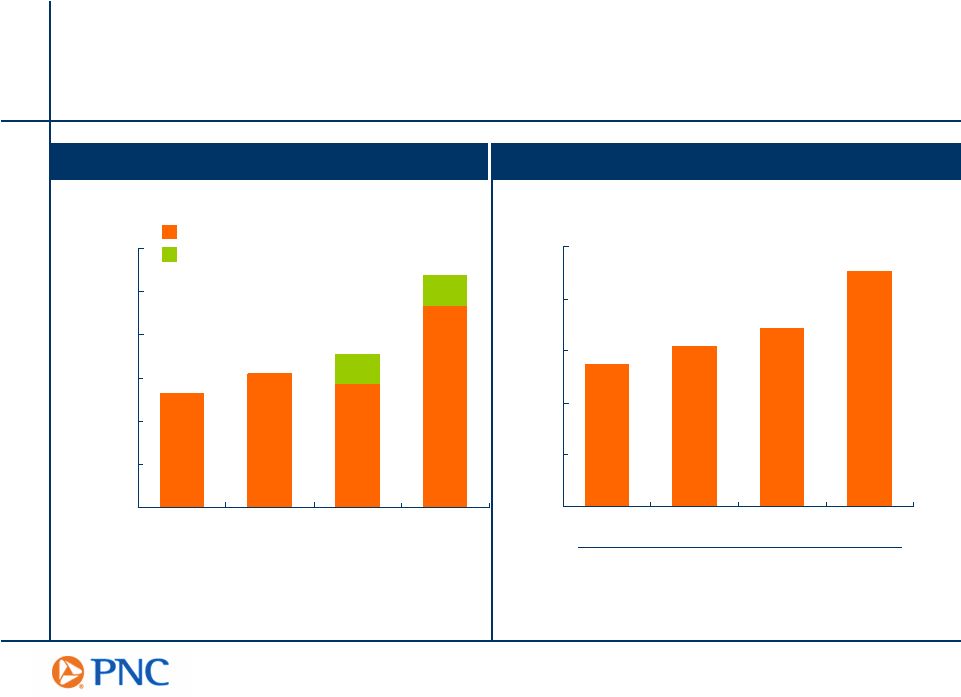

Corporate & Institutional Banking reported noninterest income for the years ended 12/31/04 and 12/31/05 was $573 million and $609 million, respectively; chart excludes net gains on institutional loans held for sale of $52 million and $7 million, respectively. $0 $250 $500 $750 $1,000 $1,250 $1,500 $1,750 $2,000 2004 2005 Year Ended December 31 Banking Growing Fee Income Banking Growing Fee Income $521 $1,223 $1,275 $602 +16% +4% Retail Banking Corporate & Institutional Banking * Geographic expansion Diversify product set Increase product penetration Leverage technology Strong Noninterest Income Growth Strategies to Drive Growth $ millions * * |

0.0 0.5 1.0 1.5 2.0 2002 2003 2004 2005 Increasing and Deepening Checking Relationships Increasing and Deepening Checking Relationships

Provides Opportunities for Deepening Relationships Average home equity loans +15% Consumer on-line banking users +19% Consumer on-line bill-pay users +81% Growth* * Growth is for 2005 vs. 2004 Retail Banking Checking Customer Base millions December 31 Small Business Consumer |

$5 $7 $9 $11 $13 $15 $17 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q $5 $7 $9 $11 $13 $15 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 0.00% 1.00% 2.00% 3.00% 4.00% 5.00% Growing a Valuable Core Deposit Base Growing a Valuable Core Deposit Base Relationship Strategy Generating Deposit Growth $ billions Retail Banking Average Certificates of Deposit Retail Banking Average Demand Deposits $ billions Average Federal Funds Rate Average Certificates of Deposit 2003 2004 2005 2003 2004 2005 |

Growing Deposits Faster Than Our Peers Growing Deposits Faster Than Our Peers Deposit Increase Compared to Peers Total interest-bearing deposits 18% 10% Total noninterest-bearing deposits 11% 10% Total deposits 16% 9% Average Balances 2005 vs. 2004 PNC Peer Median Source: SNL DataSource Peer median of super-regional banks as identified in the Appendix excluding PNC

|

Rising

Interest Rates Increase Value of PNCs Noninterest-Bearing

Deposits WFC 23 % BK 19 PNC 18 USB 16 STI 16 KEY 16 FITB 15 WB 15 NCC 14 BBT 14 0.00% 0.10% 0.20% 0.30% 0.40% 0.50% 0.60% 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q Noninterest-Bearing Deposits Becoming More Valuable Noninterest-Bearing Deposits Becoming More Valuable PNCs High Percentage of Noninterest-Bearing Funding Average Noninterest-Bearing Deposits to Average Earning Assets 2004 2005 Impact of Noninterest-Bearing Sources on PNCs Net Interest Margin 4Q05 Source: SNL DataSource |

Average

Loans Outstanding Improving Execution Driving Loan Growth Improving Execution Driving Loan Growth $0 $5 $10 $15 $20 $25 $30 $35 $40 $45 2004 2005 +14% +12% Retail Banking Corporate & Institutional Banking Drivers of Growth Retail Banking Focus on home equity loan product Offering enhanced Business Banking product set Corporate & Institutional Banking Leveraging national distribution in Commercial Real Estate and Asset Based Lending Delivering superior product set to middle market clients $ billions |

An Opportunity to Increase Securities Yields An Opportunity to Increase Securities Yields Yield on Securities Portfolio BK 4.44 % 3.68 % +76bp PNC 4.49 3.85 +64bp USB 4.85 4.38 +47bp WB 5.30 4.87 +43bp STI 4.47 4.06 +41bp BBT 4.29 3.98 +31bp KEY 4.78 4.52 +26bp WFC 5.81 5.62 +19bp FITB 4.41 4.21 +20bp NCC 5.14 5.07 +07bp Source: SNL DataSource and company filings Change Retained Portfolio Flexibility As of December 31, 2005 Effective duration of

2.6 years Weighted-average life of 4.0 years 11% is floating rate 16% matures or re-prices in next twelve months Increasing Yields on Securities Portfolio 4Q05 4Q04 |

$400 $450 $500 $550 $600 Net Interest Income Improving Net Interest Income Improving Consolidated Net Interest Income (Taxable-Equivalent Basis) Net interest income on a taxable-equivalent basis is reconciled to GAAP net interest income in the Appendix $ millions 2004 2005 |

One PNC Driving Improved Operating Leverage One PNC Driving Improved Operating Leverage Building a More Competitive Company Eliminate 3,000 positions Implement 2,400 ideas Achieve $400 million of total value 1,800 positions eliminated 88% of ideas are complete or in process Delivered $90 million in 2005. On track to capture $400 million of value by 2007 Expected Outcomes Update As of 12/31/05 |

Summary Summary Accomplished a great deal in 2005 Maintained a moderate risk profile that is key to improving consistency Executing strategies to improve operating leverage |

|

Appendix |

Cautionary Statement Regarding Forward-Looking Information Cautionary Statement Regarding Forward-Looking Information We make statements in this presentation, and we may from time to time make other statements, regarding our outlook or expectations for earnings, revenues, expenses and/or other matters regarding or affecting PNC that are forward-looking statements within the meaning of the Private Securities Litigation Reform Act. Forward-looking statements are typically identified by words such as believe, expect, anticipate, intend, outlook, estimate, forecast, project and other similar words and expressions. Forward- looking statements are subject to numerous assumptions, risks and

uncertainties, which change over time. Forward-looking statements speak only as of the date they are made. We do not assume any duty and do not undertake to update our forward-looking statements. Actual results or future events could differ, possibly materially, from those that we anticipated in our forward-looking statements, and future results could differ materially from our historical performance. In addition to factors that we have disclosed in our 2004 annual report on Form 10-K, our third quarter 2005 report on Form 10-Q, and in other reports that we file with the SEC (accessible on the SECs website at www.sec.gov and on or through PNCs corporate website at www.pnc.com), PNCs forward-looking statements are subject to, among others, the following risks and uncertainties, which could cause actual results or future events to differ materially from those that we anticipated in our forward-looking statements or from our historical performance: changes in political, economic or industry conditions, the interest rate environment,

or the financial and capital markets (including as a result of actions of the Federal Reserve Board affecting interest rates, the money supply, or otherwise reflecting changes in monetary policy), which could affect: (a) credit quality and the extent of our credit losses; (b) the extent of funding of

our unfunded loan commitments and letters of credit; (c) our allowances for loan and lease losses and unfunded loan commitments and letters of credit; (d)

demand for our credit or fee-based products and services; (e) our net interest income; (f) the value of assets under management and assets serviced, of private equity investments, of other debt and equity investments, of loans held for sale, or of other on-balance sheet or off-balance sheet assets; or (g) the availability and terms of funding necessary to meet our liquidity needs; the impact on us of legal and regulatory developments, including the following: (a) the resolution of legal proceedings or regulatory and other governmental inquiries; (b) increased litigation risk from recent regulatory and

other governmental developments; (c) the results of the regulatory examination process, our failure to satisfy the requirements of agreements with governmental agencies, and regulators future use of supervisory and enforcement tools; (d) legislative and regulatory reforms, including changes to

tax and pension laws; and (e) changes in accounting policies and

principles, with the impact of any such developments possibly affecting our ability to operate our businesses or our financial condition or results of operations or our reputation, which in turn could have an impact on such matters as business generation and retention, our ability to attract and retain management, liquidity and funding; the impact on us of changes in the nature and extent of our competition; the introduction, withdrawal, success and timing of our business initiatives and strategies; |

Cautionary Statement Regarding Forward-Looking Information (continued)

Cautionary Statement Regarding Forward-Looking Information (continued)

customer acceptance of our products and services, and our customers borrowing, repayment, investment and deposit practices; the impact on us of changes in the extent of customer or counterparty delinquencies,

bankruptcies or defaults, which could affect, among other things, credit

and asset quality risk and our provision for credit losses;

the ability to identify and effectively manage risks inherent in our businesses; how we choose to redeploy available capital, including the extent and timing of any

share repurchases and acquisitions or other investments in our businesses;

the impact, extent and timing of technological changes, the adequacy of intellectual

property protection, and costs associated with obtaining rights in intellectual property claimed by others; the timing and pricing of any sales of loans or other financial assets held for sale;

our ability to obtain desirable levels of insurance and to successfully submit claims

under applicable insurance policies; the relative and absolute investment performance of assets under management; and the extent of terrorist activities and international hostilities, increases or

continuations of which may adversely affect the economy and financial and capital markets generally or us specifically. Our future results are likely to be affected significantly by the results of the

implementation of our One PNC initiative, as discussed in this presentation. Generally, the amounts of our anticipated cost savings and revenue enhancements are

based to some extent on estimates and assumptions regarding future business performance and expenses, and these estimates and assumptions may prove to be inaccurate in some respects. Some or all of the above factors may cause the anticipated expense savings and revenue enhancements from that initiative

not to be achieved in their entirety, not to be accomplished within the

expected time frame, or to result in implementation charges beyond those currently contemplated or some other unanticipated adverse impact. Furthermore, the implementation of cost savings ideas may have unintended impacts on

our ability to attract and retain business and customers, while revenue

enhancement ideas may not be successful in the marketplace or may result in unintended costs. Assumed attrition required to achieve workforce reductions may not come in the right places or at the right times to meet planned goals. In addition, we grow our business from time to time by acquiring other financial services companies. Acquisitions in general present us with a number of risks and uncertainties related both to the acquisition transactions themselves and to the integration of the acquired businesses into PNC after closing. In particular, acquisitions may be substantially more expensive to complete (including the integration

of the acquired company) and the anticipated benefits, including

anticipated cost savings and strategic gains, may be significantly harder or take longer to achieve than expected. As a regulated financial institution, our |

Cautionary Statement Regarding Forward-Looking Information (continued)

Cautionary Statement Regarding Forward-Looking Information (continued)

pursuit of attractive acquisition opportunities could be negatively impacted due to regulatory delays or other regulatory issues. Regulatory and/or legal issues of an acquired business may cause reputational harm to PNC following the acquisition and integration of the acquired business into ours and may result in additional future costs and expenses arising as a result of those issues. Recent

acquisitions, including our acquisition of Riggs National Corporation, continue to present the integration and other post-closing risks and uncertainties described above. You can find additional information on the foregoing risks and uncertainties and

additional factors that could affect the results anticipated in our forward-looking statements or from our historical performance in the reports that we file with the

SEC. You can access our SEC reports on the SECs website at www.sec.gov and on or through our corporate website at www.pnc.com. Also, risks and uncertainties that could affect the results anticipated in forward-looking statements or from historical performance relating to our majority-owned subsidiary BlackRock, Inc. are discussed in more detail in BlackRocks filings with the SEC, accessible on the SECs website and on or through BlackRocks website at www.blackrock.com. Any annualized, proforma, estimated, third party or consensus numbers in this

presentation are used for illustrative or comparative purposes only and may not reflect actual results. Any consensus earnings estimates are calculated based on

the earnings projections made by analysts who cover that company. The analysts opinions, estimates or forecasts (and therefore the consensus earnings estimates) are theirs alone, are not those of PNC or its management, and may not reflect PNCs actual or anticipated results. |

Non-GAAP to GAAP Reconcilement Non-GAAP to GAAP Reconcilement Business segments Retail Banking $682 $610 24% Corporate & Institutional Banking 480 443 28% BlackRock 234 143 28% PFPC 104 70 32% Total business segments 1,500 1,266 18% 26% Minority interest in income of BlackRock (71) (42) Other (104) (27) Total consolidated $1,325 $1,197 11% 17% 2005 2004 $ millions For the year ended December 31 % Change Earnings Return on Avg Capital * 2005 Appendix Business Earnings and Return on Capital * Percentages for BlackRock and PFPC reflect return on average equity

|

Non-GAAP to GAAP Reconcilement Non-GAAP to GAAP Reconcilement BlackRock $369 21.6% PFPC 215 12.6% Banking businesses 515 30.2% Other 52 3.0% Total consolidated $1,151 $1,706 67.4% Noninterest Income $ millions Consolidated Total Revenue Noninterest Income to Consolidated Total Revenue* Quarter Ended 12/31/05 33.2% Appendix Sum of net interest income and noninterest income * Noninterest Income to Total Revenue* |

Non-GAAP to GAAP Reconcilement Non-GAAP to GAAP Reconcilement $ millions, except earnings per share Appendix BlackRock Adjusted Earnings |

Non-GAAP to GAAP Reconcilement Non-GAAP to GAAP Reconcilement $ millions Net interest income, GAAP basis $494 $481 $491 $503 Taxable-equivalent adjustment 3 4 7 6 Net interest income, taxable-equivalent basis $497 $485 $498 $509 1Q04 3Q04 2Q04 4Q04 Appendix Consolidated Net Interest Income Net interest income, GAAP basis $506 $534 $559 $555 Taxable-equivalent adjustment 6 7 7 13 Net interest income, taxable-equivalent basis $512 $541 $566 $568 1Q05 3Q05 2Q05 4Q05 |

Peer Groups Peer Groups BB&T Corporation BBT The Bank of New York Company, Inc. BK Fifth Third Bancorp FITB KeyCorp KEY National City Corporation NCC The PNC Financial Services Group, Inc. PNC SunTrust Banks, Inc. STI U.S. Bancorp USB Wachovia Corporation WB Wells Fargo & Company WFC Appendix Ticker Super-Regional Banks |