SLIDE PRESENTATION

Published on November 16, 2004

EXHIBIT 99.1

The PNC Financial Services Group, Inc.

Merrill Lynch

Banking and Financial Services Conference

New York, NY November 16, 2004

Cautionary Statement Regarding Forward-Looking Information

This presentation contains forward-looking statements regarding our outlook or expectations relating to PNCs future business, operations, financial condition, financial performance and asset quality. Forward-looking statements are necessarily subject to numerous assumptions, risks and uncertainties.

The forward-looking statements in this presentation are qualified by the factors affecting forward-looking statements identified in the more detailed Cautionary Statement included in the written materials we distributed at this conference and in the version of the presentation materials posted on our corporate website at www.pnc.com, as well as those factors previously disclosed in our 2003 Form 10-K and other SEC reports (accessible on the SECs website at www.sec.gov and on our corporate website). Future events or circumstances may change our outlook or expectations and may also affect the nature of the assumptions, risks and uncertainties to which our forward-looking statements are subject. The forward-looking statements in this presentation speak only as of the date of this presentation. We do not assume any duty and do not undertake to update those statements.

This presentation may also include a discussion of non-GAAP financial measures, which, to the extent not so qualified therein, is qualified by GAAP reconciliation information available on our corporate website at www.pnc.com under For Investors.

Global fund processing:

PFPC with offices in U.S., Ireland & Luxembourg

PNC A Diversified Financial Services Company

Business Leadership

Regional Community Banking

A leading community bank in PNCs major markets

8th-largest national ATM network

Wholesale Banking

Top 10 bank-owned Treasury Management business

One of the nations largest asset-based lenders

PNC Advisors One of the nations largest bank wealth managers

BlackRock

One of the nations largest publicly traded

asset managers

PFPC

Largest full-service mutual fund transfer agent in U.S.

Regional, National and Global Businesses

Global investment management:

BlackRock with offices in U.S., Edinburgh, Hong Kong, Sydney & Tokyo

PA NJ IN OH DE

KY

PNC Bank Branches PNC Employees/Offices

Todays

PNCs plans to accelerate

Discussion banking revenue growth

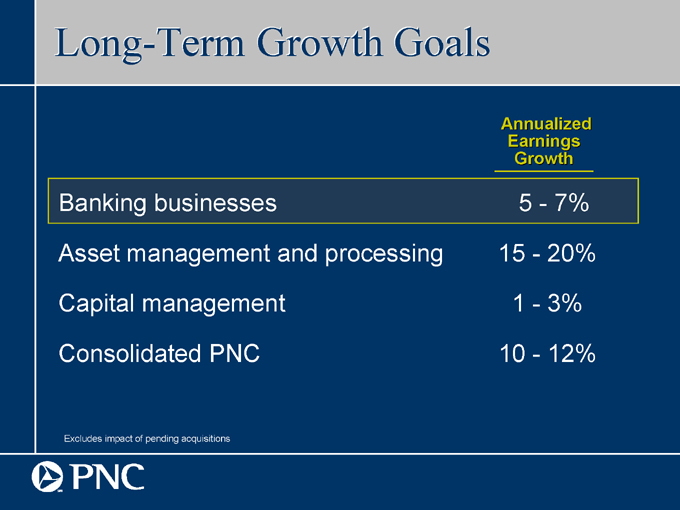

Excludes impact of pending acquisitions

Long-Term Growth Goals

Annualized Earnings Growth

Banking businesses 5 - 7%

Asset management and processing 15 - 20%

Capital management 1 - 3%

Consolidated PNC 10 - 12%

Regional Community Banking Growth Strategies

We Are Focused on Acquiring, Growing and Retaining Clients by

Increasing and deepening checking relationships

Growing valuable home equity loan portfolio Capturing small business opportunities

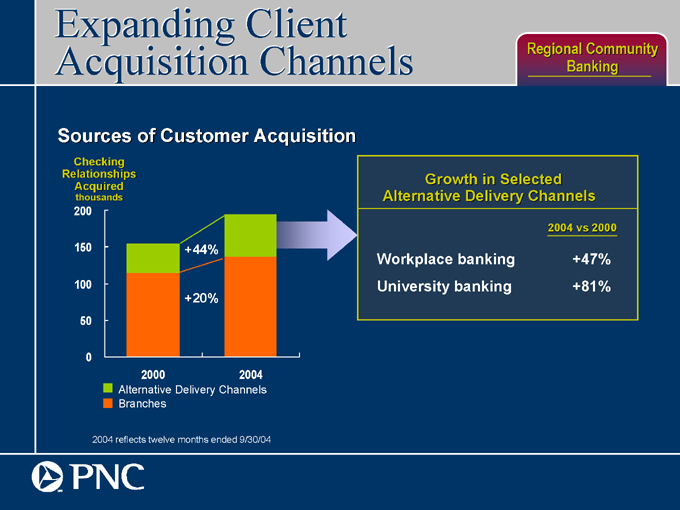

Expanding Client Acquisition Channels

Sources of Customer Acquisition

Checking Relationships Acquired thousands

200 150 100 50 0

+44%

+20%

2000 2004

Alternative Delivery Channels Branches

Regional Community Banking

Growth in Selected

Alternative Delivery Channels

2004 vs 2000

Workplace banking +47%

University banking +81%

2004 reflects twelve months ended 9/30/04

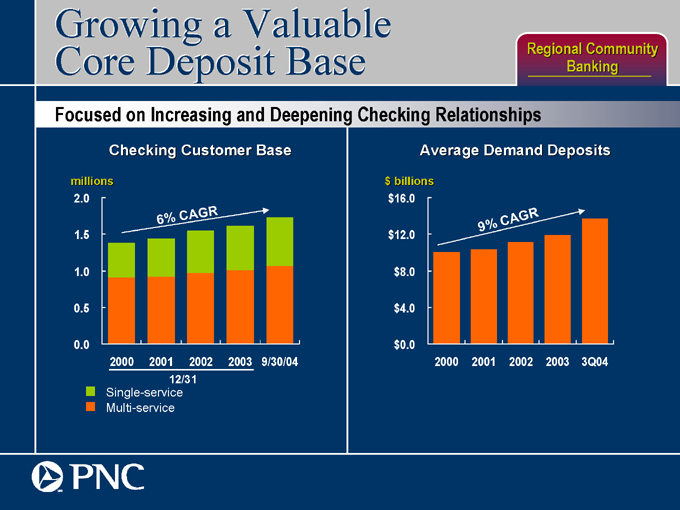

Growing a Valuable Core Deposit Base

Regional Community Banking

Focused on Increasing and Deepening Checking Relationships

Checking Customer Base millions

2.0 1.5 1.0 0.5 0.0

2000 2001 2002 2003 9/30/04

6%

CAGR

12/31

Single-service Multi-service

Average Demand Deposits $ billions $16.0

$12.0 $8.0 $4.0 $0.0

2000 2001 2002 2003 3Q04

9 %

CAGR

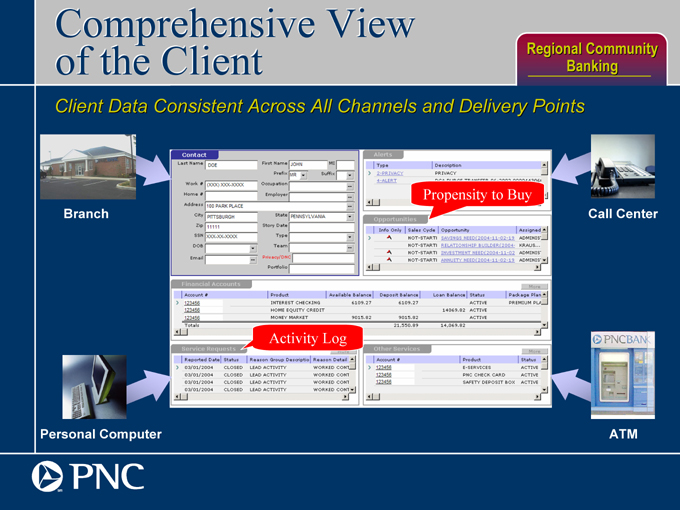

Comprehensive View of the Client

Regional Community Banking

Client Data Consistent Across All Channels and Delivery Points

Branch

Personal Computer

Call Center

Propensity to Buy

Activity Log

ATM

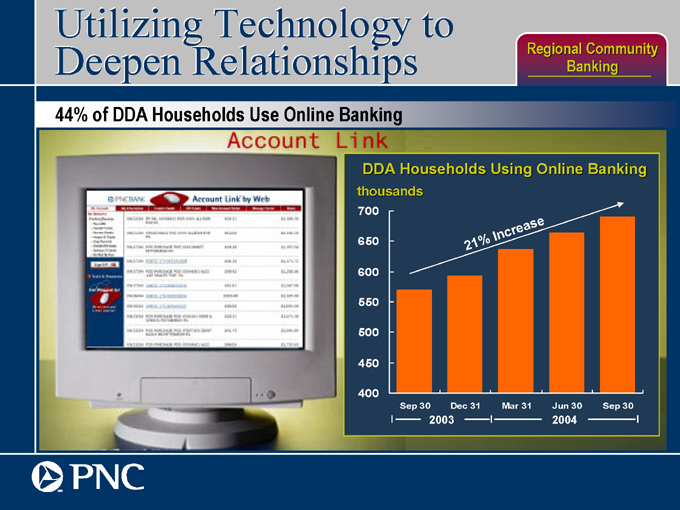

Utilizing Technology to Deepen Relationships

Regional Community Banking

44% of DDA Households Use Online Banking

Account Link

DDA Households Using Online Banking

thousands

700

650

600 550 500

450

400

21% Increase

Sep 30 Dec 31 Mar 31 Jun 30 Sep 30

2003 2004

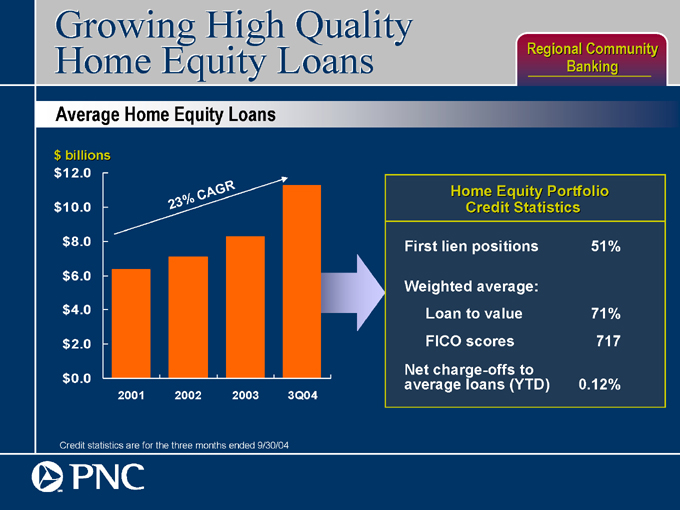

Growing High Quality Home Equity Loans

Average Home Equity Loans $ billions $12.0

$10.0 $8.0 $6.0 $4.0 $2.0 $0.0

2001 2002 2003 3Q04

2 3 %

C A

G R

Regional Community Banking

Home Equity Portfolio

Credit Statistics

First lien positions 51%

Weighted average:

Loan to value 71%

FICO scores 717

Net charge-offs to average loans (YTD) 0.12%

Credit statistics are for the three months ended 9/30/04

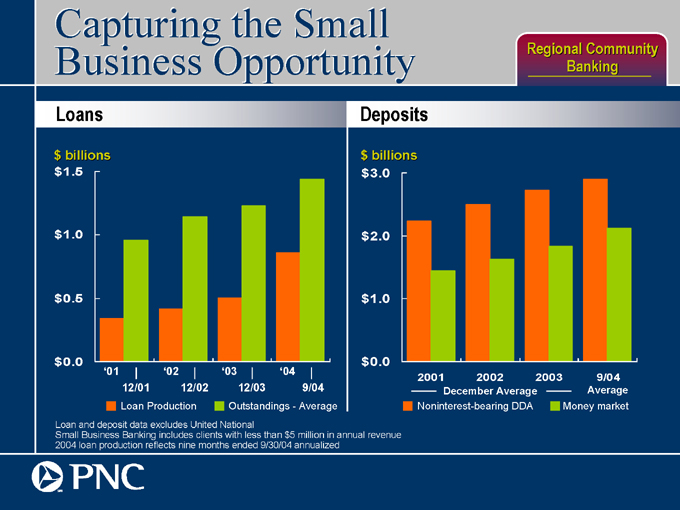

Capturing the Small Business Opportunity

Regional Community Banking

Loans $ billions $1.5

$1.0 $0.5 $0.0

01 02 03 04

12/01 12/02 12/03 9/04

Loan Production Outstandings - Average

Deposits $ billions $3.0

$2.0 $1.0 $0.0

2001 2002 2003 9/04

December Average Average

Noninterest-bearing DDA Money market

Loan and deposit data excludes United National

Small Business Banking includes clients with less than $5 million in annual revenue 2004 loan production reflects nine months ended 9/30/04 annualized

Wholesale Banking Growth Strategies

Selectively pursue large corporate business

Deliver large bank capabilities to the middle market

Leverage national reach and technology-oriented, fee-based products

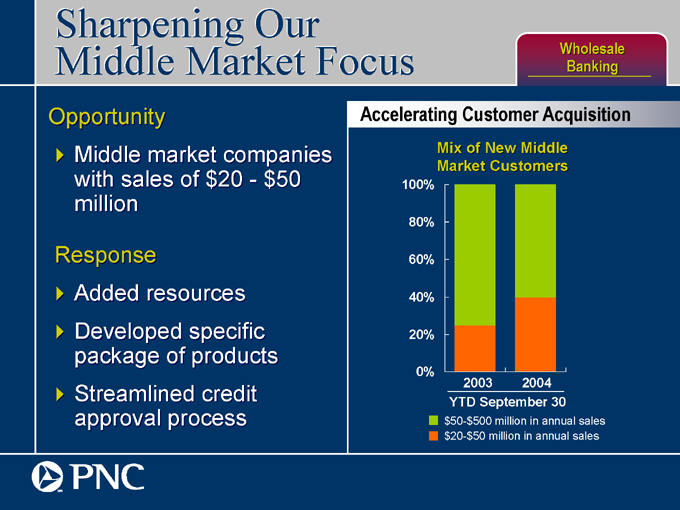

Sharpening Our Middle Market Focus

Wholesale Banking

Opportunity

Middle market companies with sales of $20 - $50 million

Response

Added resources Developed specific package of products Streamlined credit approval process

Accelerating Customer Acquisition

Mix of New Middle Market Customers

100% 80% 60% 40% 20% 0%

2003 2004

YTD September 30

$50-$500 million in annual sales $20-$50 million in annual sales

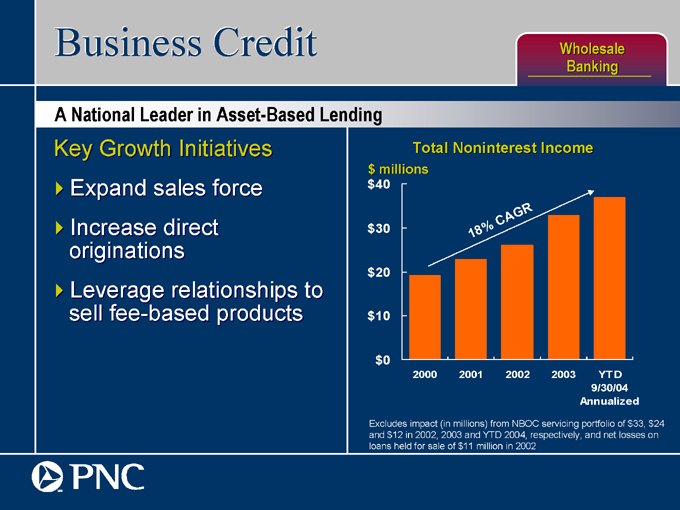

Business Credit

Wholesale Banking

A National Leader in Asset-Based Lending

Key Growth Initiatives

Expand sales force Increase direct originations Leverage relationships to sell fee-based products

Total Noninterest Income $ millions $40

$30 $20 $10 $0

2000 2001 2002 2003 YTD

9/30/04 Annualized

1 8 %

CAGR

Excludes impact (in millions) from NBOC servicing portfolio of $33, $24 and $12 in 2002, 2003 and YTD 2004, respectively, and net losses on loans held for sale of $11 million in 2002

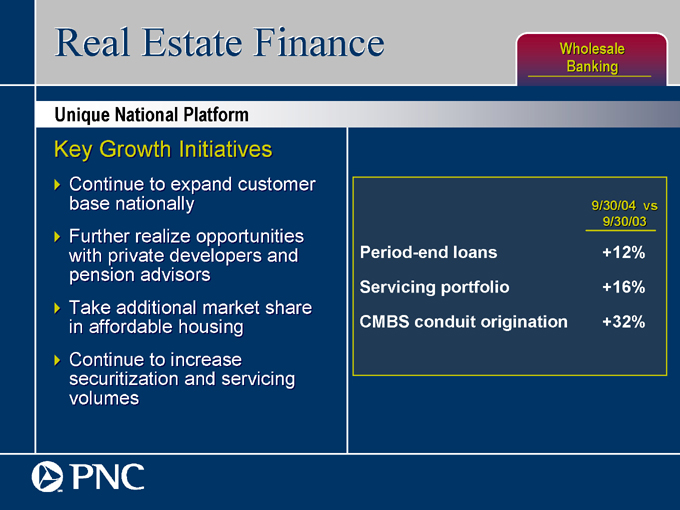

9/30/04 vs 9/30/03

Period-end loans +12%

Servicing portfolio +16%

CMBS conduit origination +32%

Real Estate Finance

Wholesale Banking

Unique National Platform

Key Growth Initiatives

Continue to expand customer base nationally Further realize opportunities with private developers and pension advisors Take additional market share in affordable housing Continue to increase securitization and servicing volumes

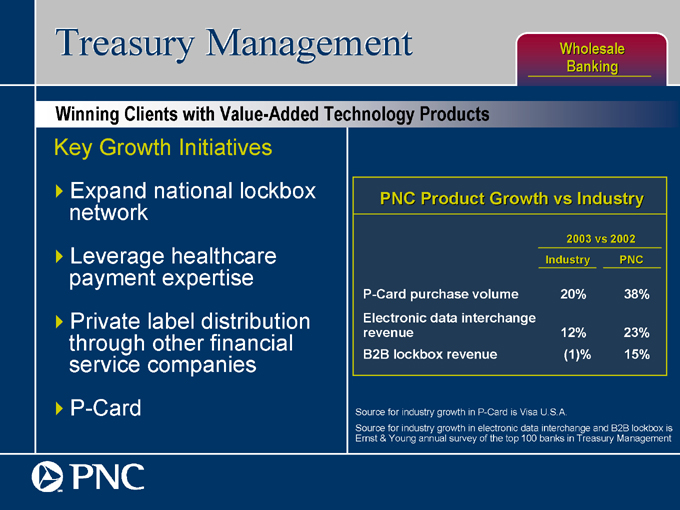

Source for industry growth in P-Card is Visa U.S.A.

Source for industry growth in electronic data interchange and B2B lockbox is Ernst & Young annual survey of the top 100 banks in Treasury Management

Treasury Management

Wholesale Banking

Winning Clients with Value-Added Technology Products

Key Growth Initiatives

Expand national lockbox network Leverage healthcare payment expertise Private label distribution through other financial service companies P-Card

PNC Product Growth vs Industry

2003 vs 2002

Industry PNC

P-Card purchase volume 20% 38%

Electronic data interchange revenue 12% 23%

B2B lockbox revenue (1)% 15%

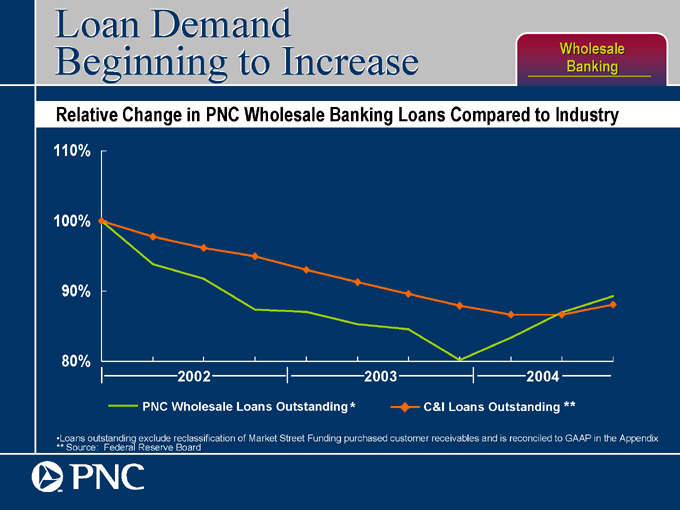

Loan Demand Beginning to Increase

Wholesale Banking

Relative Change in PNC Wholesale Banking Loans Compared to Industry

110% 100% 90% 80%

2002 2003 2004

PNC Wholesale Loans Outstanding* C&I Loans Outstanding **

Loans outstanding exclude reclassification of Market Street Funding purchased customer receivables and is reconciled to GAAP in the Appendix ** Source: Federal Reserve Board

Strengthen sales and relationship management Create a distinctive client experience Leverage other PNC businesses

PNC Advisors Growth Strategies

Results reflect nine months ended September 30, 2004 versus nine months ended September 30, 2003

Continuing to Strengthen Sales Management

PNC Advisors

Results Are Promising

Increased pipeline opportunities by 53% Realized double digit increase in wealth management sales Leveraged banking products to attract new customers

Average consumer loans outstanding up 14%

Source: Axiom

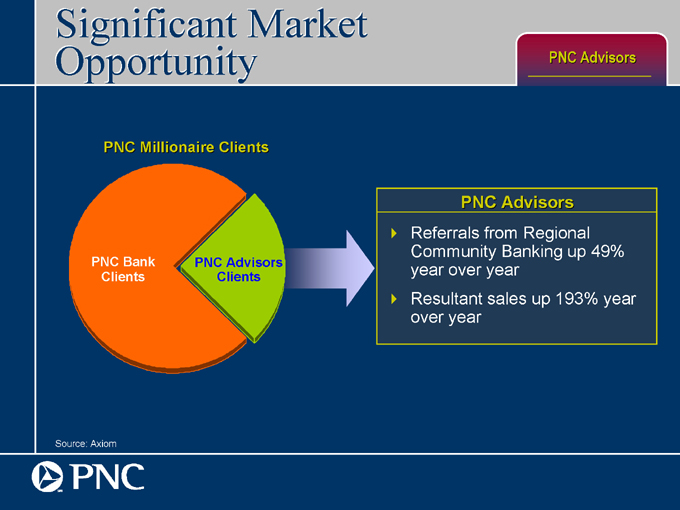

Significant Market Opportunity

PNC Advisors

PNC Millionaire Clients

PNC Bank Clients

PNC Advisors Clients

PNC Advisors

Referrals from Regional Community Banking up 49% year over year Resultant sales up 193% year over year

Source: SNL Financial

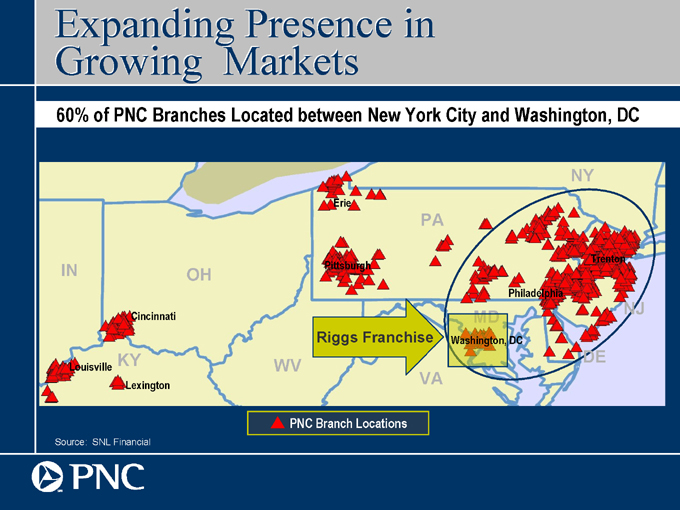

Expanding Presence in Growing Markets

60% of PNC Branches Located between New York City and Washington, DC

NY

Erie

PA

Trenton IN Pittsburgh

OH

Philadelphia

NJ

Cincinnati MD

Riggs Franchise Washington, DC

KY DE

Louisville WV

Lexington VA

PNC Branch Locations

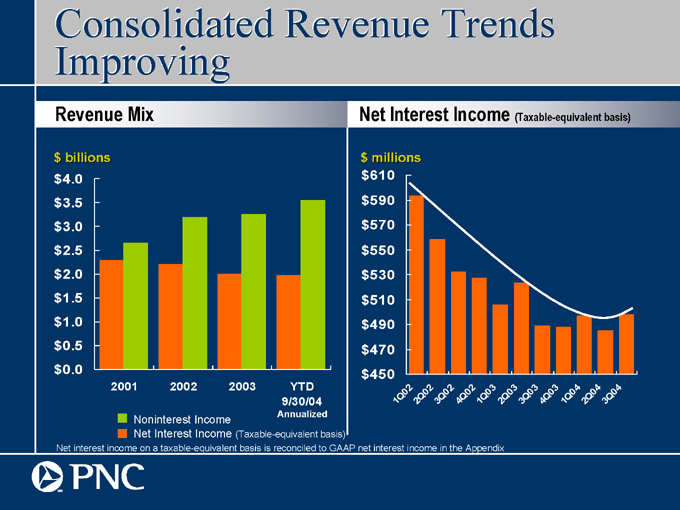

Net interest income on a taxable-equivalent basis is reconciled to GAAP net interest income in the Appendix

Consolidated Revenue Trends Improving

Revenue Mix

$ billions

$4.0

$3.5

$3.0

$2.5

$2.0

$1.5

$1.0

$0.5

$0.0

2001 2002 2003

YTD 9/30/04

Annualized

Noninterest Income

Net Interest Income (Taxable-equivalent basis)

Net Interest Income (Taxable-equivalent basis) $ millions $610 $590 $570 $550 $530 $510 $490 $470 $450

1Q02 2Q02 3Q02 4Q02 1Q03 2Q03 3Q03 4Q03 1Q04 2Q04 3Q04

Every day is an opportunity to do more

Appendix

Cautionary Statement Regarding Forward-Looking Information

We make statements in this presentation, and we may from time to time make other statements, regarding our outlook or expectations for earnings, revenues, expenses, capital levels, asset quality or other future financial or business performance, strategies or expectations, or the impact of legal, regulatory or supervisory matters on our business operations or performance, that are forward-looking statements. Forward-looking statements are typically identified by words or phrases such as believe, feel, expect, anticipate, intend, outlook, estimate, forecast, project, position, target, assume, achievable, potential, strategy, goal, objective, plan, aspiration, outcome, continue, remain, maintain, seek, strive, trend, and variations of such words and similar expressions, or future or conditional verbs such as will, would, should, could, might, can, may or similar expressions.

Forward-looking statements are subject to numerous assumptions, risks and uncertainties, which change over time. Our forward-looking statements speak only as of the date they are made. We do not assume any duty and do not undertake to update our forward-looking statements. Actual results or future events could differ, possibly materially, from those that we anticipated in our forward-looking statements, and future results could differ materially from our historical performance. The factors that we have previously disclosed in our SEC reports (accessible on our corporate website at www.pnc.com and on the SECs website at www.sec.gov) and the following factors, among others, could cause actual results or future events to differ materially from those that we anticipated in our forward-looking statements or from our historical performance: (1) changes in political, economic or industry conditions, the interest rate environment or financial and capital markets (including as a result of actions of the Federal Reserve Board affecting interest rates or the money supply or otherwise reflecting changes in monetary policy), which could affect: (a) credit quality and the extent of our credit losses; (b) the extent of funding of our unfunded loan commitments and letters of credit; (c) our allowances for loan and lease losses and unfunded loan commitments and letters of credit; (d) demand for our credit or fee-based products and services; (e) our net interest income; (f) the value of assets under management and assets serviced, of private equity investments, of other debt and equity investments, of loans held for sale, or of other on-balance sheet or off-balance sheet assets; or (g) the availability and terms of funding necessary to meet our liquidity needs; (2) the impact on us of legal and regulatory developments (including the following: (a) the resolution of legal proceedings or regulatory and other governmental inquiries; (b) increased litigation risk from recent regulatory and other governmental developments; (c) the results of the regulatory examination process, our failure to satisfy the requirements of agreements with governmental agencies, and regulators future use of supervisory and enforcement tools; (d) legislative and regulatory reforms, including changes to tax law; and (e) changes in accounting policies and principles), with the impact of any such developments possibly affecting our ability to operate our businesses or our financial condition or results of operations or our reputation, which in turn could have an impact on such matters as business generation and retention, our ability to attract and retain management, liquidity and funding; (3) the impact on us of changes in the nature or extent of our competition; (4) the introduction, withdrawal, success and timing of our business initiatives and strategies; (5) customer acceptance of our products and services, and our customers borrowing, repayment, investment and deposit practices; (6) the impact on us of

changes in the extent of customer or counterparty delinquencies, bankruptcies or defaults, which could affect, among other things, credit and asset quality risk and our provision for credit losses; (7) the ability to identify and effectively manage risks inherent in our business;

Cautionary Statement Regarding Forward-Looking Information (continued)

(8) how we choose to redeploy available capital, including the extent and timing of any share repurchases and acquisitions or other investments in our businesses;

(9) the impact, extent and timing of technological changes, the adequacy of intellectual property protection, and costs associated with obtaining rights in intellectual property claimed by others;

(10) the timing and pricing of any sales of loans or other financial assets held for sale;

(11) our ability to obtain desirable levels of insurance, and whether or not insurance coverage for claims by PNC is denied;

(12) the relative and absolute investment performance of assets under management; and

(13) the extent of terrorist activities and international hostilities, increases or continuations of which may adversely affect the economy and financial and capital markets generally or us specifically.

In addition, our forward-looking statements are also subject to risks and uncertainties related to our pending acquisition of Riggs National Corporation and the expected consequences of the integration of the remaining Riggs businesses at closing into PNC, including the following: (a) completion of the transaction is dependent on, among other things, receipt of stockholder and regulatory approvals, and we cannot at this point predict with precision when those approvals may be obtained or if they will be received at all; (b) successful completion of the transaction and our ability to realize the benefits that we anticipate from the acquisition also depend on the nature of any future developments with respect to Riggs regulatory issues, the ability to comply with the terms of all current or future regulatory requirements (including any related action plan) resulting from these issues, and the extent of future costs and expenses arising as a result of these issues, including the impact of increased litigation risk and any claims for indemnification or advancement of costs; (c) the transaction may be materially more expensive to complete than we anticipate as a result of unexpected factors or events; (d) the integration into PNC of the Riggs business and operations that we acquire, which will include conversion of Riggs different systems and procedures, may take longer than we anticipate, may be more costly than we anticipate, or may have unanticipated adverse results relating to Riggs or PNCs existing businesses; (e) it may take longer that we expect to realize the anticipated cost savings of the acquisition, and those anticipated cost savings may not be achieved or may not be achieved in their entirety; and (f) the anticipated strategic and other benefits of the acquisition to us are dependent in part on the future performance of Riggs business, and there can be no assurance as to actual future results, which could be impacted by various factors, including the risks and uncertainties generally related to the performance of PNCs and Riggs businesses (with respect to Riggs, see Riggs SEC reports, also accessible on the SECs website at www.sec.gov) or due to factors related to the acquisition of Riggs and the process of integrating Riggs business at closing into ours.

Other mergers, acquisitions, restructurings, divestitures, business alliances or similar transactions, including our recently completed acquisitions of United National Bancorp and the loan origination business of Aviation Finance Group, LLC, and our pending acquisition of SSRM Holdings Inc., will also be subject to similar risks and uncertainties related to our ability to realize expected cost savings or revenue enhancements or to implement integration and strategic plans and, in the case of SSRM Holdings Inc., related to our successful completion of the transaction.

In addition, risks and uncertainties that could affect the results anticipated in forward-looking statements or from historical performance that involve BlackRock are discussed in more detail and additional factors are identified in BlackRocks SEC reports, accessible on the SECs website or on BlackRocks website at www.blackrock.com.

Any annualized, proforma, estimated, third party or consensus numbers in this presentation are used for illustrative or comparative purposes only and may not reflect actual results. Any consensus earnings estimates are calculated based on the earnings projections made by analysts who cover that company. The analysts opinions, estimates or forecasts (and therefore the consensus earnings estimates) are theirs alone, are not those of PNC or its management, and may not reflect PNCs actual or anticipated results.

Additional Information About the Proposed Riggs National Corporation Acquisition

The PNC Financial Services Group, Inc. and Riggs National Corporation have filed a proxy statement/prospectus and will file other relevant documents concerning the merger with the United States Securities and Exchange Commission (the SEC). WE URGE INVESTORS TO READ THE PROXY STATEMENT/PROSPECTUS AND ANY OTHER DOCUMENTS TO BE FILED WITH THE SEC IN

CONNECTION WITH THE MERGER OR INCORPORATED BY REFERENCE IN THE PROXY STATEMENT/PROSPECTUS, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. Investors will be able to obtain these documents free of charge at the SECs web site (www.sec.gov). In addition, documents filed with the SEC by The PNC Financial Services Group, Inc. will be available free of charge from Shareholder Relations at (800) 843-2206. (800) Documents filed with the SEC by Riggs will be available free of charge from www.riggsbank.com.

The directors, executive officers, and certain other members of management of Riggs may be soliciting proxies in favor of the merger from its shareholders. For information about these directors, executive officers, and members of management, shareholders are asked to refer to Riggss most recent annual meeting proxy statement, which is available at the web addresses provided in the preceding paragraph.

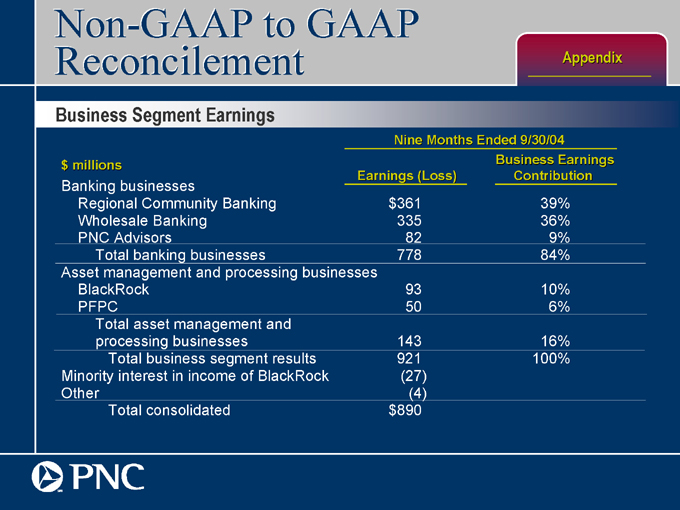

Non-GAAP to GAAP Reconcilement

Appendix

Business Segment Earnings

Nine Months Ended 9/30/04

Business Earnings

$ millions Earnings (Loss) Contribution

Banking businesses

Regional Community Banking $361 39%

Wholesale Banking 335 36%

PNC Advisors 82 9%

Total banking businesses 778 84%

Asset management and processing businesses

BlackRock 93 10%

PFPC 50 6%

Total asset management and processing businesses 143 16%

Total business segment results 921 100%

Minority interest in income of BlackRock (27)

Other (4)

Total consolidated $890

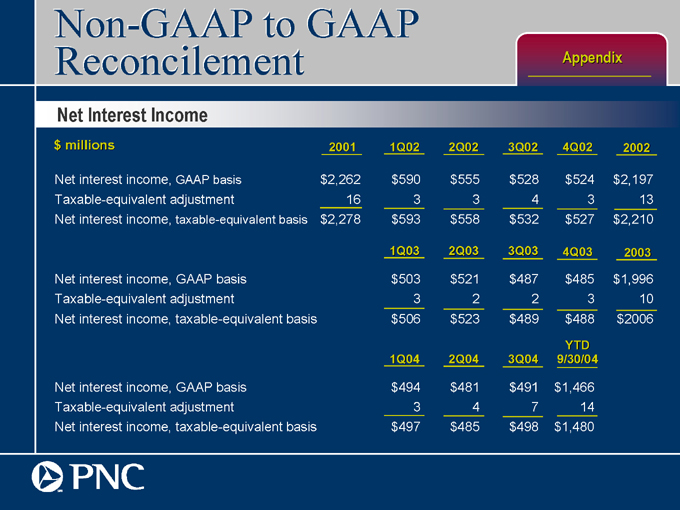

Non-GAAP to GAAP Reconcilement

Appendix

Net Interest Income

$ millions 2001 1Q02 2Q02 3Q02 4Q02 2002

Net interest income, GAAP basis $2,262 $590 $555 $528 $524 $2,197

Taxable-equivalent adjustment 16 3 3 4 3 13

Net interest income, taxable-equivalent basis $2,278 $593 $558 $532 $527 $2,210

1Q03 2Q03 3Q03 4Q03 2003

Net interest income, GAAP basis $503 $521 $487 $485 $1,996

Taxable-equivalent adjustment 3 2 2 3 10

Net interest income, taxable-equivalent basis $506 $523 $489 $488 $2006

YTD

1Q04 2Q04 3Q04 9/30/04

Net interest income, GAAP basis $494 $481 $491 $1,466

Taxable-equivalent adjustment 3 4 7 14

Net interest income, taxable-equivalent basis $497 $485 $498 $1,480

Non-GAAP to GAAP Reconcilement

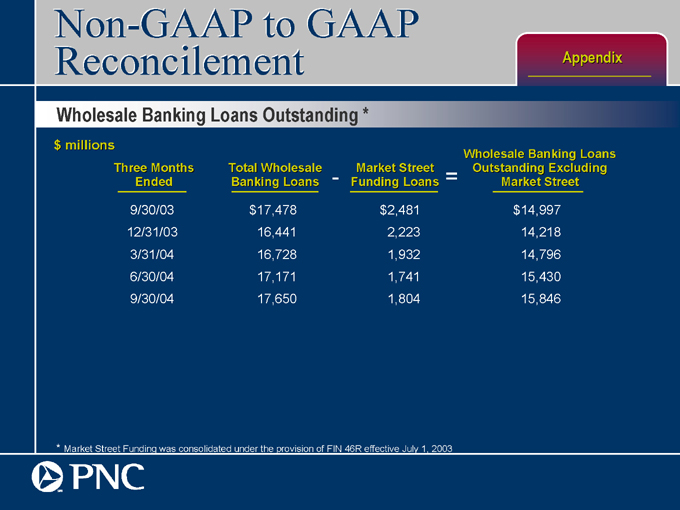

Appendix

Wholesale Banking Loans Outstanding *

$ millions Wholesale Banking Loans

Three Months Total Wholesale - Market Street = Outstanding Excluding

Ended Banking Loans Funding Loans Market Street

9/30/03 $17,478 $2,481 $14,997

12/31/03 16,441 2,223 14,218

3/31/04 16,728 1,932 14,796

6/30/04 17,171 1,741 15,430

9/30/04 17,650 1,804 15,846

* Market Street Funding was consolidated under the provision of FIN 46R effective July 1, 2003