10-Q: Quarterly report pursuant to Section 13 or 15(d)

Published on May 2, 2023

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

______________________________________

FORM 10-Q

______________________________________

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended March 31, 2023

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission file number 001-09718

The PNC Financial Services Group, Inc.

(Exact name of registrant as specified in its charter)

___________________________________________________________

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

|||||||

(Address of principal executive offices, including zip code)

(888 ) 762-2265

(Registrant’s telephone number including area code)

(Former name, former address and former fiscal year, if changed since last report)

___________________________________________________________

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol(s) |

Name of Each Exchange

on Which Registered

|

||||||

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company”, and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | ||||||||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||||||||

| Emerging growth company | ||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☒

As of April 18, 2023, there were 399,108,019 shares of the registrant’s common stock ($5 par value) outstanding.

THE PNC FINANCIAL SERVICES GROUP, INC.

Cross-Reference Index to First Quarter 2023 Form 10-Q

| Pages | |||||

| PART I – FINANCIAL INFORMATION | |||||

| Item 1. Financial Statements (Unaudited). | |||||

| Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations (MD&A). | |||||

| Item 3. Quantitative and Qualitative Disclosures about Market Risk. | 21-38, 49-50, 83-89 |

||||

| Item 4. Controls and Procedures. | |||||

| MD&A TABLE REFERENCE | ||||||||

| Table | Description | Page | ||||||

| 1 | ||||||||

| 2 | ||||||||

| 3 | ||||||||

| 4 | ||||||||

| 5 | ||||||||

| 6 | ||||||||

| 7 | ||||||||

| 8 | ||||||||

| 9 | ||||||||

| 10 | ||||||||

| 11 | ||||||||

| 12 | ||||||||

| 13 | ||||||||

| 14 | ||||||||

| 15 | ||||||||

| 16 | ||||||||

| 17 | ||||||||

| 18 | ||||||||

| 19 | ||||||||

| 20 | ||||||||

| 21 | ||||||||

| 22 | ||||||||

| 23 | ||||||||

| 24 | ||||||||

| 25 | ||||||||

| 26 | ||||||||

| 27 | ||||||||

| 28 | ||||||||

| 29 | ||||||||

| 30 | ||||||||

| 31 | ||||||||

| 32 | ||||||||

| 33 | ||||||||

| 34 | ||||||||

| NOTES TO CONSOLIDATED FINANCIAL STATEMENTS TABLE REFERENCE | ||||||||

| Table | Description | Page | ||||||

| 35 | ||||||||

| 36 | ||||||||

| 37 | ||||||||

| 38 | ||||||||

| 39 | ||||||||

| 40 | ||||||||

| 41 | ||||||||

| 42 | ||||||||

| 43 | ||||||||

| 44 | ||||||||

| 45 | ||||||||

| 46 | ||||||||

| 47 | ||||||||

| 48 | ||||||||

| 49 | ||||||||

| 50 | ||||||||

| 51 | ||||||||

| 52 | ||||||||

| 53 | ||||||||

| 54 | ||||||||

| 55 | ||||||||

| 56 | ||||||||

| 57 | ||||||||

| 58 | ||||||||

| 59 | ||||||||

| 60 | ||||||||

| 61 | ||||||||

| 62 | ||||||||

| 63 | ||||||||

| 64 | ||||||||

| 65 | ||||||||

| 66 | ||||||||

| 67 | ||||||||

| 68 | ||||||||

| 69 | ||||||||

| 70 | ||||||||

| 71 | ||||||||

| 72 | ||||||||

| 73 | ||||||||

| 74 | ||||||||

| 75 | ||||||||

| 76 | ||||||||

| 77 | ||||||||

| 78 | ||||||||

| 79 | ||||||||

FINANCIAL REVIEW

THE PNC FINANCIAL SERVICES GROUP, INC.

This Financial Review, including the Consolidated Financial Highlights, should be read together with our unaudited Consolidated Financial Statements and unaudited Statistical Information included elsewhere in this Quarterly Report on Form 10-Q (the “Report” or “Form 10-Q”) and with Items 6, 7, 8 and 9A of our 2022 Annual Report on Form 10-K (our “2022 Form 10-K”). For information regarding certain business, regulatory and legal risks, see the following: the Risk Management section of this Financial Review and of Item 7 in our 2022 Form 10-K; Item 1A Risk Factors included in this Report and our 2022 Form 10-K; and the Commitments and Legal Proceedings Notes included in this Report and Item 8 of our 2022 Form 10-K. Also, see the Cautionary Statement Regarding Forward-Looking Information section in this Financial Review and the Critical Accounting Estimates and Judgments section in this Financial Review and in our 2022 Form 10-K for certain other factors that could cause actual results or future events to differ, perhaps materially, from historical performance and from those anticipated in the forward-looking statements included in this Report. See Note 14 Segment Reporting for a reconciliation of total business segment earnings to total PNC consolidated net income as reported on a GAAP basis. In this Report, “PNC,” “we” or “us” refers to The PNC Financial Services Group, Inc. and its subsidiaries on a consolidated basis (except when referring to PNC as a public company, its common stock or other securities issued by PNC, which just refer to The PNC Financial Services Group, Inc.). References to The PNC Financial Services Group, Inc. or to any of its subsidiaries are specifically made where applicable.

See page 103 for a glossary of certain terms and acronyms used in this Report.

EXECUTIVE SUMMARY

Headquartered in Pittsburgh, Pennsylvania, we are one of the largest diversified financial institutions in the U.S. We have businesses engaged in retail banking, including residential mortgage, corporate and institutional banking and asset management, providing many of our products and services nationally. Our retail branch network is located coast-to-coast. We also have strategic international offices in four countries outside the U.S.

Key Strategic Goals

At PNC we manage our company for the long term. We are focused on the fundamentals of growing customers, loans, deposits and revenue and improving profitability, while investing for the future and managing risk, expenses and capital. We continue to invest in our products, markets and brand, and embrace our commitments to our customers, shareholders, employees and the communities where we do business.

We strive to serve our customers and expand and deepen relationships by offering a broad range of deposit, credit and fee-based products and services. We are focused on delivering those products and services to our customers with the goal of addressing their financial objectives and needs. Our business model is built on customer loyalty and engagement, understanding our customers’ financial goals and offering our diverse products and services to help them achieve financial well-being. Our approach is concentrated on organically growing and deepening client relationships across our businesses that meet our risk/return measures.

We are focused on our strategic priorities, which are designed to enhance value over the long term, and consist of:

•Expanding our leading banking franchise to new markets and digital platforms,

•Deepening customer relationships by delivering a superior banking experience and financial solutions, and

•Leveraging technology to create efficiencies that help us better serve customers.

Our capital and liquidity priorities are to support customers, fund business investments and return excess capital to shareholders, while maintaining appropriate capital in light of economic conditions, the Basel III framework and other regulatory expectations. For more detail, see the Capital Highlights portion of this Executive Summary, the Liquidity and Capital Management portion of the Risk Management section of this Financial Review and the Supervision and Regulation section in Item 1 Business of our 2022 Form 10-K.

Presentation of Noninterest Income

In the fourth quarter of 2022, PNC updated the name of the noninterest income line item “Capital markets related” to “Capital markets and advisory.” This update did not impact the components of the category. All periods presented herein reflect these changes. For a description of each updated noninterest income revenue stream, see Note 1 Accounting Policies in our 2022 Form 10-K.

Selected Financial Data

The following tables include selected financial data, which should be reviewed in conjunction with the Consolidated Financial Statements and Notes included in Item 1 of this Report as well as the other disclosures in this Report concerning our historical financial performance, our future prospects and the risks associated with our business and financial performance.

The PNC Financial Services Group, Inc. – Form 10-Q 1

Table 1: Summary of Operations, Per Common Share Data and Performance Ratios

| Dollars in millions, except per share data Unaudited |

Three months ended | ||||||||||

| March 31 | December 31 | March 31 | |||||||||

| 2023 | 2022 | 2022 | |||||||||

| Summary of Operations (a) | |||||||||||

| Net interest income | $ | 3,585 | $ | 3,684 | $ | 2,804 | |||||

| Noninterest income | 2,018 | 2,079 | 1,888 | ||||||||

| Total revenue | 5,603 | 5,763 | 4,692 | ||||||||

| Provision for (recapture of) credit losses | 235 | 408 | (208) | ||||||||

| Noninterest expense | 3,321 | 3,474 | 3,172 | ||||||||

| Income before income taxes and noncontrolling interests |

$ | 2,047 | $ | 1,881 | $ | 1,728 | |||||

| Income taxes |

353 | 333 | 299 | ||||||||

| Net income | $ | 1,694 | $ | 1,548 | $ | 1,429 | |||||

| Net income attributable to common shareholders | $ | 1,607 | $ | 1,407 | $ | 1,361 | |||||

|

Per Common Share

|

|||||||||||

| Basic | $ | 3.98 | $ | 3.47 | $ | 3.23 | |||||

| Diluted | $ | 3.98 | $ | 3.47 | $ | 3.23 | |||||

| Book value per common share | $ | 104.76 | $ | 99.93 | $ | 106.47 | |||||

| Performance Ratios | |||||||||||

| Net interest margin (b) | 2.84 | % | 2.92 | % | 2.28 | % | |||||

| Noninterest income to total revenue | 36 | % | 36 | % | 40 | % | |||||

| Efficiency | 59 | % | 60 | % | 68 | % | |||||

| Return on: | |||||||||||

| Average common shareholders’ equity | 16.11 | % | 14.19 | % | 11.64 | % | |||||

| Average assets | 1.22 | % | 1.10 | % | 1.05 | % | |||||

(a)The Executive Summary and Consolidated Income Statement Review portions of this Financial Review section provide information regarding items impacting the comparability of the periods presented.

(b)See explanation and reconciliation of this non-GAAP measure in Average Consolidated Balance Sheet and Net Interest Analysis and Reconciliation of Taxable-Equivalent Net Interest Income (non-GAAP) in the Statistical Information (Unaudited) section in Item 1 of this Report.

Table 2: Balance Sheet Highlights and Other Selected Ratios

| Dollars in millions, except as noted Unaudited |

March 31 2023 |

December 31 2022 |

March 31 2022 |

|||||||||||

| Balance Sheet Highlights (a) | ||||||||||||||

| Assets | $ | 561,777 | $ | 557,263 | $ | 541,246 | ||||||||

| Loans | $ | 326,475 | $ | 326,025 | $ | 294,457 | ||||||||

|

Allowance for loan and lease losses |

$ | 4,741 | $ | 4,741 | $ | 4,558 | ||||||||

| Interest-earning deposits with banks | $ | 33,865 | $ | 27,320 | $ | 48,776 | ||||||||

| Investment securities | $ | 138,239 | $ | 139,334 | $ | 132,411 | ||||||||

| Total deposits | $ | 436,833 | $ | 436,282 | $ | 450,197 | ||||||||

| Borrowed funds | $ | 60,822 | $ | 58,713 | $ | 26,571 | ||||||||

| Total shareholders’ equity | $ | 49,044 | $ | 45,774 | $ | 49,181 | ||||||||

| Common shareholders’ equity | $ | 41,809 | $ | 40,028 | $ | 44,170 | ||||||||

| Other Selected Ratios | ||||||||||||||

| Common equity Tier 1 | 9.2 | % | 9.1 | % | 9.9 | % | ||||||||

| Loans to deposits | 75 | % | 75 | % | 65 | % | ||||||||

| Common shareholders’ equity to total assets | 7.4 | % | 7.2 | % | 8.2 | % | ||||||||

(a)The Executive Summary and Consolidated Balance Sheet Review portions of this Financial Review provide information regarding items impacting the comparability of the periods presented.

Income Statement Highlights

Net income of $1.7 billion, or $3.98 per diluted common share, for the first quarter of 2023 increased $146 million, or 9%, compared to $1.5 billion, or $3.47 per diluted common share, for the fourth quarter of 2022, primarily due to a lower provision for credit losses and a decline in expenses, partially offset by decreased net interest income and noninterest income.

•For the three months ended March 31, 2023 compared to the three months ended December 31, 2022:

•Total revenue decreased $160 million, or 3%, to $5.6 billion.

•Net interest income of $3.6 billion decreased $99 million, or 3%, driven by two fewer days in the quarter and higher funding costs, partially offset by higher yields on interest-earning assets.

2 The PNC Financial Services Group, Inc. – Form 10-Q

•Net interest margin decreased 8 basis points to 2.84% as higher yields on interest-earning assets were more than offset by increased funding costs.

•Noninterest income decreased $61 million, or 3%, and included lower merger and acquisition advisory activity as well as seasonally lower consumer transaction volumes.

•Provision for credit losses of $235 million in the first quarter of 2023 included the impact of updated economic assumptions and changes in portfolio composition and quality. The fourth quarter of 2022 included a provision for credit losses of $408 million.

•Noninterest expense decreased $153 million, or 4%, to $3.3 billion, reflecting strong expense control and lower personnel costs, primarily due to lower variable compensation related to decreased business activity as well as seasonally lower benefits expense.

•We generated positive operating leverage of 2%.

Net income of $1.7 billion, or $3.98 per diluted common share, for the first quarter of 2023 increased $265 million, or 19%, compared to $1.4 billion, or $3.23 per diluted common share, for the first quarter of 2022, as a result of higher net interest income and noninterest income, partially offset by a higher provision for credit losses and increased expenses.

•For the three months ended March 31, 2023 compared to the three months ended March 31, 2022:

•Total revenue increased $911 million, or 19%, to $5.6 billion.

•Net interest income increased $781 million, or 28%, as a result of higher interest-earning asset yields and balances, partially offset by higher funding costs.

•Net interest margin increased 56 basis points, reflecting the benefit of higher yields on interest-earning assets.

•Noninterest income increased $130 million, or 7%, as a result of business growth across the franchise as well as higher private equity revenue, partially offset by the impact of lower average equity markets.

•Noninterest expense increased $149 million, or 5%, due to higher personnel costs, an increased FDIC assessment rate and continued investments in technology and marketing to support business growth.

•We generated positive operating leverage of 15%.

For additional detail, see the Consolidated Income Statement Review section of this Financial Review.

Balance Sheet Highlights

Our balance sheet was strong and well positioned at March 31, 2023. In comparison to December 31, 2022:

•Total assets increased modestly, to $561.8 billion.

•Total loans remained largely stable at $326.5 billion.

•Total commercial loans increased modestly to $225.4 billion as new production and higher utilization of loan commitments were largely offset by payoffs and maturities.

•Total consumer loans were relatively stable at $101.1 billion as increases in home equity, residential mortgages and automobile loans were offset by declines in the remaining portfolios as paydowns outpaced new originations.

•Investment securities decreased $1.1 billion to $138.2 billion, due to prepayments and maturities outpacing purchases, partially offset by the favorable impact of interest rate changes on net unrealized losses for available for sale securities.

•Interest-earning deposits with banks, primarily with the Federal Reserve Bank, increased $6.5 billion, or 24%, to $33.9 billion, primarily due to higher borrowed funds and deposits. In the first quarter of 2023, Interest-earning deposits with banks also included a $1.0 billion uninsured deposit with First Republic Bank. The deposit was acquired out of First Republic Bank's receivership on May 1, 2023, and will be repaid to PNC.

•Total deposits increased $551 million to $436.8 billion as a result of higher consumer time deposits, partially offset by seasonally lower commercial deposits, and reflected a continued shift from noninterest-bearing to interest-bearing deposit products as interest rates have risen.

•Borrowed funds increased $2.1 billion, or 4%, to $60.8 billion as a result of parent company senior debt issuances in January 2023.

For additional detail, see the Consolidated Balance Sheet Review section of this Financial Review.

The PNC Financial Services Group, Inc. – Form 10-Q 3

Credit Quality Highlights

The first quarter of 2023 reflected solid credit quality performance.

•At March 31, 2023 compared to December 31, 2022:

•Nonperforming assets of $2.0 billion were stable.

•Overall loan delinquencies of $1.3 billion decreased $164 million, or 11%, driven by lower consumer and commercial loan delinquencies.

•The ACL related to loans, which consists of the ALLL and the allowance for unfunded lending related commitments, totaled $5.4 billion at both March 31, 2023 and December 31, 2022. During the three months ended March 31, 2023, reserves reflected our updated economic assumptions and changes in portfolio composition and quality. ACL to total loans was 1.66% and 1.67% at March 31, 2023 and December 31, 2022, respectively.

•Net charge-offs of $195 million, or 0.24% of average loans, in the first quarter of 2023 decreased $29 million, or 13%, compared to $224 million, or 0.28% of average loans, for the fourth quarter of 2022, due to lower consumer and commercial net charge-offs.

For additional detail see the Credit Risk Management portion of the Risk Management section of this Financial Review.

Capital and Liquidity Highlights

We maintained our strong capital and liquidity positions.

•Common shareholders’ equity of $41.8 billion at March 31, 2023, increased $1.8 billion, or 4%, compared to December 31, 2022, driven by the benefit of net income and an increase in AOCI, partially offset by common dividends paid and share repurchases during the first quarter of 2023.

•In the first quarter of 2023, PNC returned $1.0 billion of capital to shareholders, reflecting $0.6 billion of dividends on common shares and $0.4 billion of common share repurchases, representing 2.4 million shares.

•Consistent with the SCB framework, which allows for capital returns in amounts in excess of the SCB minimum levels, our Board of Directors has authorized a repurchase framework under the previously approved repurchase program of up to 100 million common shares, of which approximately 47% were still available for repurchase at March 31, 2023. Due to recent market volatility and increased economic uncertainty, share repurchase activity is expected to be reduced in the second quarter of 2023 compared to recent quarters. PNC continues to evaluate and may adjust share repurchase activity, as actual amounts and timing are dependent on market and economic conditions as well as other factors. PNC’s SCB for the four-quarter period that began October 1, 2022 is 2.9%.

•On April 3, 2023, the PNC Board of Directors declared a quarterly cash dividend on common stock of $1.50 per share payable on May 5, 2023.

•Our CET1 ratio increased to 9.2% at March 31, 2023 from 9.1% at December 31, 2022.

•PNC elected a five-year transition provision effective March 31, 2020 to delay until December 31, 2021 the full impact of the CECL standard on regulatory capital, followed by a three-year transition period. Effective for the first quarter of 2022, PNC is now in the three-year transition period, and the full impact of the CECL standard is being phased-in to regulatory capital through December 31, 2024. The fully implemented ratios reflect the full impact of CECL and exclude the benefits of this transition provision. The CET1 fully implemented ratio was 9.1% at March 31, 2023 compared to 8.9% at December 31, 2022.

•PNC’s average LCR for the three months ended March 31, 2023 was 108% and exceeded the regulatory minimum requirement throughout the quarter.

See the Liquidity and Capital Management portion of the Risk Management section of this Financial Review for more detail on our 2023 liquidity and capital actions as well as our capital ratios.

PNC’s ability to take certain capital actions, including returning capital to shareholders, is subject to PNC meeting or exceeding an SCB established by the Federal Reserve Board in connection with the Federal Reserve Board’s CCAR process. For additional information, see Capital Management in the Risk Management section in this Financial Review and the Supervision and Regulation section in our 2022 Form 10-K.

Business Outlook

Statements regarding our business outlook are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. Our forward-looking financial statements are subject to the risk that economic and financial market conditions will be substantially different than those we are currently expecting and do not take into account potential legal and regulatory contingencies. These statements are based on our views that:

•The economy continues to expand in the first half of 2023, but economic growth is slowing in response to the ongoing Federal Reserve monetary policy tightening to slow inflation. This has led to large increases in both short- and long-term interest rates. With much higher mortgage rates the housing market is already in contraction, with steep drops in existing

4 The PNC Financial Services Group, Inc. – Form 10-Q

home sales and single-family housing starts, and a modest decline in house prices. Other sectors where interest rates play an outsized role, such as business investment and consumer spending on durable goods, will contract over 2023.

•PNC’s baseline outlook is for a recession starting in the second half of 2023, with real GDP contracting less than 1% before recovery starts in the first half of 2024 as the Federal Reserve lowers interest rates in response to a deteriorating labor market and slower inflation. The unemployment rate will increase throughout 2023, peaking at above 5% in the second half of 2024. Inflation will slow with the recession and be back to the Federal Reserve’s 2% long-term objective by mid-2024.

•PNC expects the FOMC to raise the federal funds rate by 25 basis points in May. This would bring the federal funds rate to a range of 5.00% to 5.25% by early-May. PNC expects a federal funds rate cut of 25 basis points in early 2024 as inflation moves toward the FOMC’s 2% long-term objective.

For the second quarter of 2023, compared to the first quarter of 2023, we expect:

•Average loans to be stable,

•Net interest income to be down 2% to 4%,

•Fee income to be stable to down 1%,

•Other noninterest income, excluding net securities gains and Visa activity, to be $200 million to $250 million,

•Revenue to be down approximately 3%,

•Noninterest expense to be up 1% to 2%, and

•Net loan charge-offs to be $200 million to $250 million.

For the full year 2023, compared to the full year of 2022, we expect:

•Average loans to be up 5% to 7%,

•Period-end loans to be up 1% to 3%,

•Revenue to be up 4% to 5%,

•Noninterest expense to be up 2% to 3%, and

•The effective tax rate to be approximately 18%.

We cannot provide, without unreasonable effort, a meaningful or accurate reconciliation of forward-looking non-GAAP measures to their most directly comparable GAAP financial measures. This is due to the inherent difficulty of forecasting the timing and amounts necessary for the reconciliation when such amounts are subject to events that cannot be reasonably predicted, as noted in our Cautionary Statement. Accordingly, we cannot address the probable significance of unavailable information.

See the Cautionary Statement Regarding Forward-Looking Information section in this Financial Review and Item 1A Risk Factors included in this Report and in our 2022 Form 10-K for other factors that could cause future events to differ, perhaps materially, from those anticipated in these forward-looking statements.

CONSOLIDATED INCOME STATEMENT REVIEW

Our Consolidated Income Statement is presented in Item 1 of this Report.

Net income of $1.7 billion, or $3.98 per diluted common share, for the first quarter of 2023 increased $146 million, or 9%, compared to $1.5 billion, or $3.47 per diluted common share, for the fourth quarter of 2022, primarily due to a lower provision for credit losses and a decline in expenses, partially offset by decreased net interest income and noninterest income. Net income increased $265 million, or 19%, compared to $1.4 billion, or $3.23 per diluted common share for the first quarter of 2022, as a result of higher net interest income and noninterest income, partially offset by a higher provision for credit losses and increased expenses.

The PNC Financial Services Group, Inc. – Form 10-Q 5

Net Interest Income

Table 3: Summarized Average Balances and Net Interest Income (a)

| March 31, 2023 | December 31, 2022 | March 31, 2022 | ||||||||||||||||||||||||||||||||||||

| Three months ended Dollars in millions |

Average Balances |

Average Yields/ Rates |

Interest Income/ Expense |

Average Balances |

Average Yields/ Rates |

Interest Income/ Expense |

Average Balances |

Average Yields/ Rates |

Interest Income/ Expense |

|||||||||||||||||||||||||||||

| Assets | ||||||||||||||||||||||||||||||||||||||

| Interest-earning assets | ||||||||||||||||||||||||||||||||||||||

| Investment securities | $ | 143,391 | 2.49 | % | $ | 891 | $ | 142,890 | 2.36 | % | $ | 843 | $ | 133,897 | 1.64 | % | $ | 548 | ||||||||||||||||||||

| Loans | 325,526 | 5.29 | % | 4,290 | 321,875 | 4.75 | % | 3,889 | 290,701 | 3.19 | % | 2,311 | ||||||||||||||||||||||||||

| Interest-earning deposits with banks | 34,054 | 4.58 | % | 390 | 30,395 | 3.76 | % | 286 | 62,540 | 0.19 | % | 29 | ||||||||||||||||||||||||||

| Other | 8,806 | 5.75 | % | 126 | 9,690 | 5.20 | % | 127 | 9,417 | 2.07 | % | 48 | ||||||||||||||||||||||||||

| Total interest-earning assets/interest income | $ | 511,777 | 4.46 | % | 5,697 | $ | 504,850 | 4.02 | % | 5,145 | 496,555 | 2.37 | % | 2,936 | ||||||||||||||||||||||||

| Liabilities | ||||||||||||||||||||||||||||||||||||||

| Interest-bearing liabilities | ||||||||||||||||||||||||||||||||||||||

| Interest-bearing deposits | $ | 315,056 | 1.66 | % | 1,291 | $ | 301,447 | 1.07 | % | 812 | $ | 299,543 | 0.04 | % | 27 | |||||||||||||||||||||||

| Borrowed funds | 62,968 | 4.98 | % | 783 | 59,231 | 4.07 | % | 613 | 30,312 | 1.10 | % | 83 | ||||||||||||||||||||||||||

| Total interest-bearing liabilities/interest expense | $ | 378,024 | 2.20 | % | 2,074 | $ | 360,678 | 1.55 | % | 1,425 | $ | 329,855 | 0.13 | % | 110 | |||||||||||||||||||||||

| Net interest margin/income (non-GAAP) | 2.84 | % | 3,623 | 2.92 | % | 3,720 | 2.28 | % | 2,826 | |||||||||||||||||||||||||||||

| Taxable-equivalent adjustments | (38) | (36) | (22) | |||||||||||||||||||||||||||||||||||

| Net interest income (GAAP) | $ | 3,585 | $ | 3,684 | $ | 2,804 | ||||||||||||||||||||||||||||||||

(a)Interest income calculated as taxable-equivalent interest income. To provide more meaningful comparisons of interest income and yields for all interest-earning assets, as well as net interest margins, we use interest income on a taxable-equivalent basis in calculating average yields and net interest margins by increasing the interest income earned on tax-exempt assets to make it fully equivalent to interest income earned on taxable investments. This adjustment is not permitted under GAAP on the Consolidated Income Statement. For more information, see Reconciliation of Taxable-Equivalent Net Interest Income (non-GAAP) in the Statistical Information (Unaudited) section in Item 1 of this Report.

Changes in net interest income and margin result from the interaction of the volume and composition of interest-earning assets and related yields, interest-bearing liabilities and related rates paid, and noninterest-bearing sources of funding. See the Statistical Information (Unaudited) – Average Consolidated Balance Sheet And Net Interest Analysis section of this Report.

Net interest income decreased $99 million, or 3%, for the first quarter of 2023 compared to the fourth quarter of 2022, driven by two fewer days in the quarter and higher funding costs, partially offset by higher yields on interest-earning assets. Net interest income increased $781 million, or 28%, for the first quarter of 2023 compared to the same period in 2022, as a result of higher interest-earning asset yields and balances, partially offset by higher funding costs. Net interest margin decreased 8 basis points compared to the fourth quarter of 2022 as higher yields on interest-earning assets were more than offset by increased funding costs. Compared to the first quarter of 2022, net interest margin increased 56 basis points, reflecting the benefit of higher yields on interest-earning assets.

Average investment securities of $143.4 billion were relatively stable for the first quarter of 2023 compared to the fourth quarter of 2022. Compared to the first quarter of 2022, average investment securities increased $9.5 billion, or 7%, reflecting net purchases, primarily of agency residential mortgage-backed securities. Average investment securities represented 28% of average interest-earning assets for the first quarter of 2023 and the fourth quarter of 2022, and 27% for the first quarter of 2022.

Average loans of $325.5 billion for the first quarter of 2023 increased $3.7 billion compared to the fourth quarter of 2022, primarily driven by growth in PNC’s corporate banking business during the fourth quarter of 2022. In comparison to the first quarter of 2022, average loans increased $34.8 billion, or 12%, reflecting growth in both commercial and consumer loans. Average loans represented 64% of average interest-earning assets for both the first quarter of 2023 and the fourth quarter of 2022, and 59% for the first quarter of 2022.

Average interest-earning deposits with banks of $34.1 billion for the first quarter of 2023, increased $3.7 billion, or 12% compared to the fourth quarter of 2022, primarily due to higher borrowed funds and deposits. Compared to the first quarter of 2022, average interest-earning deposits with banks decreased $28.5 billion, or 46%, primarily due to higher loans outstanding.

Average interest-bearing deposits of $315.1 billion for the first quarter of 2023 increased $13.6 billion, or 5%, and $15.5 billion, or 5%, compared to the fourth and first quarters of 2022, respectively. Both comparisons reflected a continued shift from noninterest-bearing to interest-bearing deposits, as interest rates have risen. In total, average interest-bearing deposits represented 83% of average interest-bearing liabilities for the first quarter of 2023, 84% for the fourth quarter of 2022 and 91% for the first quarter of 2022.

6 The PNC Financial Services Group, Inc. – Form 10-Q

Average borrowed funds of $63.0 billion for the first quarter of 2023 increased $3.7 billion, or 6%, compared to the fourth quarter of 2022, driven by parent company senior debt issuances in January 2023. Compared to the first quarter of 2022, average borrowed funds increased $32.7 billion, or 108% due to increased FHLB borrowings and senior debt issuances.

Further details regarding average loans and deposits are included in the Business Segments Review section of this Financial Review.

Noninterest Income

Table 4: Noninterest Income

| Three months ended | Three months ended | ||||||||||||||||||||||||||||||||||||||||||||||

| March 31 | December 31 | Change | March 31 | March 31 | Change | ||||||||||||||||||||||||||||||||||||||||||

| Dollars in millions | 2023 | 2022 | $ | % | 2023 | 2022 | $ | % | |||||||||||||||||||||||||||||||||||||||

| Noninterest income | |||||||||||||||||||||||||||||||||||||||||||||||

| Asset management and brokerage | $ | 356 | $ | 345 | $ | 11 | 3 | % | $ | 356 | $ | 377 | $ | (21) | (6) | % | |||||||||||||||||||||||||||||||

| Capital markets and advisory | 262 | 336 | (74) | (22) | % | 262 | 252 | 10 | 4 | % | |||||||||||||||||||||||||||||||||||||

| Card and cash management | 659 | 671 | (12) | (2) | % | 659 | 620 | 39 | 6 | % | |||||||||||||||||||||||||||||||||||||

| Lending and deposit services | 306 | 296 | 10 | 3 | % | 306 | 269 | 37 | 14 | % | |||||||||||||||||||||||||||||||||||||

| Residential and commercial mortgage | 177 | 184 | (7) | (4) | % | 177 | 159 | 18 | 11 | % | |||||||||||||||||||||||||||||||||||||

| Other | 258 | 247 | 11 | 4 | % | 258 | 211 | 47 | 22 | % | |||||||||||||||||||||||||||||||||||||

Total noninterest income |

$ | 2,018 | $ | 2,079 | $ | (61) | (3) | % | $ | 2,018 | $ | 1,888 | $ | 130 | 7 | % | |||||||||||||||||||||||||||||||

Noninterest income as a percentage of total revenue was 36% for both the first quarter of 2023 and the fourth quarter of 2022 compared to 40% for the first quarter of 2022.

Asset management and brokerage fees increased compared to the fourth quarter of 2022, reflecting the impact of higher average equity markets and increased annuity sales. The decrease compared to the first quarter of 2022 reflected the impact of lower average equity markets. PNC’s discretionary client assets under management of $177 billion at March 31, 2023 increased from $173 billion at December 31, 2022, primarily as a result of higher spot equity markets. PNC’s discretionary client assets under management decreased from $182 billion at March 31, 2022, driven by lower spot equity markets.

Capital markets and advisory fees decreased compared to the fourth quarter of 2022 driven by lower merger and acquisition advisory fees. The increase compared to the first quarter of 2022 included higher asset backed financing, merger and acquisition advisory and underwriting fees.

Card and cash management revenue decreased compared to the fourth quarter of 2022, reflecting seasonally lower consumer transaction volumes. The increase in the first quarter of 2022 comparison was primarily due to increased treasury management product revenue and higher consumer spending.

Lending and deposit services increased compared to both the fourth and first quarters of 2022, primarily driven by increased client activity.

Residential and commercial mortgage decreased compared to the fourth quarter of 2022 due to lower results from residential mortgage servicing rights valuation, net of economic hedge. The increase compared to the first quarter of 2022 was driven by modestly higher commercial and residential banking activities.

Other noninterest income increased compared to both the fourth quarter and first quarter of 2022. The increase compared to the first quarter of 2022 included the impact of higher private equity revenue. The first quarter of 2023 included $45 million of negative Visa Class B fair value adjustments compared to $41 million of negative adjustments in the fourth quarter of 2022, and $4 million of positive adjustments for the first quarter of 2022.

The PNC Financial Services Group, Inc. – Form 10-Q 7

Noninterest Expense

Table 5: Noninterest Expense

| Three months ended | Three months ended | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| March 31 | December 31 | Change | March 31 | March 31 | Change | ||||||||||||||||||||||||||||||||||||||||||||||||

| Dollars in millions | 2023 | 2022 | $ | % | 2023 | 2022 | $ | % | |||||||||||||||||||||||||||||||||||||||||||||

| Noninterest expense | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Personnel | $ | 1,826 | $ | 1,943 | $ | (117) | (6) | % | $ | 1,826 | $ | 1,717 | $ | 109 | 6 | % | |||||||||||||||||||||||||||||||||||||

| Occupancy | 251 | 247 | 4 | 2 | % | 251 | 258 | (7) | (3) | % | |||||||||||||||||||||||||||||||||||||||||||

| Equipment | 350 | 369 | (19) | (5) | % | 350 | 331 | 19 | 6 | % | |||||||||||||||||||||||||||||||||||||||||||

| Marketing | 74 | 106 | (32) | (30) | % | 74 | 61 | 13 | 21 | % | |||||||||||||||||||||||||||||||||||||||||||

| Other | 820 | 809 | 11 | 1 | % | 820 | 805 | 15 | 2 | % | |||||||||||||||||||||||||||||||||||||||||||

Total noninterest expense |

$ | 3,321 | $ | 3,474 | $ | (153) | (4) | % | $ | 3,321 | $ | 3,172 | $ | 149 | 5 | % | |||||||||||||||||||||||||||||||||||||

Noninterest expense decreased compared to the fourth quarter of 2022, reflecting strong expense control and lower personnel costs, primarily due to lower variable compensation related to decreased business activity as well as seasonally lower benefits expense. The increase compared to the first quarter of 2022 was due to higher personnel costs, increased technology costs and marketing to support business growth. In both comparisons, the increase in other noninterest expense included the impact of a higher FDIC assessment rate, which resulted in an additional $25 million of expense in the first quarter of 2023.

Effective Income Tax Rate

The effective income tax rate was 17.2% in the first quarter of 2023, compared to 17.7% in the fourth quarter of 2022, and 17.3% for the same period in 2022.

Provision For (Recapture of) Credit Losses

Table 6: Provision for (Recapture of) Credit Losses

| Three months ended | Three months ended | ||||||||||||||||||||||||||||||||||

| March 31 | December 31 | Change | March 31 | March 31 | Change | ||||||||||||||||||||||||||||||

| Dollars in millions | 2023 | 2022 | $ | 2023 | 2022 | $ | |||||||||||||||||||||||||||||

| Provision for (recapture of) credit losses | |||||||||||||||||||||||||||||||||||

| Loans and leases | $ | 229 | $ | 380 | $ | (151) | $ | 229 | $ | (172) | $ | 401 | |||||||||||||||||||||||

| Unfunded lending related commitments | (22) | 12 | (34) | (22) | (23) | 1 | |||||||||||||||||||||||||||||

| Investment securities | (1) | 10 | (11) | (1) | 1 | (2) | |||||||||||||||||||||||||||||

| Other financial assets | 29 | 6 | 23 | 29 | (14) | 43 | |||||||||||||||||||||||||||||

| Total provision for (recapture of) credit losses | $ | 235 | $ | 408 | $ | (173) | $ | 235 | $ | (208) | $ | 443 | |||||||||||||||||||||||

Provision for credit losses of $235 million in the first quarter of 2023 included the impact of updated economic assumptions and changes in portfolio composition and quality. The fourth quarter of 2022 included a provision for credit losses of $408 million. The first quarter of 2022 included a recapture of credit losses of $208 million.

8 The PNC Financial Services Group, Inc. – Form 10-Q

CONSOLIDATED BALANCE SHEET REVIEW

The summarized balance sheet data in Table 7 is based upon our Consolidated Balance Sheet in Item 1 of this Report.

Table 7: Summarized Balance Sheet Data

| March 31 | December 31 | Change | |||||||||||||||||||||

| Dollars in millions | 2023 | 2022 | $ | % | |||||||||||||||||||

| Assets | |||||||||||||||||||||||

| Interest-earning deposits with banks | $ | 33,865 | $ | 27,320 | $ | 6,545 | 24 | % | |||||||||||||||

| Loans held for sale | 998 | 1,010 | (12) | (1) | % | ||||||||||||||||||

| Investment securities | 138,239 | 139,334 | (1,095) | (1) | % | ||||||||||||||||||

| Loans | 326,475 | 326,025 | 450 | — | |||||||||||||||||||

| Allowance for loan and lease losses | (4,741) | (4,741) | — | ||||||||||||||||||||

| Mortgage servicing rights | 3,293 | 3,423 | (130) | (4) | % | ||||||||||||||||||

| Goodwill | 10,987 | 10,987 | — | ||||||||||||||||||||

| Other | 52,661 | 53,905 | (1,244) | (2) | % | ||||||||||||||||||

| Total assets | $ | 561,777 | $ | 557,263 | $ | 4,514 | 1 | % | |||||||||||||||

| Liabilities | |||||||||||||||||||||||

| Deposits | $ | 436,833 | $ | 436,282 | $ | 551 | — | ||||||||||||||||

| Borrowed funds | 60,822 | 58,713 | 2,109 | 4 | % | ||||||||||||||||||

| Allowance for unfunded lending related commitments | 672 | 694 | (22) | (3) | % | ||||||||||||||||||

| Other | 14,376 | 15,762 | (1,386) | (9) | % | ||||||||||||||||||

| Total liabilities | 512,703 | 511,451 | 1,252 | — | |||||||||||||||||||

| Equity | |||||||||||||||||||||||

| Total shareholders’ equity | 49,044 | 45,774 | 3,270 | 7 | % | ||||||||||||||||||

| Noncontrolling interests | 30 | 38 | (8) | (21) | % | ||||||||||||||||||

| Total equity | 49,074 | 45,812 | 3,262 | 7 | % | ||||||||||||||||||

| Total liabilities and equity | $ | 561,777 | $ | 557,263 | $ | 4,514 | 1 | % | |||||||||||||||

Our balance sheet was strong and well positioned at March 31, 2023. In comparison to December 31, 2022:

•Total assets increased modestly, and included higher Federal Reserve Bank balances.

•Total liabilities were largely stable.

•Total equity increased due to the benefit of net income, a preferred stock issuance and an improvement in AOCI, partially offset by dividends paid and common share repurchases.

The ACL related to loans totaled $5.4 billion at both March 31, 2023 and December 31, 2022. During the three months ended March 31, 2023, reserves reflected our updated economic assumptions and changes in portfolio composition and quality. See the following for additional information regarding our ACL related to loans:

•Allowance for Credit Losses in the Credit Risk Management section of this Financial Review,

•Critical Accounting Estimates and Judgments section of this Financial Review, and

•Note 3 Loans and Related Allowance for Credit Losses.

The following discussion provides additional information about the major components of our balance sheet. Information regarding our capital and regulatory compliance is included in the Liquidity and Capital Management portion of the Risk Management section in this Financial Review and in Note 20 Regulatory Matters in our 2022 Form 10-K.

The PNC Financial Services Group, Inc. – Form 10-Q 9

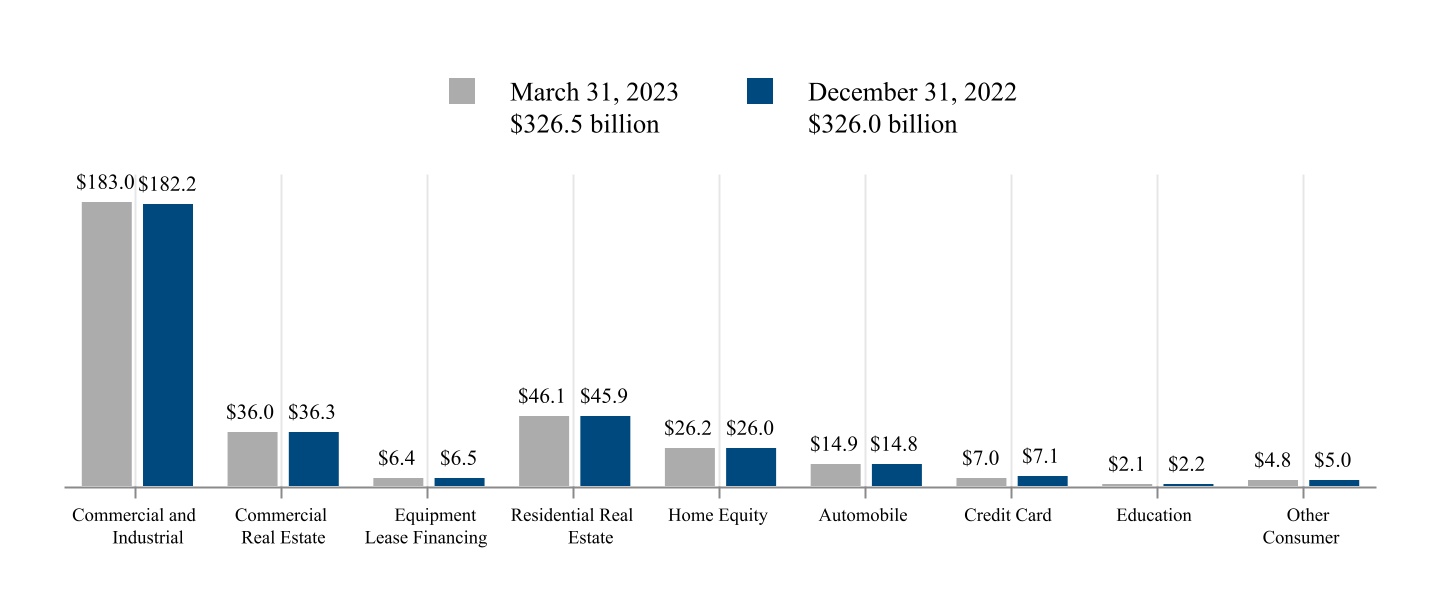

Loans

Table 8: Loans

| March 31 | December 31 | Change | |||||||||||||||||||||

| Dollars in millions | 2023 | 2022 | $ | % | |||||||||||||||||||

| Commercial | |||||||||||||||||||||||

| Commercial and industrial | $ | 182,997 | $ | 182,219 | $ | 778 | — | ||||||||||||||||

| Commercial real estate | 35,991 | 36,316 | (325) | (1) | % | ||||||||||||||||||

| Equipment lease financing | 6,424 | 6,514 | (90) | (1) | % | ||||||||||||||||||

| Total commercial | 225,412 | 225,049 | 363 | — | |||||||||||||||||||

| Consumer | |||||||||||||||||||||||

| Residential real estate | 46,067 | 45,889 | 178 | — | |||||||||||||||||||

| Home equity | 26,203 | 25,983 | 220 | 1 | % | ||||||||||||||||||

| Automobile | 14,923 | 14,836 | 87 | 1 | % | ||||||||||||||||||

| Credit card | 6,961 | 7,069 | (108) | (2) | % | ||||||||||||||||||

| Education | 2,131 | 2,173 | (42) | (2) | % | ||||||||||||||||||

| Other consumer | 4,778 | 5,026 | (248) | (5) | % | ||||||||||||||||||

| Total consumer | 101,063 | 100,976 | 87 | — | |||||||||||||||||||

| Total loans | $ | 326,475 | $ | 326,025 | $ | 450 | — | ||||||||||||||||

Commercial loans increased modestly as an increase in commercial and industrial loans was offset by declines in both commercial real estate and equipment lease financing.

Consumer loans were relatively stable as increases in home equity, residential mortgages and automobile loans were offset by declines in the remaining portfolios as paydowns outpaced new originations.

For additional information regarding our loan portfolio see the Credit Risk Management portion of the Risk Management section in this Financial Review and Note 3 Loans and Related Allowance for Credit Losses.

10 The PNC Financial Services Group, Inc. – Form 10-Q

Investment Securities

Investment securities of $138.2 billion at March 31, 2023 decreased $1.1 billion, compared to December 31, 2022, due to prepayments and maturities outpacing purchases, partially offset by the favorable impact of interest rate changes on net unrealized losses for available for sale securities.

The level and composition of the investment securities portfolio fluctuates over time based on many factors, including market conditions, loan and deposit growth and balance sheet management activities. We manage our investment securities portfolio to optimize returns, while providing a reliable source of liquidity for our banking and other activities, considering the LCR, NSFR and other internal and external guidelines and constraints.

Table 9: Investment Securities (a)

| March 31, 2023 | December 31, 2022 | ||||||||||||||||||||||

| Dollars in millions | Amortized Cost (b) |

Fair Value |

Amortized Cost (b) |

Fair Value |

|||||||||||||||||||

| U.S. Treasury and government agencies | $ | 45,291 | $ | 43,455 | $ | 45,767 | $ | 43,330 | |||||||||||||||

| Agency residential mortgage-backed | 76,701 | 71,565 | 77,385 | 71,073 | |||||||||||||||||||

| Non-agency residential mortgage-backed | 947 | 1,040 | 973 | 1,074 | |||||||||||||||||||

| Agency commercial mortgage-backed | 2,674 | 2,518 | 2,693 | 2,501 | |||||||||||||||||||

| Non-agency commercial mortgage-backed (c) | 2,624 | 2,529 | 2,992 | 2,883 | |||||||||||||||||||

| Asset-backed (d) | 7,277 | 7,219 | 7,291 | 7,183 | |||||||||||||||||||

| Other (e) | 6,482 | 6,319 | 6,642 | 6,394 | |||||||||||||||||||

| Total investment securities (f) | $ | 141,996 | $ | 134,645 | $ | 143,743 | $ | 134,438 | |||||||||||||||

(a)Of our total securities portfolio, 97% were rated AAA/AA at both March 31, 2023 and December 31, 2022.

(b)Amortized cost is presented net of the allowance for investment securities, which totaled $148 million at March 31, 2023 and primarily related to non-agency commercial mortgage-backed securities. The comparable amount at December 31, 2022 was $149 million.

(c)Collateralized primarily by office buildings, multifamily housing, retail properties, lodging properties and industrial properties.

(d)Collateralized primarily by corporate debt, government guaranteed education loans and other consumer credit products.

(e)Includes state and municipal securities.

(f)Includes available for sale and held to maturity securities, which are recorded on our balance sheet at fair value and amortized cost, respectively.

Table 9 presents our investment securities portfolio by amortized cost and fair value. The relationship of fair value to amortized cost at March 31, 2023 compared to December 31, 2022 primarily reflected the impact of lower interest rates on the valuation of fixed rate securities. We continually monitor the credit risk in our portfolio and maintain the allowance for investment securities at an appropriate level to absorb expected credit losses on our investment securities portfolio for the remaining contractual term of the securities adjusted for expected prepayments. See Note 2 Investment Securities for additional details regarding the allowance for investment securities.

The duration of investment securities was 4.4 years and 4.5 years at March 31, 2023 and December 31, 2022, respectively. We estimate that at March 31, 2023 the effective duration of investment securities was 4.4 years for an immediate 50 basis points parallel increase in interest rates and 4.4 years for an immediate 50 basis points parallel decrease in interest rates. Comparable amounts at December 31, 2022 for the effective duration of investment securities were 4.4 years and 4.5 years, respectively.

Based on expected prepayment speeds, the weighted-average expected maturity of the investment securities portfolio was 5.8 years at March 31, 2023 compared to 6.0 years at December 31, 2022.

Table 10: Weighted-Average Expected Maturities of Mortgage and Asset-Backed Debt Securities

| March 31, 2023 | Years | |||||||

| Agency residential mortgage-backed | 7.5 | |||||||

| Non-agency residential mortgage-backed | 10.1 | |||||||

| Agency commercial mortgage-backed | 5.3 | |||||||

| Non-agency commercial mortgage-backed | 1.4 | |||||||

| Asset-backed | 2.4 | |||||||

Additional information regarding our investment securities portfolio is included in Note 2 Investment Securities and Note 11 Fair Value.

The PNC Financial Services Group, Inc. – Form 10-Q 11

Funding Sources

Table 11: Details of Funding Sources

| March 31 | December 31 | Change | |||||||||||||||||||||

| Dollars in millions | 2023 | 2022 | $ | % | |||||||||||||||||||

| Deposits | |||||||||||||||||||||||

| Noninterest-bearing | $ | 118,014 | $ | 124,486 | $ | (6,472) | (5) | % | |||||||||||||||

| Interest-bearing | |||||||||||||||||||||||

| Money market | 63,943 | 64,150 | (207) | — | |||||||||||||||||||

| Demand | 128,404 | 126,143 | 2,261 | 2 | % | ||||||||||||||||||

| Savings | 104,712 | 103,033 | 1,679 | 2 | % | ||||||||||||||||||

| Time deposits | 21,760 | 18,470 | 3,290 | 18 | % | ||||||||||||||||||

| Total interest-bearing deposits | 318,819 | 311,796 | 7,023 | 2 | % | ||||||||||||||||||

| Total deposits | 436,833 | 436,282 | 551 | — | |||||||||||||||||||

| Borrowed funds | |||||||||||||||||||||||

| Federal Home Loan Bank borrowings | 32,020 | 32,075 | (55) | — | |||||||||||||||||||

| Senior debt | 19,622 | 16,657 | 2,965 | 18 | % | ||||||||||||||||||

| Subordinated debt | 5,630 | 6,307 | (677) | (11) | % | ||||||||||||||||||

| Other | 3,550 | 3,674 | (124) | (3) | % | ||||||||||||||||||

| Total borrowed funds | 60,822 | 58,713 | 2,109 | 4 | % | ||||||||||||||||||

| Total funding sources | $ | 497,655 | $ | 494,995 | $ | 2,660 | 1 | % | |||||||||||||||

Total deposits increased modestly as a result of higher consumer time deposits, partially offset by seasonally lower commercial deposits. In addition, noninterest-bearing balances decreased due to the continued shift into interest-bearing deposit products as interest rates have risen.

Borrowed funds increased due to parent company senior debt issuances in January 2023.

The level and composition of borrowed funds fluctuates over time based on many factors, including market conditions, loan, investment securities and deposit growth and capital considerations. We manage our borrowed funds to provide a reliable source of liquidity for our banking and other activities, considering our LCR and NSFR requirements and other internal and external guidelines and constraints. See the Liquidity and Capital Management portion of the Risk Management section in this Financial Review for additional information regarding our liquidity and capital activities. See Note 7 Borrowed Funds in this Report and Note 10 Borrowed Funds in our 2022 Form 10-K for additional information related to our borrowings.

Shareholders’ Equity

Total shareholders’ equity was $49.0 billion at March 31, 2023, an increase of $3.2 billion compared to December 31, 2022, as increases related to net income of $1.7 billion, a preferred stock issuance of $1.5 billion and an improvement in AOCI of $1.1 billion were partially offset by dividends paid of $0.7 billion and common share repurchases of $0.4 billion.

12 The PNC Financial Services Group, Inc. – Form 10-Q

BUSINESS SEGMENTS REVIEW

We have three reportable business segments:

•Retail Banking

•Corporate & Institutional Banking

•Asset Management Group

Business segment results and a description of each business are included in Note 14 Segment Reporting. Certain amounts included in this Business Segments Review differ from those amounts shown in Note 14, primarily due to the presentation in this Financial Review of business net interest income on a taxable-equivalent basis.

Net interest income in business segment results reflects our internal funds transfer pricing methodology. Assets receive a funding charge and liabilities and capital receive a funding credit based on a transfer pricing methodology that incorporates product repricing characteristics, tenor and other factors.

Total business segment financial results differ from total consolidated net income. The impact of these differences is reflected in the “Other” category as shown in Table 78 in Note 14 Segment Reporting. “Other” includes residual activities that do not meet the criteria for disclosure as a separate reportable business, such as asset and liability management activities, including net securities gains or losses, ACL for investment securities, certain trading activities, certain runoff consumer loan portfolios, private equity investments, intercompany eliminations, certain corporate overhead, tax adjustments that are not allocated to business segments, exited businesses and differences between business segment performance reporting and financial statement reporting (GAAP).

The PNC Financial Services Group, Inc. – Form 10-Q 13

Retail Banking

Retail Banking’s core strategy is to build lifelong, primary relationships by creating a sense of financial well-being and ease for our clients. Over time, we seek to deepen those relationships by meeting the broad range of our clients’ financial needs across savings, liquidity, lending, payments, investment and retirement solutions. We work to deliver these solutions in the most seamless and efficient way possible, meeting our customers where they want to be met – whether in a branch, through digital channels, at an ATM or through our phone-based customer contact centers – while continuously optimizing the cost to sell and service. We believe that, over time, we can grow our customer base, enhance the breadth and depth of our client relationships and improve our efficiency through differentiated products and leading digital channels.

Table 12: Retail Banking Table

| (Unaudited) | |||||||||||||||||||||||

| Three months ended March 31 | Change | ||||||||||||||||||||||

| Dollars in millions, except as noted | 2023 | 2022 | $ | % | |||||||||||||||||||

| Income Statement | |||||||||||||||||||||||

| Net interest income | $ | 2,281 | $ | 1,531 | $ | 750 | 49 | % | |||||||||||||||

| Noninterest income | 743 | 745 | (2) | — | |||||||||||||||||||

| Total revenue | 3,024 | 2,276 | 748 | 33 | % | ||||||||||||||||||

| Provision for (recapture of) credit losses | 238 | (81) | 319 | * | |||||||||||||||||||

| Noninterest expense | 1,927 | 1,892 | 35 | 2 | % | ||||||||||||||||||

| Pretax earnings | 859 | 465 | 394 | 85 | % | ||||||||||||||||||

| Income taxes | 202 | 109 | 93 | 85 | % | ||||||||||||||||||

| Noncontrolling interests | 10 | 16 | (6) | (38) | % | ||||||||||||||||||

| Earnings | $ | 647 | $ | 340 | $ | 307 | 90 | % | |||||||||||||||

| Average Balance Sheet | |||||||||||||||||||||||

| Loans held for sale | $ | 542 | $ | 1,183 | $ | (641) | (54) | % | |||||||||||||||

| Loans | |||||||||||||||||||||||

| Consumer | |||||||||||||||||||||||

| Residential real estate | $ | 35,421 | $ | 31,528 | $ | 3,893 | 12 | % | |||||||||||||||

| Home equity | 24,571 | 22,458 | 2,113 | 9 | % | ||||||||||||||||||

| Automobile | 14,918 | 16,274 | (1,356) | (8) | % | ||||||||||||||||||

| Credit card | 6,904 | 6,401 | 503 | 8 | % | ||||||||||||||||||

| Education | 2,188 | 2,532 | (344) | (14) | % | ||||||||||||||||||

| Other consumer | 1,990 | 2,348 | (358) | (15) | % | ||||||||||||||||||

| Total consumer | 85,992 | 81,541 | 4,451 | 5 | % | ||||||||||||||||||

| Commercial | 11,438 | 11,610 | (172) | (1) | % | ||||||||||||||||||

| Total loans | $ | 97,430 | $ | 93,151 | $ | 4,279 | 5 | % | |||||||||||||||

| Total assets | $ | 115,384 | $ | 111,754 | $ | 3,630 | 3 | % | |||||||||||||||

| Deposits | |||||||||||||||||||||||

| Noninterest-bearing | $ | 60,801 | $ | 64,058 | $ | (3,257) | (5) | % | |||||||||||||||

| Interest-bearing | 201,720 | 201,021 | 699 | — | |||||||||||||||||||

| Total deposits | $ | 262,521 | $ | 265,079 | $ | (2,558) | (1) | % | |||||||||||||||

| Performance Ratios | |||||||||||||||||||||||

| Return on average assets | 2.27 | % | 1.23 | % | |||||||||||||||||||

| Noninterest income to total revenue | 25 | % | 33 | % | |||||||||||||||||||

| Efficiency | 64 | % | 83 | % | |||||||||||||||||||

14 The PNC Financial Services Group, Inc. – Form 10-Q

At or for three months ended March 31 |

Change | ||||||||||||||||||||||

| Dollars in millions, except as noted | 2023 | 2022 | $ | % | |||||||||||||||||||

| Supplemental Noninterest Income Information | |||||||||||||||||||||||

| Asset management and brokerage | $ | 131 | $ | 134 | $ | (3) | (2) | % | |||||||||||||||

| Card and cash management | $ | 324 | $ | 308 | $ | 16 | 5 | % | |||||||||||||||

| Lending and deposit services | $ | 181 | $ | 164 | $ | 17 | 10 | % | |||||||||||||||

| Residential and commercial mortgage | $ | 104 | $ | 99 | $ | 5 | 5 | % | |||||||||||||||

| Residential Mortgage Information | |||||||||||||||||||||||

| Residential mortgage servicing statistics (in billions, except as noted) (a) | |||||||||||||||||||||||

| Serviced portfolio balance (b) | $ | 188 | $ | 135 | $ | 53 | 39 | % | |||||||||||||||

| Serviced portfolio acquisitions | $ | 2 | $ | 6 | $ | (4) | (67) | % | |||||||||||||||

| MSR asset value (b) | $ | 2.2 | $ | 1.3 | $ | 0.9 | 69 | % | |||||||||||||||

| MSR capitalization value (in basis points) (b) | 119 | 98 | 21 | 21 | % | ||||||||||||||||||

| Servicing income: (in millions) | |||||||||||||||||||||||

| Servicing fees, net (c) | $ | 78 | $ | 33 | $ | 45 | * | ||||||||||||||||

| Mortgage servicing rights valuation, net of economic hedge | $ | 14 | $ | 2 | $ | 12 | * | ||||||||||||||||

| Residential mortgage loan statistics | |||||||||||||||||||||||

| Loan origination volume (in billions) | $ | 1.4 | $ | 5.1 | $ | (3.7) | (73) | % | |||||||||||||||

| Loan sale margin percentage | 2.26 | % | 2.45 | % | |||||||||||||||||||

| Percentage of originations represented by: | |||||||||||||||||||||||

| Purchase volume (d) | 84 | % | 42 | % | |||||||||||||||||||

| Refinance volume | 16 | % | 58 | % | |||||||||||||||||||

| Other Information (b) | |||||||||||||||||||||||

| Customer-related statistics (average) | |||||||||||||||||||||||

| Non-teller deposit transactions (e) | 65 | % | 64 | % | |||||||||||||||||||

| Digital consumer customers (f) | 75 | % | 78 | % | |||||||||||||||||||

| Credit-related statistics | |||||||||||||||||||||||

| Nonperforming assets | $ | 1,009 | $ | 1,168 | $ | (159) | (14) | % | |||||||||||||||

| Net charge-offs - loans and leases | $ | 112 | $ | 141 | $ | (29) | (21) | % | |||||||||||||||

| Other statistics | |||||||||||||||||||||||

| ATMs | 8,697 | 9,502 | (805) | (8) | % | ||||||||||||||||||

| Branches (g) | 2,450 | 2,591 | (141) | (5) | % | ||||||||||||||||||

| Brokerage account client assets (in billions) (h) | $ | 73 | $ | 74 | $ | (1) | (1) | % | |||||||||||||||

*- Not Meaningful

(a) Represents mortgage loan servicing balances for third parties and the related income.

(b)Presented as of period end, except for average customer-related statistics and net charge-offs, which are both shown for the three months ended.

(c)Servicing fees net of impact of decrease in MSR value due to passage of time, including the impact from regularly scheduled loan principal payments, prepayments and loans paid off during the period.

(d)Mortgages with borrowers as part of residential real estate purchase transactions.

(e)Percentage of total consumer and business banking deposit transactions processed at an ATM or through our mobile banking application.

(f)Represents consumer checking relationships that process the majority of their transactions through non-teller channels.

(g)Reflects all branches and solution centers excluding standalone mortgage offices and satellite offices (e.g., drive-ups, electronic branches and retirement centers) that provide limited products and/or services.

(h)Includes cash and money market balances.

Retail Banking earnings for the first three months of 2023 increased $307 million compared to the same period in 2022 primarily due to increased net interest income, partially offset by an increased provision for credit losses, and higher noninterest expense.

Net interest income increased in the comparison primarily due to wider interest rate spreads on the value of deposits, partially offset by narrower interest rate spreads on the value of loans.

Noninterest income was relatively stable in the comparison.

Provision for credit losses included the impact of updated economic assumptions and changes in portfolio composition and quality.

Noninterest expense increased in the comparison, and included increased technology costs and higher marketing spend.

Retail Banking average total loans increased in the first three months of 2023 compared to the same period in 2022. Average consumer loans increased 5% driven by higher residential real estate and home equity loans as a result of new volume and draws on existing accounts outpacing liquidations, as well as growth in credit card loans due to new account production and purchase volume increases. The increase was partially offset by a decline in automobile, education and other consumer loans as paydowns outpaced new

The PNC Financial Services Group, Inc. – Form 10-Q 15

originations. Average commercial loans decreased primarily due to forgiveness of PPP loans, largely offset by growth in dealer segment balances.

Our focus on growing primary customer relationships is at the core of our deposit strategy in Retail, which is based on attracting and retaining stable, low-cost deposits as a key funding source for PNC. We have taken a disciplined approach to pricing, focused on retaining relationship-based balances and executing on targeted deposit growth and retention strategies aimed at more rate sensitive customers. Our goal with regard to deposits is to optimize balances, economics and long-term customer growth. In the first three months of 2023, average total deposits decreased compared to the same period in 2022, reflecting the impact of inflationary pressures and competitive pricing dynamics.

As part of our strategic focus on growing customers and meeting their financial needs, we have established a coast-to-coast network of retail branches, solution centers and ATMs that operate alongside PNC’s suite of digital capabilities. Over time, we plan to continue to convert a portion of branches into solution centers, which have a distinctive layout and the capability to support transactions, sales and advice using a combination of technology and personalized banker assistance.

Retail Banking continues to enhance the customer experience with refinements to product and service offerings that drive value for consumers and small businesses. We are focused on meeting the financial needs of customers by providing a broad range of liquidity, banking, payments and investment products.

16 The PNC Financial Services Group, Inc. – Form 10-Q

Corporate & Institutional Banking

Corporate & Institutional Banking’s strategy is to be the leading relationship-based provider of traditional banking products and services to its customers through the economic cycles. We aim to grow our market share and drive higher returns by delivering value-added solutions that help our clients better run their organizations, all while maintaining prudent risk and expense management. We continue to focus on building client relationships where the risk-return profile is attractive.

Table 13: Corporate & Institutional Banking Table

| (Unaudited) | |||||||||||||||||||||||

| Three months ended March 31 | Change | ||||||||||||||||||||||

| Dollars in millions, except as noted | 2023 | 2022 | $ | % | |||||||||||||||||||

| Income Statement | |||||||||||||||||||||||

| Net interest income | $ | 1,414 | $ | 1,160 | $ | 254 | 22 | % | |||||||||||||||

| Noninterest income | 886 | 804 | 82 | 10 | % | ||||||||||||||||||

| Total revenue | 2,300 | 1,964 | 336 | 17 | % | ||||||||||||||||||

| Provision for (recapture of) credit losses | (28) | (118) | 90 | 76 | % | ||||||||||||||||||

| Noninterest expense | 939 | 837 | 102 | 12 | % | ||||||||||||||||||

| Pretax earnings | 1,389 | 1,245 | 144 | 12 | % | ||||||||||||||||||

| Income taxes | 325 | 285 | 40 | 14 | % | ||||||||||||||||||

| Noncontrolling interests | 5 | 4 | 1 | 25 | % | ||||||||||||||||||

| Earnings | $ | 1,059 | $ | 956 | $ | 103 | 11 | % | |||||||||||||||

| Average Balance Sheet | |||||||||||||||||||||||

| Loans held for sale | $ | 456 | $ | 628 | $ | (172) | (27) | % | |||||||||||||||

| Loans | |||||||||||||||||||||||

| Commercial | |||||||||||||||||||||||

| Commercial and industrial | $ | 168,874 | $ | 141,622 | $ | 27,252 | 19 | % | |||||||||||||||

| Commercial real estate | 34,605 | 32,433 | 2,172 | 7 | % | ||||||||||||||||||

| Equipment lease financing | 6,451 | 6,099 | 352 | 6 | % | ||||||||||||||||||

| Total commercial | 209,930 | 180,154 | 29,776 | 17 | % | ||||||||||||||||||

| Consumer | 7 | 8 | (1) | (13) | % | ||||||||||||||||||

| Total loans | $ | 209,937 | $ | 180,162 | $ | 29,775 | 17 | % | |||||||||||||||

| Total assets | $ | 234,536 | $ | 200,724 | $ | 33,812 | 17 | % | |||||||||||||||

| Deposits | |||||||||||||||||||||||

| Noninterest-bearing | $ | 58,529 | $ | 86,178 | $ | (27,649) | (32) | % | |||||||||||||||

| Interest-bearing | 86,832 | 68,429 | 18,403 | 27 | % | ||||||||||||||||||

| Total deposits | $ | 145,361 | $ | 154,607 | $ | (9,246) | (6) | % | |||||||||||||||

| Performance Ratios | |||||||||||||||||||||||

| Return on average assets | 1.83 | % | 1.93 | % | |||||||||||||||||||

| Noninterest income to total revenue | 39 | % | 41 | % | |||||||||||||||||||

| Efficiency | 41 | % | 43 | % | |||||||||||||||||||

| Other Information | |||||||||||||||||||||||

| Consolidated revenue from: (a) | |||||||||||||||||||||||

| Treasury Management (b) | $ | 785 | $ | 546 | $ | 239 | 44 | % | |||||||||||||||

| Commercial mortgage banking activities: | |||||||||||||||||||||||

| Commercial mortgage loans held for sale (c) | $ | 27 | $ | 16 | $ | 11 | 69 | % | |||||||||||||||

| Commercial mortgage loan servicing income (d) | 39 | 68 | (29) | (43) | % | ||||||||||||||||||

| Commercial mortgage servicing rights valuation, net of economic hedge | 41 | 13 | 28 | 215 | % | ||||||||||||||||||

| Total | $ | 107 | $ | 97 | $ | 10 | 10 | % | |||||||||||||||

| Commercial mortgage servicing statistics | |||||||||||||||||||||||

| Serviced portfolio balance (in billions) (e) | $ | 281 | $ | 278 | $ | 3 | 1 | % | |||||||||||||||

| MSR asset value (e) | $ | 1,061 | $ | 886 | $ | 175 | 20 | % | |||||||||||||||

| Average loans by C&IB business | |||||||||||||||||||||||

| Corporate Banking | $ | 118,229 | $ | 92,503 | $ | 25,726 | 28 | % | |||||||||||||||

| Real Estate | 47,297 | 43,213 | 4,084 | 9 | % | ||||||||||||||||||

| Business Credit | 30,180 | 26,535 | 3,645 | 14 | % | ||||||||||||||||||

| Commercial Banking | 8,430 | 10,045 | (1,615) | (16) | % | ||||||||||||||||||

| Other | 5,801 | 7,866 | (2,065) | (26) | % | ||||||||||||||||||

| Total average loans | $ | 209,937 | $ | 180,162 | $ | 29,775 | 17 | % | |||||||||||||||

| Credit-related statistics | |||||||||||||||||||||||

| Nonperforming assets (e) | $ | 801 | $ | 866 | $ | (65) | (8) | % | |||||||||||||||

| Net charge-offs (recoveries) - loans and leases | $ | 85 | $ | (1) | $ | 86 | * | ||||||||||||||||

*- Not Meaningful

(a)See the additional revenue discussion regarding treasury management and commercial mortgage banking activities in the Product Revenue section of this Corporate & Institutional Banking section.

The PNC Financial Services Group, Inc. – Form 10-Q 17

(b)Amounts are reported in net interest income and noninterest income.

(c)Represents commercial mortgage banking income for valuations on commercial mortgage loans held for sale and related commitments, derivative valuations, origination fees, gains on sale of loans held for sale and net interest income on loans held for sale.

(d)Represents net interest income and noninterest income from loan servicing, net of reduction in commercial mortgage servicing rights due to amortization expense and payoffs. Commercial mortgage servicing rights valuation, net of economic hedge is shown separately.

(e)As of March 31.

Corporate & Institutional Banking earnings in the first three months of 2023 increased $103 million compared to the same period in 2022 driven by higher net interest income and noninterest income, partially offset by increased noninterest expense and a lower provision recapture.

Net interest income increased in the comparison primarily due to wider interest rate spreads on the value of deposits and higher average loan balances, partially offset by narrower interest rate spreads on the value of loans and lower average deposit balances.

Noninterest income increased in the comparison and included higher capital markets and advisory fees and growth in treasury management product revenue.

Noninterest expense increased in the comparison due to continued investments to support business growth.

Average loans increased compared to the three months ended March 31, 2022 due to increases in Corporate Banking, Real Estate and Business Credit, partially offset by a decrease in Commercial Banking:

•Corporate Banking provides lending, equipment finance, treasury management and capital markets products and services to mid-sized and large corporations, and government and not-for-profit entities. Average loans for this business increased driven by strong new production throughout 2022 and higher average utilization of loan commitments.

•Real Estate provides banking, financing and servicing solutions for commercial real estate clients across the country. Average loans for this business increased largely due to new production throughout 2022, partially offset by a lower average utilization of loan commitments.

•Business Credit provides asset-based lending and equipment financing solutions. The loan and lease portfolio is relatively high yielding, with acceptable risk as the loans are mainly secured by business assets. Average loans for this business increased primarily driven by new production and higher utilization of loan commitments.

•Commercial Banking provides lending, treasury management and capital markets related products and services to smaller corporations and businesses. Average loans for this business declined primarily driven by PPP loan forgiveness and lower average utilization of loan commitments.

The deposit strategy of Corporate & Institutional Banking is to remain disciplined on pricing and focused on growing and retaining relationship-based balances over time, executing on customer and segment-specific deposit growth strategies and continuing to provide funding and liquidity to PNC. Average total deposits decreased compared to the three months ended March 31, 2022, reflecting the impact of competitive pricing dynamics. We continue to actively monitor the interest rate environment and make adjustments to our deposit strategy in response to evolving market conditions, bank funding needs and client relationship dynamics.

Following the BBVA acquisition in 2021 and our de novo expansion efforts, we are now a coast-to-coast franchise and have a presence in the largest 30 U.S. metropolitan statistical areas. These expanded locations complement Corporate & Institutional Banking’s existing national businesses with a significant presence in these cities, and our full suite of commercial products and services are offered nationally.

Product Revenue

In addition to credit and deposit products for commercial customers, Corporate & Institutional Banking offers other services, including treasury management, capital markets and advisory products and services and commercial mortgage banking activities, for customers of all business segments. On a consolidated basis, the revenue from these other services is included in net interest income and noninterest income, as appropriate. From a business perspective, the majority of the revenue and expense related to these services is reflected in the Corporate & Institutional Banking segment results, and the remainder is reflected in the results of other businesses where the customer relationship exists. The Other Information section in Table 13 includes the consolidated revenue to PNC for treasury management and commercial mortgage banking services. A discussion of the consolidated revenue from these services follows.

The Treasury Management business provides corporations with cash and investment management services, receivables and disbursement management services, funds transfer services, international payment services and access to online/mobile information management and reporting services. Treasury management revenue is reported in noninterest income and net interest income. Noninterest income includes treasury management product revenue less earnings credits provided to customers on compensating deposit balances used to pay for products and services. Net interest income includes funding credit from all treasury management customer deposit balances. Compared to the first three months of 2022, treasury management revenue increased due to wider interest rate spreads on the value of deposits and higher noninterest income.

18 The PNC Financial Services Group, Inc. – Form 10-Q

Commercial mortgage banking activities include revenue derived from commercial mortgage servicing (both net interest income and noninterest income), revenue derived from commercial mortgage loans held for sale and hedges related to those activities. Total revenue from commercial mortgage banking activities increased in the comparison primarily due to a higher benefit from commercial mortgage servicing rights valuation, net of economic hedge and higher revenue from commercial mortgage loans held for sale, partially offset by lower commercial mortgage servicing income.

Capital markets and advisory includes services and activities primarily related to merger and acquisition advisory, equity capital markets advisory, asset-backed financing, loan syndication, securities underwriting and customer-related trading. The increase in capital markets and advisory fees in the comparison was mostly driven by higher fees and credit valuation on customer-related derivative activities as well as asset-backed financing and underwriting fees.

The PNC Financial Services Group, Inc. – Form 10-Q 19

Asset Management Group

The Asset Management Group strives to be the leading relationship-based provider of investment, planning, credit and cash management solutions and fiduciary services to affluent individuals and institutions by endeavoring to proactively deliver value-added ideas, solutions and exceptional service. Asset Management Group’s priorities are to serve our clients’ financial objectives, grow and deepen customer relationships and deliver solid financial performance with prudent risk and expense management.

Table 14: Asset Management Group Table

| (Unaudited) | |||||||||||||||||||||||